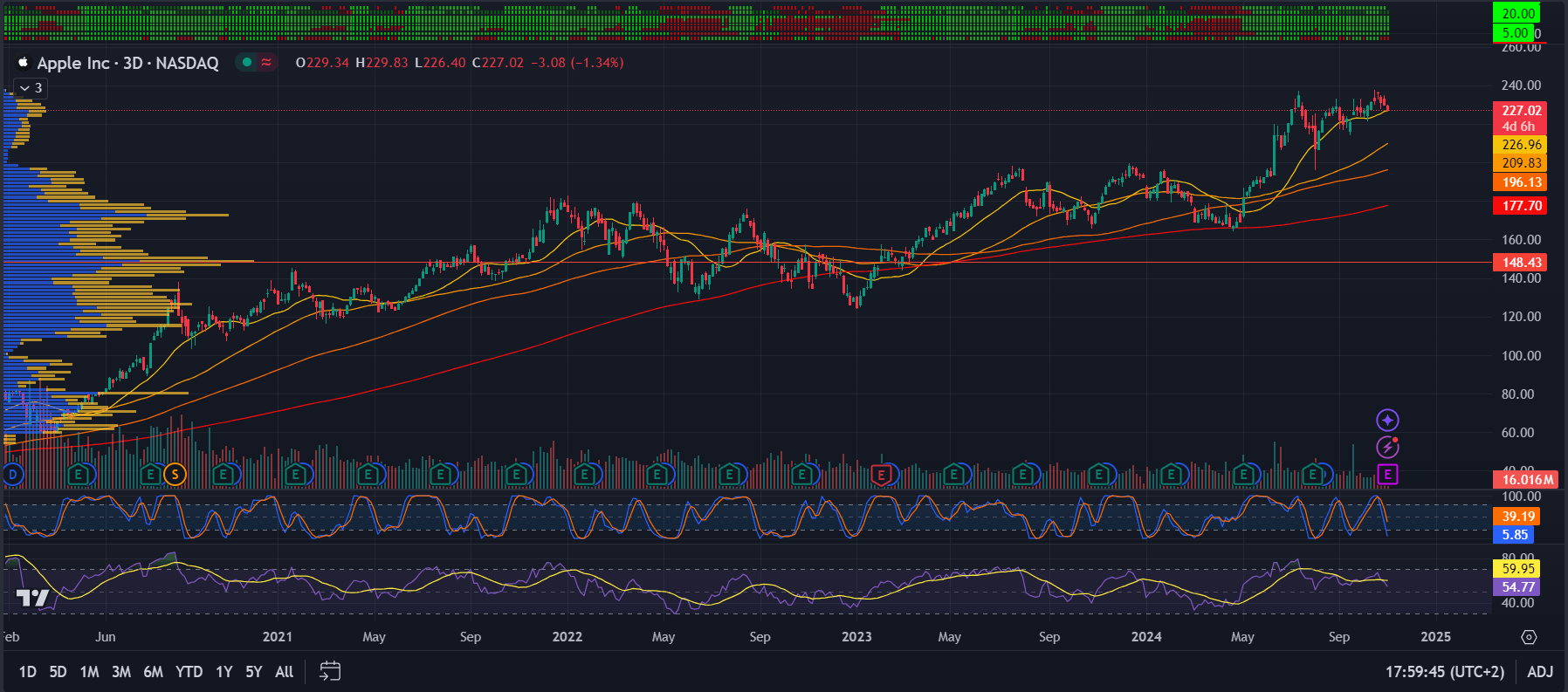

Apple Q3 2024 Earnings Preview

Earnings Release Date:

Thursday, October 31, after market close

Expected EPS: $1.60

Expected Revenue: $94.521 billion

Apple Inc. is set to announce its Q3 2024 earnings this Thursday, with analysts expecting a solid performance. Estimated earnings per share (EPS) are $1.60, with revenues projected to reach $94.521 billion. Apple’s last report in Q2 surprised on the upside, with EPS at $1.40 versus estimates of $1.34 and revenues of $85.777 billion, exceeding expectations of $84.433 billion. Over the past three months, Apple’s stock has increased by 10.63%, outperforming the S&P 500’s 5.19% gain.

