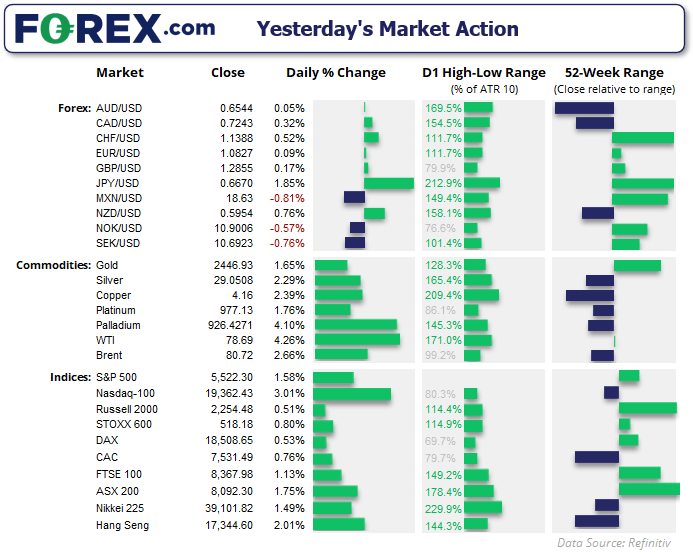

Wednesday was a day of divergent policies that saw the Bank of Japan (BOJ) hike rates more than expected and the Fed signal a cut.

The FOMC meeting went largely as expected, with rates being held at 5.25-5% and a 25bp rate cut being signalled for September. Jerome Powell told the press that there was a “real discussion” for cutting rates at this meeting despite the majority voting for a hold, upside risks to inflation had decreased and downside risks to employment were real. There was a lot of data upcoming, and that a September cut could be in play if inflation moved lower in line with expectations.

So unless incoming inflation data surprised wildly to the upside, the Fed’s cutting cycle should begin next month. And his dual combo of lowering inflation risks and raising concerns over employment made another cut this year more likely.

