US Dollar Talking Points:

- The USD has had a rough Q3, with a massive push driven by the initial stages of carry unwind in USD/JPY, and more recently from bulls testing breakouts in EUR/USD following a massive breakout in GBP/USD.

- There are some possible items of interest for contrarians, however, and in this article, I’m going to investigate that from the perspective of the longer-term look at the US Dollar and its largest constituent of the Euro.

- I’ll be going over these setups in the weekly webinar, held each Tuesday at 11am ET: Click here for registration information.

It’s been a rough Q3 for the US Dollar as the currency has seemed to get hit from multiple sides. It was the first seven weeks of the quarter that were especially brutal as the USD/JPY carry trade started to unwind.

And there was good reason for that, too, as the Federal Reserve was moving closer and closer to rate cuts, which would narrow the rate divergence between the economies represented in the pair. It was that carry trade that had driven USD/JPY to 37-year highs and given the fact that the JPY is a 13.6% allocation in the DXY basket, that similarly helped the Dollar to put in a massive topside move in 2021 and 2022.

But sellers hit quickly after the Q3 open and soon after, the US Dollar did something it hadn’t done since January of 2018, with RSI on the weekly chart going into oversold territory. I talked about this in the webinar at the time and looking at that prior instance, it can take time for such a forceful move to start to turn. In that prior instance, it took about three months before bulls took over and that’s not to fault bears for not trying, as a fresh yearly low was set a couple of weeks after the oversold signal. But notably, that produced a higher-low via RSI to illustrate a case of divergence.

And I must disclaim this right up front: Just because RSI moved into oversold territory it does not mean that the dollar has to turn. RSI is a lagging indicator, and it’s not predictive at all. It does, however, highlight important context and that should be enough to produce more questions when investigating projections, which I’ll dig deeper into below.

US Dollar Weekly Price Chart

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

The US Dollar: Composition Matters

The US Dollar via the DXY contract is a rather unique instrument, and I think many fail to give that the credit that it deserves. The USD is merely a composite of underlying currencies, as I had explained in the US Dollar Reserve Currency article; and the largest two components of that are the Euro and the Japanese Yen.

This impact on trading, especially for shorter-term themes, can be immense. That means we could get some really great news out of the US yet it causes the Dollar to trade lower. Or perhaps there could be some really bad news but the Dollar trades higher. The bigger question in each count is how that news impacts Europe and Japan along with overall global macro. But, this is key for our discussion in today’s article.

When the USD stretches to such depths as oversold or overbought on the weekly chart, there’s something profound taking place as we’re also seeing similarly stretched moves press in currencies such as the Euro and/or the Japanese Yen; and the DXY basket is merely a reflection of that.

For Q3 of this year that impact is obvious, as we had the initial stages of carry unwind from the USD/JPY carry trade pushing both USD/JPY and DXY lower. This is something that could continue in Q4 as there’s likely more carry trade left to unwind, as we haven’t yet seen the 38.2% retracement of the trend produced by that theme taken-out.

But the bigger question there is timing.

With the Fed cutting rates and the BoJ talking about more possible rate hikes, that could further compress the rate divergence in the USD/JPY pair, thereby leading to even more motivation for longer-term longs to scale out of that trade. And as we saw in Q3 that could have an incredibly forceful impact in both markets.

