FOMC November Meeting Key Points

- After a surprisingly strong couple of weeks of US economic data, traders are starting to wonder if even a 25bps-at-each-Fed-meeting pace may be too much for rate cuts.

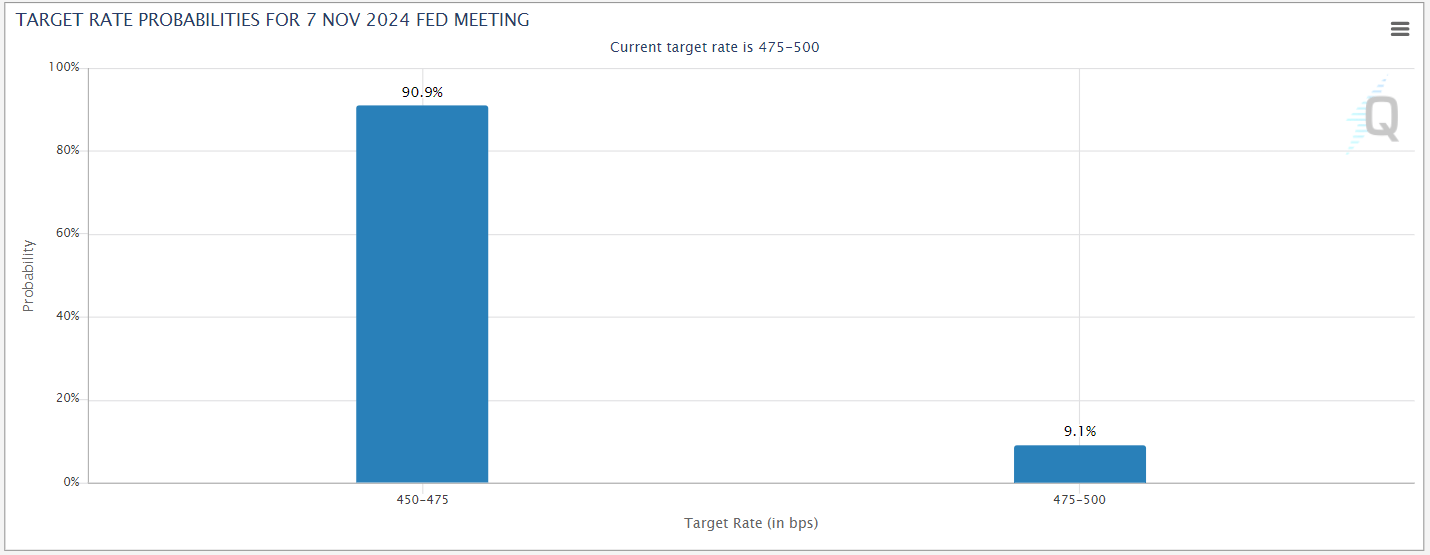

- Traders are pricing in roughly a 1-in-10 chance that the Fed leaves interest rates unchanged at its November, but it may take 4 more better-than-expected US economic reports in a row.

