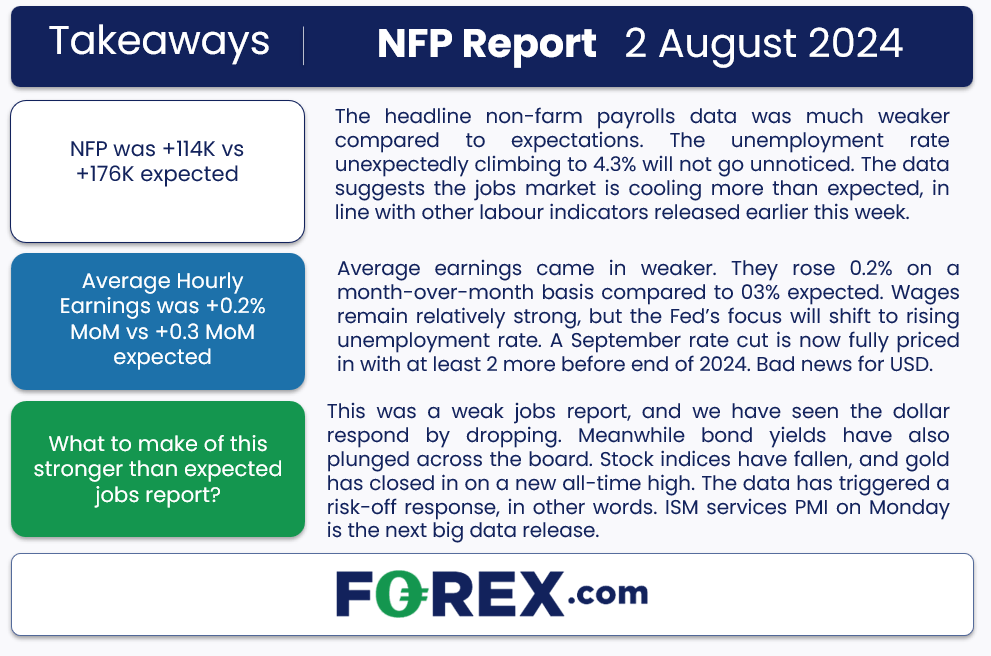

This was a weak jobs report, and we have seen the dollar respond by dropping. Meanwhile bond yields have also plunged across the board. Stock indices have fallen, and gold has closed in on a new all-time high. The data has triggered a risk-off response, in other words. The jobs data completes a week marked by weaker US economic data, a dovish Fed, and a surprisingly hawkish Bank of Japan. There is one more macro even left that could provide even more volatility in the markets, namely the ISM services PMI on Monday. I reckon once the equity market volatility settles, the recent weakness in US data should translate into a more widespread dollar weakness. So, I maintain a bearish dollar forecast for the week ahead, especially now that we have seen a weaker jobs report today.

NFP disappoints, triggering bond market rally

The headline non-farm payrolls data was much weaker compared to expectations (NFP was +114K vs +176K expected). The unemployment rate unexpectedly climbing to 4.3% will not go unnoticed. The data suggests the jobs market is cooling more than expected, in line with other labour indicators released earlier this week.

Average earnings came in weaker. They rose 0.2% on a month-over-month basis compared to 03% expected. Wages remain relatively strong, but the Fed’s focus will shift to rising unemployment rate. A September rate cut is now fully priced in with at least 2 more before end of 2024. Bad news for USD.

Before discussing the jobs report and looking ahead to next week, let’s have a quick look at the dollar index chart.