Key Areas to Watch in Apple’s Q4 Earnings

- iPhone Revenue

iPhone sales remain Apple’s primary revenue driver. With approximately 10 days of sales from the new iPhone 16 lineup in Q3, expectations are for moderate growth in iPhone revenue. A larger impact from iPhone 16 sales and Apple Intelligence is anticipated in the next quarter as customers increasingly adopt iOS 18.1, which introduces AI-powered features like enhanced writing tools, photo editing, and summarized notifications, enhancing the appeal of the new devices. - Gross Margin Expansion

Apple’s gross margin has become an increasingly important factor, driven by high-margin services revenue and integration of hardware production. Modest gross margin expansion is expected compared to last year, reflecting the rising proportion of services income and Apple’s vertical hardware integration. - Services Revenue Growth

Services are Apple’s second-largest revenue segment, and the company is projected to report double-digit growth in this area. Apple’s robust ecosystem, encompassing software, hardware, and semiconductor integration, gives it a competitive edge and maintains strong returns on invested capital. - Capital Allocation

Apple’s strong cash flow continues to support capital returns to shareholders. With a net cash position of $51 billion as of September 2023, the company aims to progress toward its goal of becoming cash-neutral, although this may take several more years. Since announcing this goal in 2018, Apple has reduced its net cash position by over half.

Positives and Risks

- Positives: Apple’s in-house chip development has accelerated product innovation and differentiation, which is evident in its tightly integrated ecosystem of devices and services. This approach strengthens Apple’s competitive position and enhances profitability.

- Risks: Apple’s heavy reliance on consumer spending exposes it to competition and market cyclicality. Additionally, Apple’s supply chain is vulnerable to geopolitical risks due to its dependence on Foxconn for assembly and Taiwan Semiconductor Manufacturing (TSMC) for chips. Heightened tensions between the U.S. and China, or potential conflicts involving Taiwan, could severely impact Apple’s production capabilities. China’s recent recommendation for officials to avoid iPhones adds to the uncertainty surrounding Apple’s sales in this key market.

Conclusion

Apple’s Q3 2024 earnings are expected to be robust, with strong growth across iPhone sales, services, and gross margins. However, risks related to supply chain vulnerabilities and geopolitical tensions could pose challenges ahead. Investors will closely watch for updates on iPhone 16 sales performance and insights into Apple’s progress toward achieving cash-neutral status.