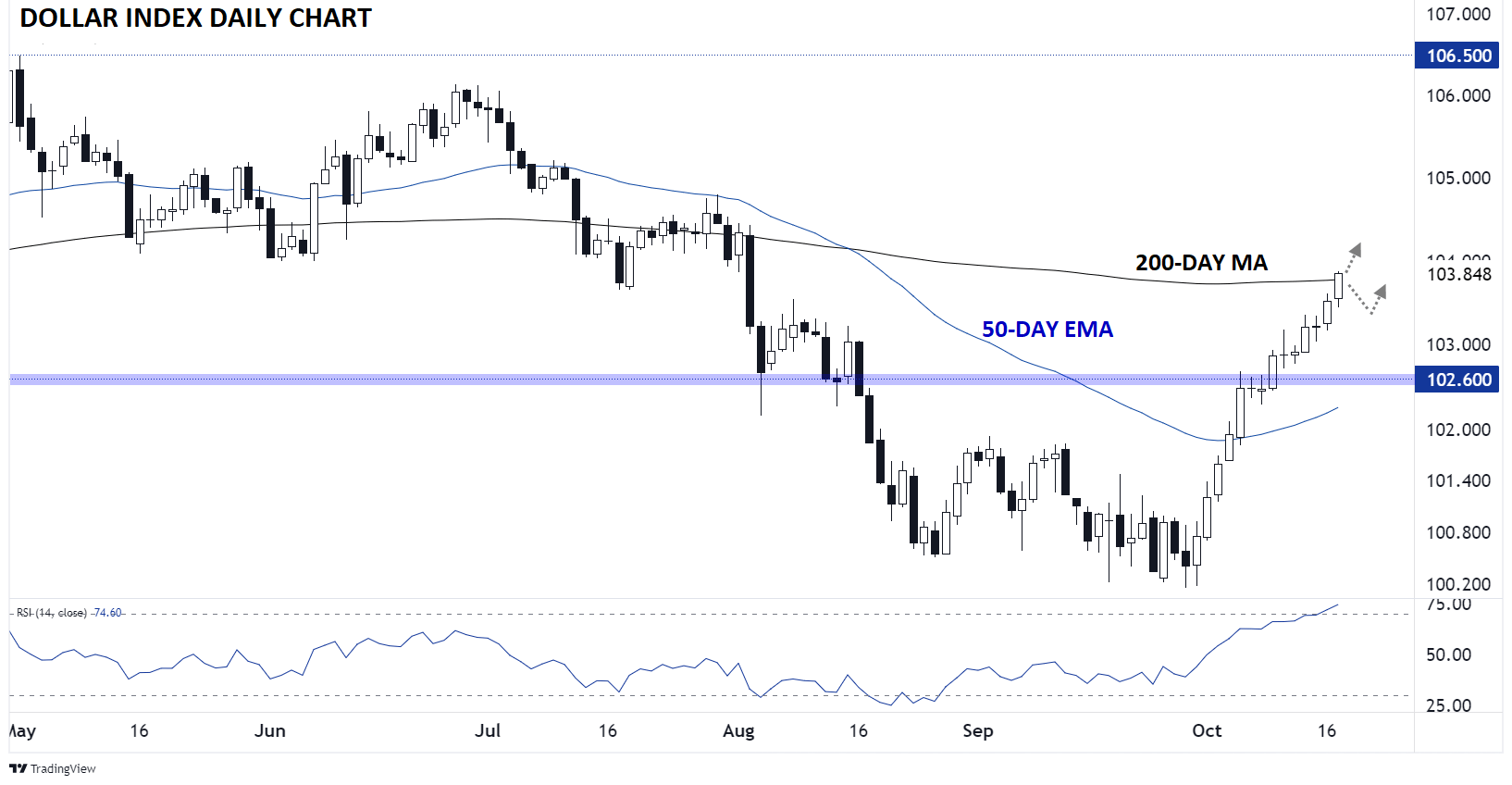

- The US Dollar Index’s technical bias will remain to the upside as long as it holds above its 50-day EMA and previous support/resistance near 102.60

Just as a wise sailor must be alert to any potential shift in the winds and currents, a successful trader must navigate the shifting narratives that drive markets and policy.

When it comes to the US central bank, Federal Reserve Chairman Jerome Powell emphasized a shift in focus from the inflation to the labor market at his Jackson Hole speech in August, foreshadowing the 50bps (0.50%) interest rate cut that the central bank ultimately delivered last month, though Fed speakers were clear in their subsequent comments that they expected to downshift toward 25bps rate cuts moving forward.

After a surprisingly strong couple of weeks of US economic data however, traders are starting to wonder if even a 25bps-at-each-Fed-meeting pace may be too much. Starting with a blowout jobs report at the start of this month and followed by a hotter-than-expected US CPI report last week, it’s clear that to the extent that the Fed is data dependent, it should be viewing the economy as stronger than it was at the start of October.

Though not necessarily top-tier releases, this morning’s data only further underscored the outperformance of the US economy. Retail Sales, the headline release, came in at 0.4% m/m vs. 0.3% expected, and more impressively, the “Core” Retail Sales reading was 0.5% m/m, crushing expectations of a mere 0.1% uptick. At the same time, initial jobless claims feel sharply to 241K after last week’s (potentially weather-distorted?) 260K reading, and even the Philly Fed Manufacturing Index came in above expectations at 10.3 vs. 4.2 anticipated.

All of that data now has traders pricing in roughly a 1-in-10 chance that the Fed leaves interest rates unchanged at its November, per the CME FedWatch tool:

Source: CME FedWatch

In my view, these odds are about right at the moment: In the end, Jerome Powell and Company prefer to make gradual, predictable changes to monetary policy to minimize any disruption to the underlying economy. Careening from leaving interest rates unchanged for years to a 50bps rate cut back to pausing the implied rate cut cycle would introduce additional uncertainty into the US economy, right at the same time that a new President will be preparing to take office.

The scenario where the Fed feels comfortable leaving interest rates unchanged would be a parlay of unanimously strong economic reports between now and the next monetary policy meeting on November 6, specifically better-than-expected labor market data and hotter-than-anticipated inflation figures. For me, the four reports to watch between now and then are two initial unemployment claims readings on October 24 and 31, the Core PCE report on October 31, and the October NFP report on November 1. If we naively assume each of those reports has a 50% chance to “beat” expectations and every one must beat for the Fed to hold rates, the odds of a Fed hold in November should be ~6%, near the current implied price.

Put simply, there’s a narrow path toward a Fed pause in November, but it would likely require every notable economic report between now and then indicating a stronger-than-assumed US economy. Regardless of what the Fed does in November though, the projected path for interest rates looking out into 2025 and beyond is higher than it’s been in weeks (if not months!), and that’s lending support to the US dollar.

US Dollar Technical Analysis – DXY Daily Chart

Source: TradingView, StoneX

From a technical perspective, the US Dollar Index (DXY) has been on a tear since the start of the month, surging from near 100.00 even to almost 104.00 as of writing. The index is now trading above its 200-day MA for the first time since the start of August on the back of strong US data and a shift toward more easing from the US’s major rivals.

Looking ahead, some profit-taking is definitely possible heading into the weekend (or if any of the economic reports noted above miss expectations). That said, DXY’s technical bias will remain to the upside as long as it holds above its 50-day EMA and previous support/resistance near 102.60.

-- Written by Matt Weller, Global Head of Research

Check out Matt’s Daily Market Update videos on YouTube and be sure to follow Matt on Twitter: @MWellerFX

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Yesterday 07:31 PM

Latest Fed articles

December 23, 2024 11:30 PM

December 17, 2024 04:12 PM

December 17, 2024 06:28 AM

December 13, 2024 10:13 AM