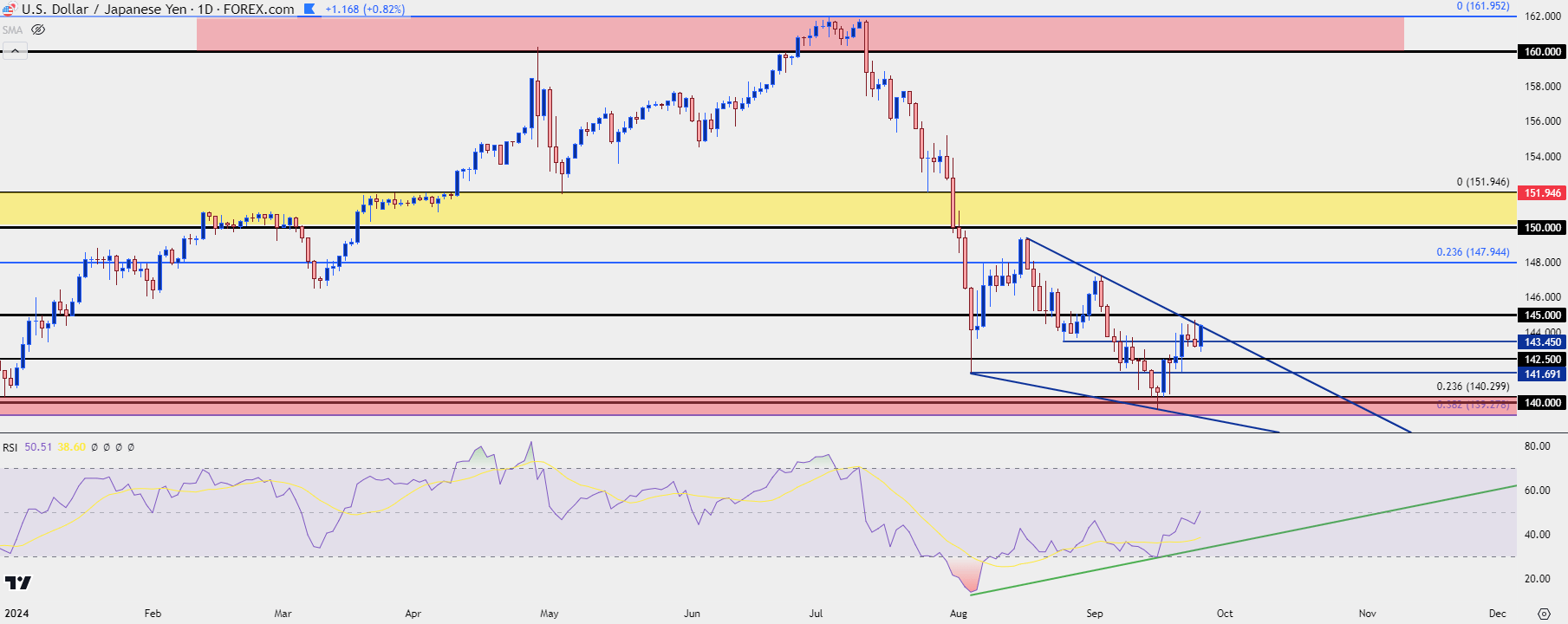

But at this stage USD/JPY is holding on to near-term bullish potential as the pair held a test of the 140.00 support zone after last week’s open, and since the FOMC rate cut there’s been a build of bullish context in the pair.

There’s also a falling wedge formation which is often approached with aim of bullish reversal. The resistance side of that formation has already been tested but buyers haven’t been able to drive through, not yet at least.

If they can, the move would seemingly come at odds to the fundamental backdrop but that’s not necessarily a surprise, especially considering the more-forceful impact of sentiment. It takes buyers and sellers, supply, and demand to push prices. While fundamentals will often have a push on that dynamic, if a market is deeply oversold, such as we saw in USD/JPY’s daily chart in August, it’s rationale to think there could be more room for the pullback to run.

As of right now there’s also a case of RSI divergence on the daily chart as price tests resistance in the falling wedge, both items that could point the potential for a larger retracement.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

The Euro

The Euro is the largest component of DXY at 57.6% and, like I mentioned above, I’m dubious about any direct relationships to price from fundamentals and this is another illustration of that.

EUR/USD has been in a strong up-trend through Q3 and if we look at the underlying fundamentals there’s not a great explanation for that. The European Central Bank continues to cut rates, and will probably need to continue doing so alongside the Fed. Yet, if we look at the chart which set yet another fresh yearly high this morning, there’s little rationale to explain the trend.

This is something that could take on more attention in Q4, especially if we are going to see a USD bullish backdrop develop after those oversold conditions showed on the longer-term chart in August.