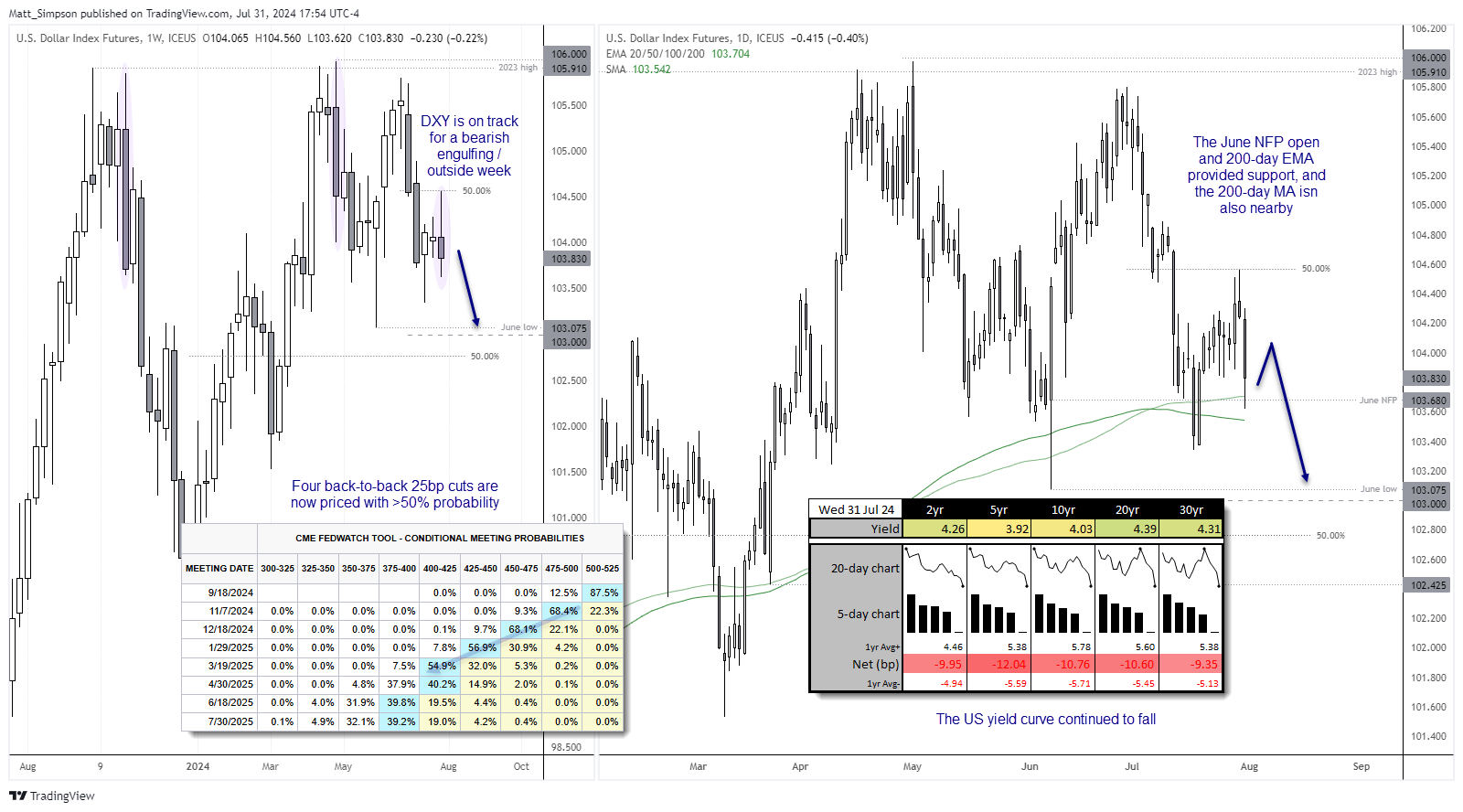

Fed fund futures have priced four back-to-back 25bp cuts between September and March meetings with a probability of over 50%, with a fifth cut in June at nearly 50%. The US yield curve continued to decline to drag the US dollar broadly lower against its FX peers.

The BOJ surprise 15bp hike (relative to the 10bp expected) sent USD/JPY below 149 for the first time since March during its most bearish day in three months. Their ‘detailed plan’ to taper their bond purchases was not as detailed as we’d have liked, but it is expected to be around reduced by half to 3 trillion yen by Q1 2026. This initially saw yen pairs wobble, but the dovish Fed meeting allowed the yen to continue rallying.

Yet AUD/USD only posted a marginal gain against the US dollar thanks to softer CPI data which has poured cold water on any expectations of another RBA hike. So while a bullish pinbar formed on the daily chart of AUD/USD, it is one of the least compelling setups for bulls as it is essentially pairing a currency pair without much if a divergent theme between central banks. RBA has the lower rate and Fed cuts will simply narrow the gap.

Wall Street indices and commodities rallied on the dovish Fed meeting and positive earnings from Meta and an bullish call on Nvidia. The S&P 500 rose to an 8-day high, the Nasdaq reached a 5-day high and the Dow Jones stopped just short of its record high before paring gains and closing the day with a shooting star candle.

WTI crude oil enjoyed its best day since October and rallied 4.3%, with gold, silver and copper all rising in line with yesterday’s bullish bias.

US dollar index technical analysis:

The US dollar index is now on track for a bearish engulfing / outside week. Its high perfectly respected a 50% retracement level to indicate a swing high has formed around 104.50 and momentum has turned lower on the daily chart. The US dollar index managed to hold above the June NFP open price (103.68) and 200-day EMA 103.70) but a soft set of ISM manufacturing and NFP data could see it continue lower, beneath the 200-day MA (103.54) and head for our bearish target around the June low (103.075).

Events in focus (AEDT)

- 09:00 – AU manufacturing PMI

- 11:30 – AU trade balance

- 11:45 – CN manufacturing PMI (Caixin)

- 16:30 – AU commodity prices

- 18:00 – EU manufacturing PMI

- 21:00 – BOE interest rate decision, MPC votes

- 22:30 – US jobless claims

- 23:15 – BOE Bailey speaks

- 00:00 – ISM manufacturing PMI

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Yesterday 07:31 PM

Latest articles

Today 12:31 AM

Yesterday 10:31 PM

December 19, 2024 10:26 PM

December 18, 2024 10:16 PM