Today 4:00 AM

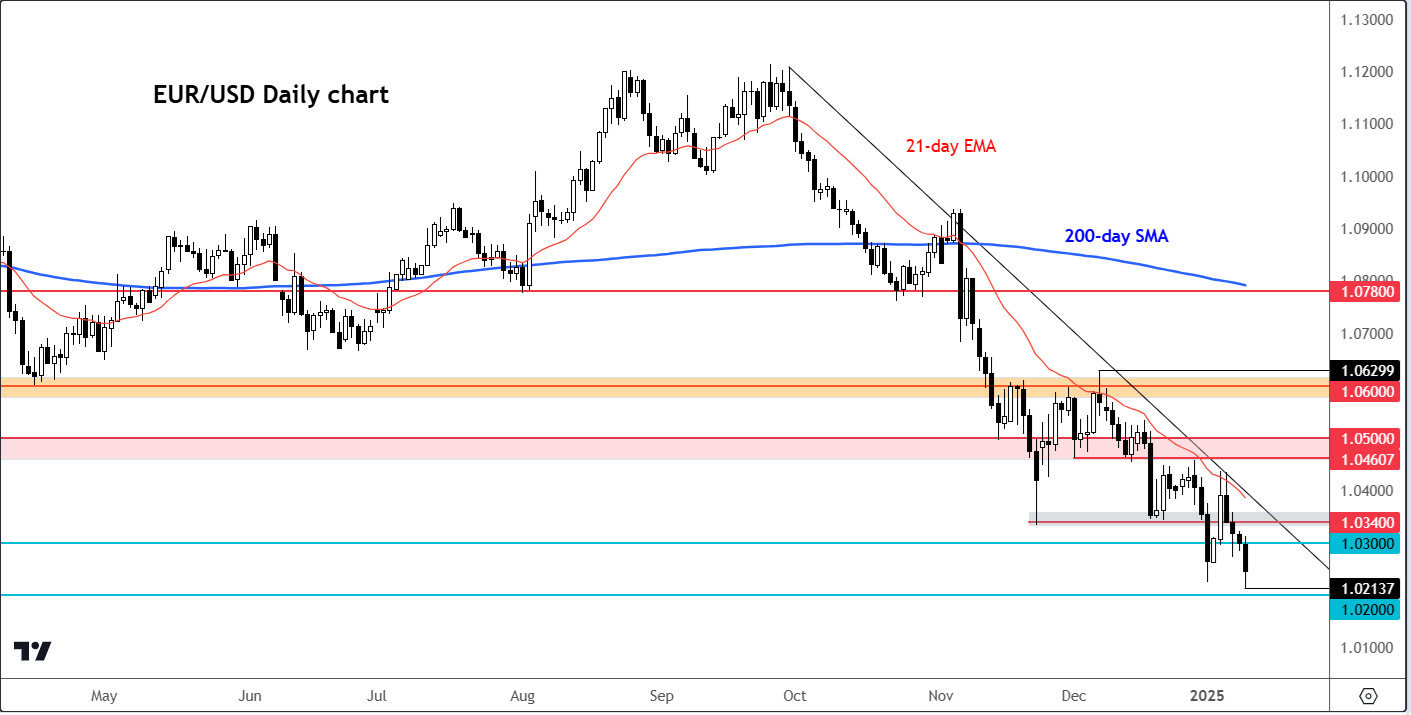

The EUR/USD fell to a new multi-year low of just shy of 1.0200, before bouncing modestly off its earlier lows. The currency pair is now on track to drop for the fourth consecutive month. In the last 15 weeks, it has only managed two small positive weekly closes. The bearish momentum has been gathering pace, owing largely to a strengthening US dollar. Meanwhile, weak growth in the Eurozone and China have also weighed on the single currency, not to mentioned ongoing political turmoil in Germany and France. Against this backdrop, the EUR/USD forecast remains bearish, and we could see the pair drop below $1.02 handle in the early parts of the week ahead.

EUR/USD forecast: Why has the dollar been rising?

The greenback has been supported by investors repricing US interest rates higher due, first and foremost, to expectations of inflationary policies under Donald Trump, when he takes office later this month. At the same time, we have seen surprising strength in US data. This was again highlighted by the non-farm payrolls report on Friday, pointing to a labour market that appears to be gaining momentum again. Consequently, traders have now shifted the full pricing of the next Fed rate cut all the way to the start of Q4. Consequently, US bond yields have pushed further higher, with the benchmark 10-year now yielding 4.76% - and getting closer to last year’s high of 5.02% that was hit in October, just before the Fed pivoted. Due to this hawkish repricing of US interest rates, the EUR/USD forecast remains bearish as we look forward to another week of volatility. US CPI and Chinese GDP are among the data highlight to watch.

Source: TradingView.com

So, how strong was the jobs growth?

Well, it was almost extremely robust. While revisions shaved about 8K off the previous two months' figures, the December payrolls report significantly outperformed expectations. Markets reacted swiftly: stock index futures sold off, and the dollar gained strength against all major currencies, except the yen. The unemployment rate also declined to 4.1% from 4.2%, bolstering the argument for an extended pause in policy changes from the Fed. Meanwhile, average earnings met expectations, rising 0.3% month-over-month and 3.9% year-over-year, slightly down from 4.0%. The combination of strong headline job gains and steady wage growth highlights a resilient labour market.

Attention turns to US CPI and Chinese growth

Should CPI inflation data on Wednesday show signs of persisting, any calls for a rate cut in the first half of the year will be firmly dismissed again. In any case, the upside potential for the EUR/USD is likely to be limited until something changes fundamentally. Thus, if CPI is to cause a shift in the market, it will have to be significantly weaker to cause a major dent in the dollar’s bullish trend or the EUR/USD’s bearish trend.

On Friday, we will have some important data from China. In addition to GDP figures, the day will bring the latest retail sales and industrial production data from the world’s second-largest economy. China's gloomy economic outlook has driven a surge in demand for Chinese bonds, pushing down yields, local stock prices, and the yuan. It has also had a negative influence on the EUR/USD exchange rate. Stronger data will be crucial to alleviating concerns about a potential deflationary spiral in the Chinese economy. But if data reveals weakening growth, then this should further weigh on Chinese assets, and undermine the EUR/USD forecast.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 01:00 PM

Today 08:00 AM

Yesterday 10:00 PM

Yesterday 05:00 PM

January 10, 2025 08:30 PM

Latest EUR/USD Weekly Outlook articles

December 8, 2024 03:00 AM

November 17, 2024 03:00 AM

November 10, 2024 03:00 AM

September 29, 2024 03:00 AM