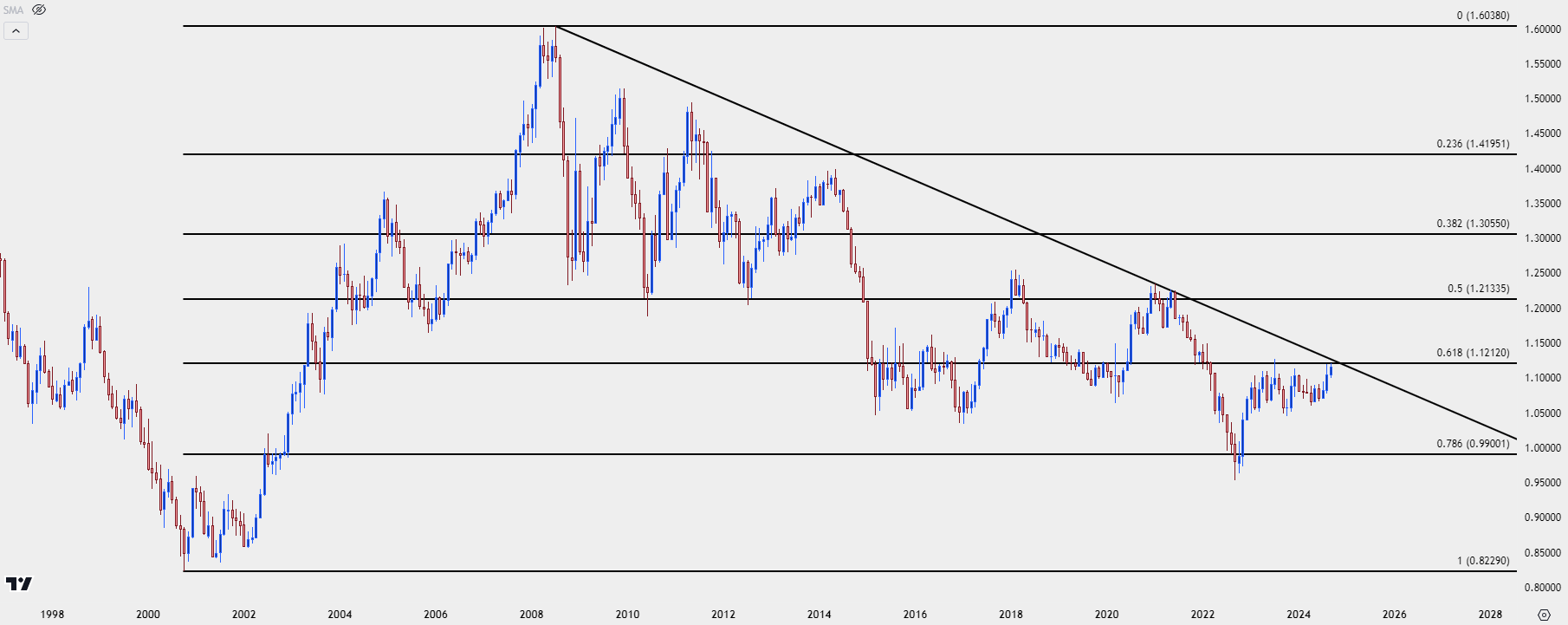

There’s also a long-term resistance level now in-play on the pair. Below I’m looking at the monthly chart of EUR/USD and the 1.1212 price has had an impact on price action in numerous ways over the past decade.