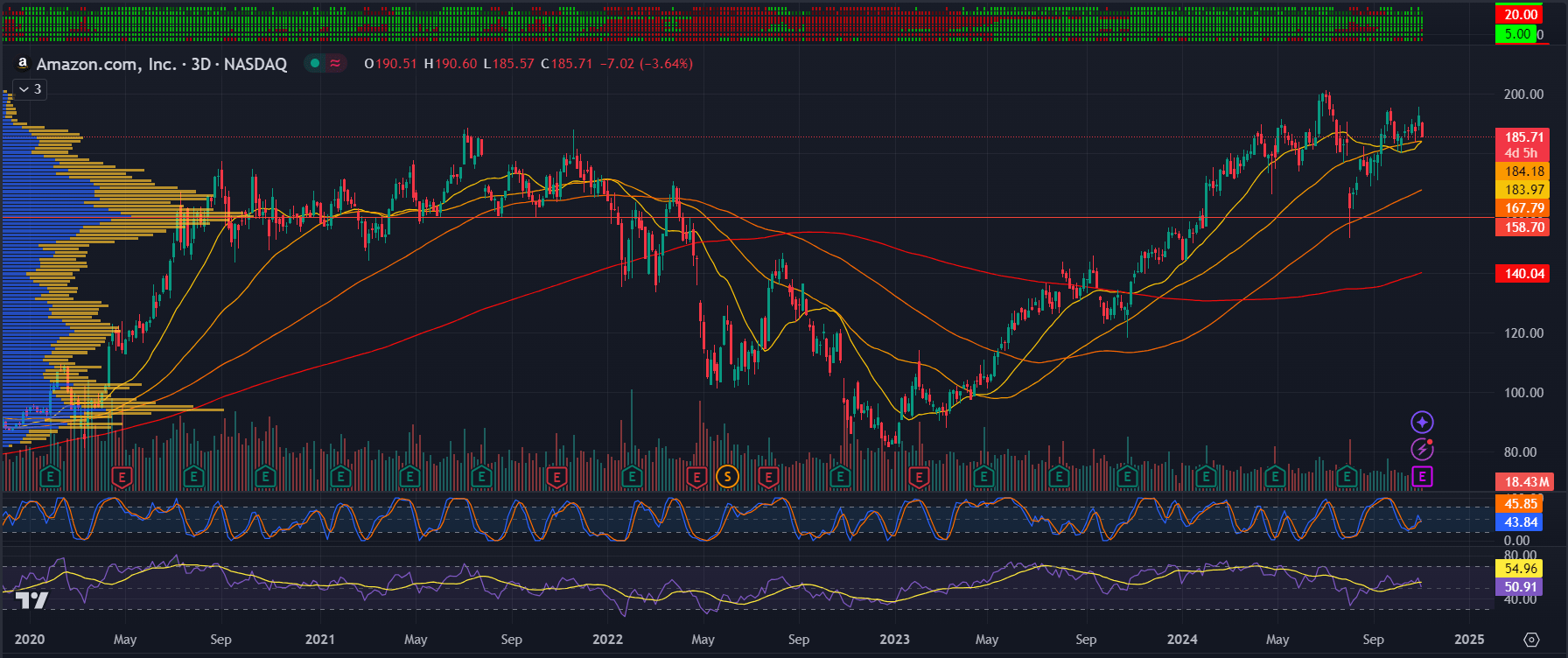

Amazon Q3 2024 Earnings Preview

Earnings Release Date: October 31, 2024 (After Market Close)

Expected EPS: $1.14 (+34.1% YoY)

Expected Revenue: $154 billion - $158 billion

Amazon.com, Inc. is set to release its Q3 2024 earnings report on October 31, 2024 after the market closes. Analysts are forecasting earnings per share (EPS) of $1.14, representing a 34.1% increase from the same quarter last year, when Amazon posted an EPS of $0.85. Revenues are expected to come in between $154 billion and $158 billion, translating to 9.5% growth at the midpoint. However, this revenue guidance fell short of Wall Street’s expectations for double-digit growth, raising some concerns ahead of the report.

Key Growth Drivers:

- AWS (Amazon Web Services): AWS continues to be Amazon’s primary profit driver, contributing $9.3 billion in operating income during Q2 2024, accounting for two-thirds of the company’s total profitability. AWS grew by 19% YoY last quarter, surpassing expectations. Investors will be watching closely to see if this strong growth continues in Q3, particularly as Amazon invests heavily in AI infrastructure through AWS.

- Advertising Revenue: While Amazon’s advertising revenue grew 20% YoY last quarter, it fell short of the 24% growth seen in the prior quarter. Analysts will be keen to see if this segment rebounds in Q3 or if growth continues to decelerate.

- E-Commerce and Prime Services: Amazon’s core e-commerce business, as well as its Prime Video segment, remains a key area of focus. The company is facing intense competition from rivals like Walmart and Alibaba, which could impact its market share and profit margins.

Concerns and Headwinds:

- Capital Expenditures (CapEx): Amazon’s CapEx surged 54% in the previous quarter, driven by investments in AI and data centers. CapEx reached $17.6 billion, raising concerns about how these expenditures may pressure profit margins in the near term.

- Competition: In addition to the cloud computing segment facing competition from Microsoft Azure and Google Cloud, Amazon’s e-commerce and entertainment segments are challenged by Walmart, Alibaba, TEMU, and other platforms. This competition could limit Amazon’s ability to maintain its dominant market position.