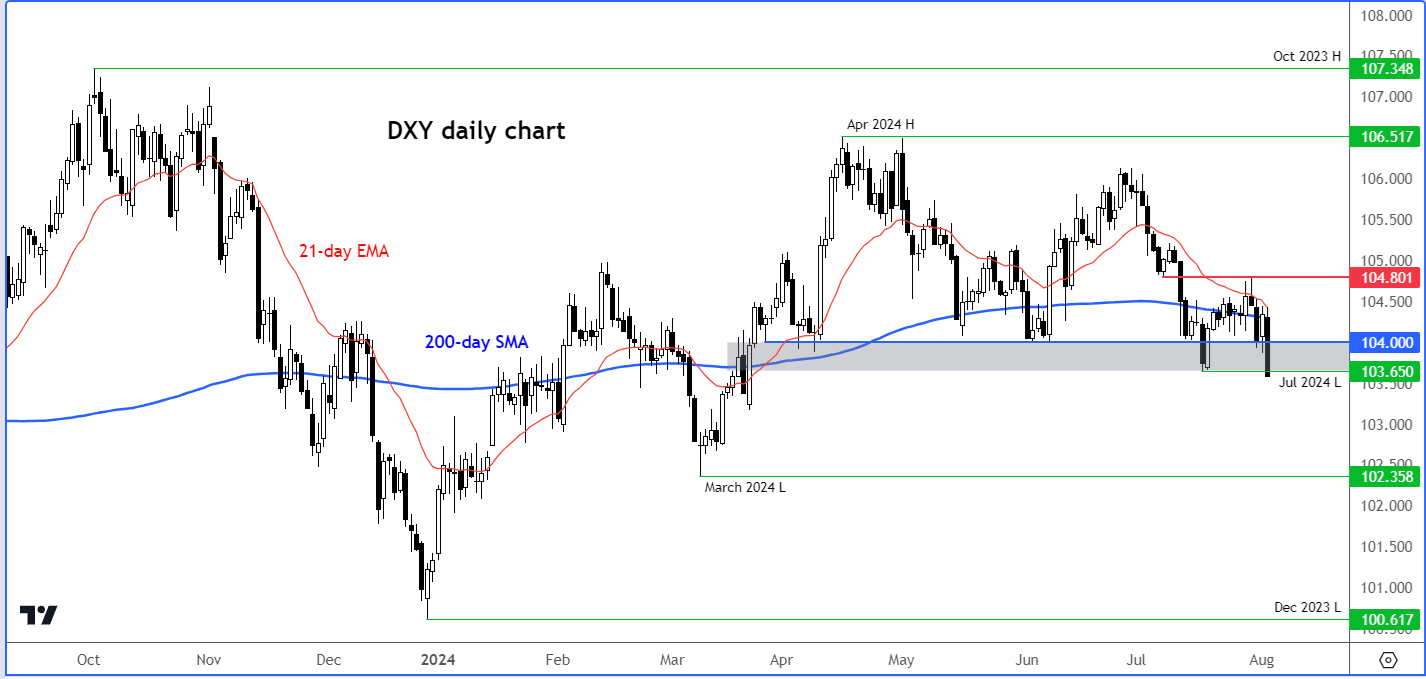

Dollar Index testing key 104.00 support

Source: TradingView.com

If the dollar index breaks below the 104.00 support on a closing basis, I reckon more losses can be on the way in the days ahead given the weakening US macro data we have seen of late. This level has been tested several times in the last few months and so far held. But the more a level gets tested, the more likely it is going to break. So watch out below!

Dollar forecast: NFP disappoints

What caused all the turmoil in risk this week?

Weak US economic reports, particularly the ISM services PMI, mixed-to-weak tech earnings, and less-than-expected dovish stances from the Federal Reserve and the Bank of England while not forgetting a more hawkish Bank of Japan than expected, have dampened risk appetite. This week's disappointing US data has caused bond yields to drop significantly, though this hasn't yet translated to a weaker dollar, except against the yen, with the equity sell-off keeping the dollar strong against commodity currencies. Manufacturing activity contracted the most in eight months according to PMI data, while initial jobless claims hit a one-year high as hiring slowed.

Dollar forecast: Markets price in 3 rate cuts

The cooling job market and economy have fuelled speculation of three more rate cuts before year-end, despite the Fed's less dovish policy stance recently. There was a heightened risk of today’s non-farm payrolls report falling short if this week’s labour market indicators are anything to go by - and that's precisely what happened (see above). Jobless claims rose to 249k from 235k previously, and the ISM manufacturing employment index dropped to 43.4 from 49.2, the lowest since June 2020. Additionally, new orders declined, with demand softening further, while supply chain pipelines and inventories remain full. Now that the NFP has disappointed, calls for Fed action will intensify further.

Week ahead: ISM Services PMI, RBA rate decision and Canadian jobs report

Looking ahead to next week, the ISM services report from the US is the major event on the calendar. While there are some secondary data releases from the Asia Pacific region, none of these are expected to shake up the markets as much as recent events have. This suggests that market movements next week might be driven more by changes in risk appetite. However, with a lack of a major catalyst, volatility might be on the lower side.

ISM services PMI

Monday, 5 August

15:00 BST

Following a rather poor ISM manufacturing PMI last week, which triggered recession alarm bells and a drop in stocks and bond yields, the focus will now turn to the largest sector of the economy with the release of the services PMI. This is expected to rebound back into expansion (at 51.3) following a surprise drop into contraction last month (48.8). That drop was driven by a slump in business activity, contracting for first time since May 2020, while new orders also contracted. With the Fed growing more concerned about employment, it is worth keeping an eye on the employment component of the latest ISM Services PMI as well as the headline reading.

RBA rate decision

Tuesday, 6 August

05:30 BST

Let's make this clear: The RBA doesn't seem to have a tough choice ahead. Their latest quarterly inflation figures were lower than anticipated, which might prompt them to ease off their hawkish stance in their policy statement. Sure, inflation is still higher than desired, but this data might be enough to shift their tone. Even if they don't, traders likely won't take their hawkish signals seriously. Considering the Fed's dovish stance and the RBNZ's shift away from a hawkish approach, there's little reason to expect a rate hike, especially with growth indicators weakening, despite overall strong employment numbers.

Canadian jobs report

Friday, 9 August

13:30 BST

Last month’s surprise drop in employment hurt the Canadian dollar, which suffered further blows from a sell-off in crude oil and a general risk-off tone across financial markets last week. The Bank of Canada has already started to ease its policy, cutting the benchmark overnight rate twice now by 25 basis points at its past two meetings. At 4.50%, Canada’s base rate is lower than the US and UK, which explains why the USD/CAD has been on the rise. Should Canadian data weaken further then the CAD/JPY might be a more interesting pair to watch given the yen’s big upsurge amid a refreshingly hawkish Bank of Japan.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Yesterday 10:18 PM

Yesterday 10:16 PM

Yesterday 09:00 PM

Yesterday 08:00 PM

Yesterday 07:39 PM

Yesterday 07:00 PM

Latest Forex Friday articles

December 6, 2024 05:13 PM

December 6, 2024 08:23 AM

December 4, 2024 09:46 PM

December 4, 2024 01:49 AM