Global stock markets exhibited mixed performances on Friday, January 17, 2025, influenced by a combination of economic data, corporate earnings, and geopolitical events.

Asian Markets

In Asia, stock indices reflected varied outcomes:

- Japan's Nikkei 225: The index declined by 1%, influenced by a strengthening yen and rising speculation about a potential Bank of Japan rate hike.

- China's Shanghai Composite: The index experienced a slight uptick, as China's economy achieved its 5% growth target for 2024, driven by a nearly 6% surge in manufacturing due to strong exports and consumption-boosting policies.

- Hong Kong's Hang Seng: The index rose modestly, aligning with the positive economic data from China.

European Markets

European markets opened cautiously, with investors focusing on the eurozone's consumer inflation data and the UK's retail sales figures. The Ibex 35 retreated by 0.5%, moving away from the 11,900-point mark.

The euro remained below $1.03, and Brent crude oil prices increased by 0.8%.

United States Markets

On Wall Street, major indices experienced slight declines amid mixed earnings reports and economic data suggesting tempered U.S. economic growth. The future actions of the Federal Reserve regarding interest rates remain a point of speculation amid inflation reports.

Corporate News

Taiwan Semiconductor Manufacturing Company (TSMC) reported a significant profit increase of 57% to NT$374.7 billion ($11.37 billion) in Q4 2024, exceeding analyst expectations. The company attributed its strong performance to high demand for artificial intelligence (AI), which is balancing the typically slow sales period for smartphones. TSMC's revenue soared 39% to NT$868.5 billion.

In the electric vehicle (EV) market, Tesla initiated discounts on its Cybertruck models, offering reductions ranging from $1,600 to $3,270. This move comes amid a competitive landscape and follows the company's decision to reassign some workers from the Cybertruck production line to the Model Y line at its Austin factory. Despite Tesla's claim of the Cybertruck being America's top-selling electric pickup in 2024, the introduction of discounts suggests efforts to bolster demand in a crowded market.

Commodities and Currency

In the commodities market, oil prices edged higher following previous declines, with Brent crude at $81.42 and WTI at $78.95. The dollar weakened, lifting the yen and gold prices.

Economic Data

In the United States, the Philadelphia Fed's economic index rose from minus 10.9 points in the previous month to plus 44.3 points in January, marking the highest level since April 2021 and the second-largest monthly increase on record. The sub-index for new orders showed particularly strong growth. Retail sales in December did not rise as much as expected overall, but the "Retail Control" group—which excludes food, auto, building materials, and fuel—saw a more significant increase than forecasted. Initial jobless claims rose more than expected in the previous week, primarily due to wildfires in California; however, the four-week average reached its lowest level since April 2024. Despite these positive indicators, financial markets showed little reaction, appearing more focused on the inauguration of the new U.S. administration.

Economic Calendar

Looking ahead, U.S. markets will be closed on Monday, January 20, 2025, in observance of Martin Luther King Jr. Day. Investors will be monitoring upcoming economic data releases and corporate earnings reports for further insights into market trends.

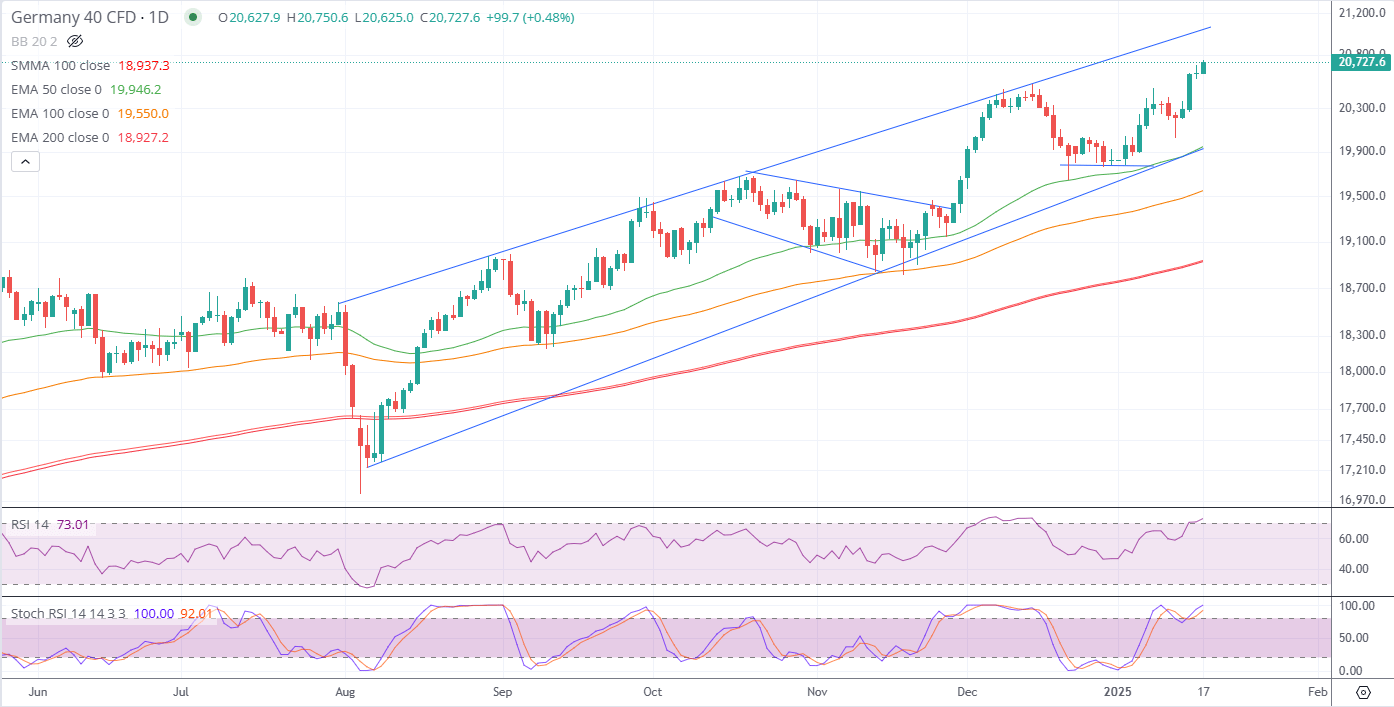

DAX Technical Analysis (1 Day)

DAX (Germany 40) index continues to exhibit a robust upward trajectory, maintaining its position within a well-defined ascending trend channel over the medium to long term. This pattern indicates sustained investor confidence, as the index has consistently registered higher lows and higher highs, suggesting potentially favorable market outlook.

Currently, the DAX is trading near its all-time highs, with no significant resistance levels immediately apparent in the price chart. This absence of overhead resistance implies potential for further gains. In the event of a market correction, the index might find support around the 19,900-point mark, followed by 19,500.

Relative Strength Index (RSI): The RSI is currently at 76.35, placing it in the overbought territory. While this suggests that the index may be due for a short-term pullback, it also reflects strong upward momentum.

Outlook

As the week concludes, investors remain cautious, balancing strong corporate earnings against potential geopolitical uncertainties. The inauguration of the new U.S. administration brings potential market-moving executive orders, contributing to the cautious tone in global markets.

Latest market news

Today 06:50 PM

Today 03:00 PM

Today 12:00 PM

Today 10:00 AM

Latest DAX newsletter articles

January 15, 2025 08:58 AM

January 14, 2025 08:31 AM

January 13, 2025 09:23 AM

December 18, 2024 08:59 AM