- Labor Relations: Ongoing labor issues and potential unionization efforts within Amazon’s warehouse workforce have raised concerns about operational disruptions and public perception. Strikes or increased activism could affect the company's delivery times and efficiency, especially during peak shopping seasons.

Q3 Earnings Outlook and Key Focus Areas:

- AWS Growth: Investors will closely monitor AWS, which has grown by double digits over the past four quarters. With Amazon holding a 32% market share in cloud services, the key question will be how long AWS can sustain this impressive growth.

- Cost Management and Margin Improvement: As Amazon continues to ramp up investments in AI and cloud computing, investors will want to see evidence of margin improvement or efficient cost management to ensure that heavy CapEx spending does not erode profitability.

Conclusion:

Amazon’s Q3 2024 earnings are expected to deliver strong year-over-year growth in both earnings and revenue, driven largely by AWS and its expanding role in the AI infrastructure space. However, concerns about capital expenditures, competition in core business segments, and labor relations may weigh on investor sentiment. As Amazon continues to diversify its revenue streams and focus on high-growth areas like cloud computing and AI, its ability to manage costs while maintaining market leadership will be key to sustaining its long-term growth trajectory.

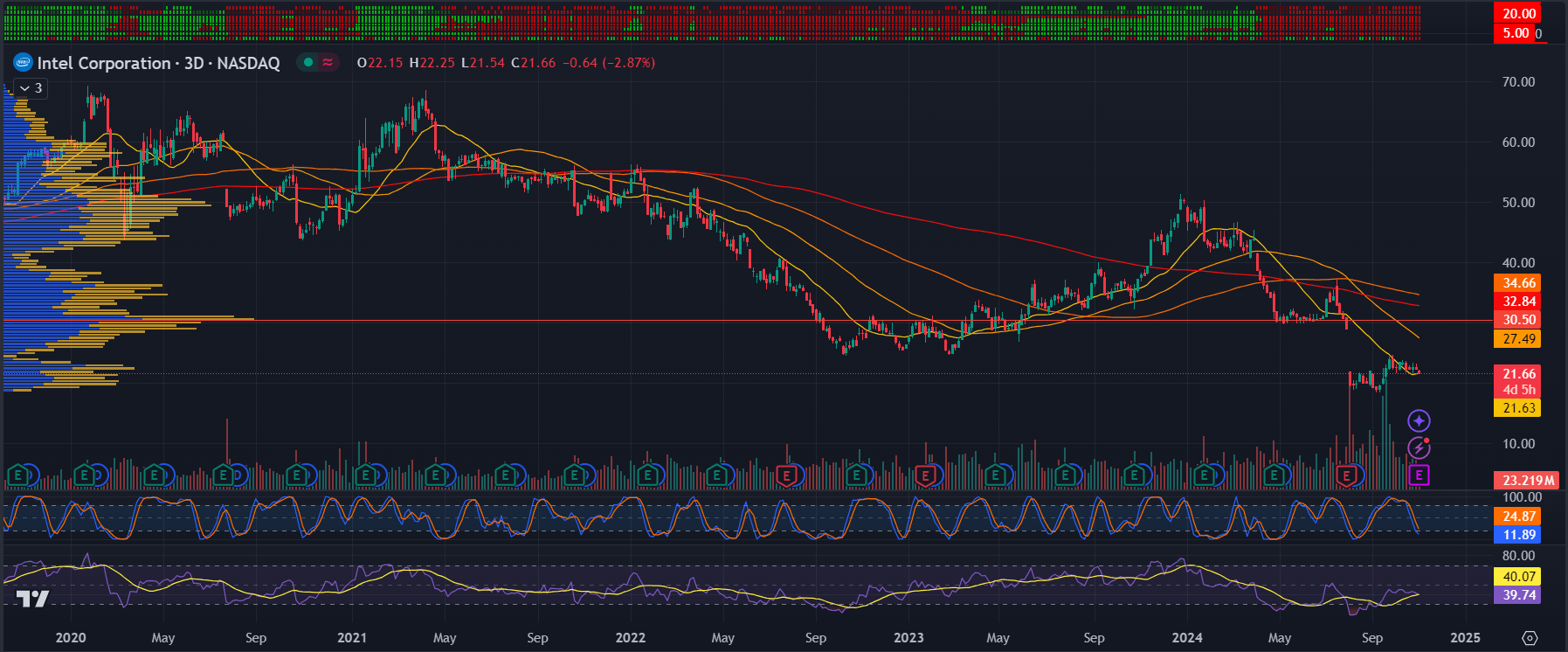

Intel Q3 2024 Earnings Preview

Earnings Release Date:

Tuesday, October 31, after market close

Expected EPS: -$0.02 (down from $0.02 in the last quarter)

Expected Revenue: $13.02 billion (up from $12.93 billion in the last quarter)

Intel Corporation will report its Q3 2024 earnings on October 31, with analysts projecting a loss of $0.02 per share. Revenue is expected to be $13.02 billion, reflecting a slight increase from the previous quarter’s $12.93 billion, but this still represents a 105% drop in earnings and an 8.1% decrease in revenue year-over-year. Intel’s share price has declined by 24.25% over the past three months, significantly underperforming the S&P 500’s 5.19% gain.

Intel is currently undergoing a challenging transition as it seeks to reposition itself as a foundry business, manufacturing chips for other companies. This transformation has led to layoffs and dividend suspensions over the past year as Intel manages the financial strain associated with this shift. Intel has even considered the possibility of selling off its foundry division due to the losses.

Key Positives for Intel:

- Government Support

Intel is set to receive up to $3 billion in funding from the U.S. CHIPS Act to support semiconductor manufacturing for national defense, which could provide valuable financial backing during its transformation. - Investment Confidence

Recent investments from financial institutions and Apollo’s interest in Intel shares signal long-term confidence in the company, despite current challenges. - Strategic Partnerships

Intel’s partnership with Amazon AWS to co-develop AI custom chips represents a promising growth opportunity. This multi-year, multi-billion dollar investment could strengthen Intel’s position in the AI chip market. - Intellectual Property and Patents

With a robust patent portfolio, Intel holds a competitive advantage, allowing it to protect its innovations and retain proprietary technology. - Customer Trust and Long-Term Contracts

Intel’s long-standing relationships with major tech companies help stabilize its revenue and create switching costs for customers, who may prefer not to change suppliers for critical applications.

Key Challenges for Intel:

- Financial Strain

Intel has a debt load of $53 billion and limited free cash flow, putting pressure on its ability to sustain investments and fund its transformation effectively. - Intense Market Competition

The semiconductor market is increasingly saturated, with competitors like AMD and NVIDIA gaining significant market share in CPUs and GPUs, respectively. New ARM-based chip manufacturers are also entering the scene, intensifying competition and pressuring Intel’s pricing and innovation. - Strategic Challenges

Intel faces a combination of competitive, financial, and strategic threats, with no immediate positive catalysts on the horizon. - Shareholder Dilution

Intel’s number of outstanding shares has increased by 2% in the past year, which can dilute shareholder value and reflects a reliance on equity to finance operations.

Conclusion

Intel’s Q3 earnings report will provide insights into how the company is navigating its foundry transformation amid ongoing financial and competitive challenges. While government support and strategic partnerships with companies like Amazon AWS offer a path forward, Intel’s reliance on debt and the fierce competition from rivals like AMD and NVIDIA remain significant obstacles. Investors will closely watch for any earnings surprises and indications of stability as Intel pursues its long-term vision.

Latest market news

Yesterday 07:55 PM

Yesterday 05:50 PM

Yesterday 05:30 PM

Yesterday 05:06 PM

Latest Tech articles

July 18, 2024 02:46 PM

June 4, 2024 03:00 PM

May 29, 2024 12:51 PM

March 21, 2024 04:05 AM