EUR/USD Monthly Price Chart

Chart prepared by James Stanley, EUR/USD on Tradingview

Chart prepared by James Stanley, EUR/USD on Tradingview

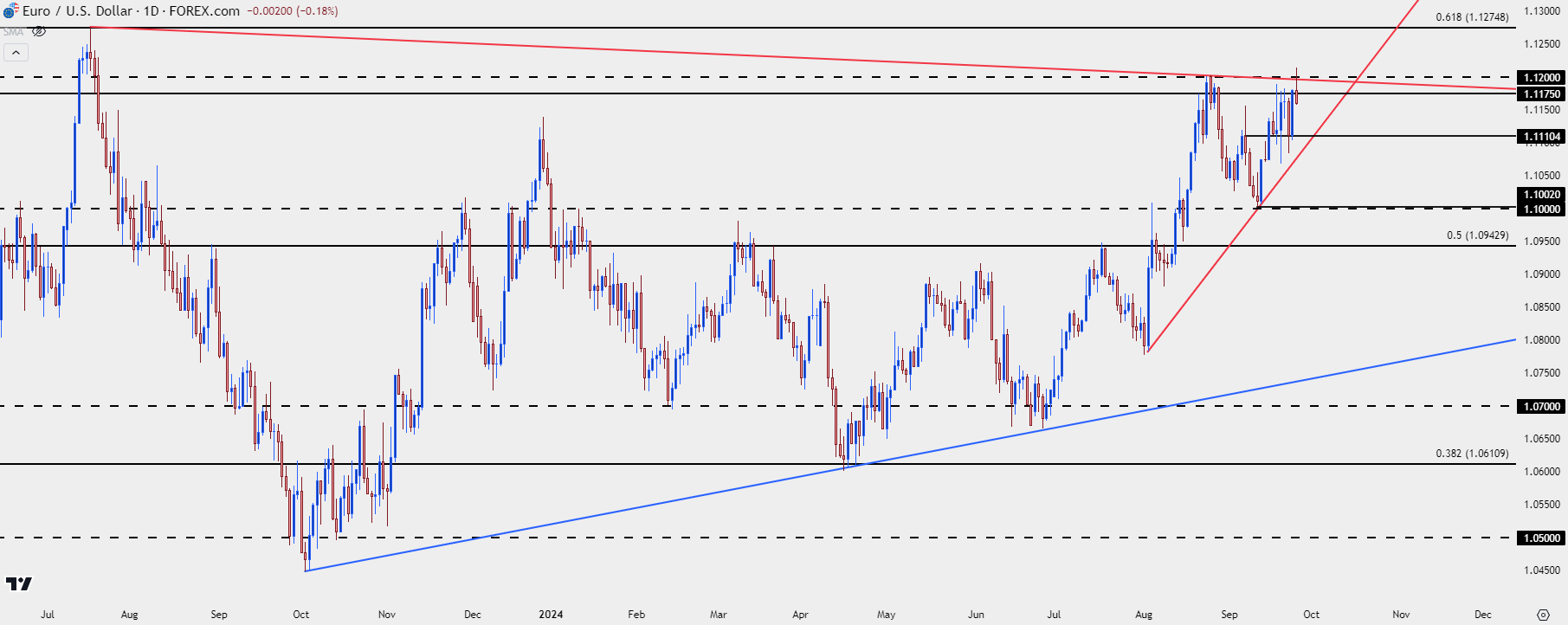

In yesterday’s webinar I spoke of possible ‘capitulation scenarios’ in EUR/USD in the event that buyers didn’t show up to support fresh highs. And that’s something that can remain of interest, and likely something that would need to come into play for the US Dollar to hold above the yearly high that was defended earlier this morning.

At this point, we can see the early stages of what might turn out to be a capitulation scenario. EUR/USD broke out to a fresh yearly high this morning before finding resistance at 1.1212, and since then prices have start to pull back.

It’s still too early to say for certain that this is what we have but if sellers can defend this morning’s high, while driving through support at 1.1110, that scenario will start to look more attractive.

Below that, the 1.1000 psychological level was well-defended ahead of the ECB’s rate cut and that similarly retains some interest. And below that, 1.0943 comes into the picture as this is the 50% mark from the same Fibonacci retracement that set last year’s high at 1.1275 (the 61.8% retracement) and, so far, this year’s low at 1.0611 (the 38.2% retracement).

If bears can produce that – defense of the high, and then tests through those supports – the intermediate-term would appear as though we have range continuation in EUR/USD, which could further point to a similar theme in USD and that would keep the door open for bigger picture bounces in the US Dollar.

EUR/USD Daily Price Chart

Chart prepared by James Stanley, EUR/USD on Tradingview

Chart prepared by James Stanley, EUR/USD on Tradingview

--- written by James Stanley, Senior Strategist

US Dollar Talking Points:

- The USD has had a rough Q3, with a massive push driven by the initial stages of carry unwind in USD/JPY, and more recently from bulls testing breakouts in EUR/USD following a massive breakout in GBP/USD.

- There are some possible items of interest for contrarians, however, and in this article, I’m going to investigate that from the perspective of the longer-term look at the US Dollar and its largest constituent of the Euro.

It’s been a rough Q3 for the US Dollar as the currency has seemed to get hit from multiple sides. It was the first seven weeks of the quarter that were especially brutal as the USD/JPY carry trade started to unwind.

And there was good reason for that, too, as the Federal Reserve was moving closer and closer to rate cuts, which would narrow the rate divergence between the economies represented in the pair. It was that carry trade that had driven USD/JPY to 37-year highs and given the fact that the JPY is a 13.6% allocation in the DXY basket, that similarly helped the Dollar to put in a massive topside move in 2021 and 2022.

But sellers hit quickly after the Q3 open and soon after, the US Dollar did something it hadn’t done since January of 2018, with RSI on the weekly chart going into oversold territory. I talked about this in the webinar at the time and looking at that prior instance, it can take time for such a forceful move to start to turn. In that prior instance, it took about three months before bulls took over and that’s not to fault bears for not trying, as a fresh yearly low was set a couple of weeks after the oversold signal. But notably, that produced a higher-low via RSI to illustrate a case of divergence.

And I must disclaim this right up front: Just because RSI moved into oversold territory it does not mean that the dollar has to turn. RSI is a lagging indicator, and it’s not predictive at all. It does, however, highlight important context and that should be enough to produce more questions when investigating projections, which I’ll dig deeper into below.

US Dollar Weekly Price Chart

Chart prepared by James Stanley; data derived from Tradingview

The US Dollar: Composition Matters

The US Dollar via the DXY contract is a rather unique instrument, and I think many fail to give that the credit that it deserves. The USD is merely a composite of underlying currencies, as I had explained in the US Dollar Reserve Currency article; and the largest two components of that are the Euro and the Japanese Yen.

This impact on trading, especially for shorter-term themes, can be immense. That means we could get some really great news out of the US yet it causes the Dollar to trade lower. Or perhaps there could be some really bad news but the Dollar trades higher. The bigger question in each count is how that news impacts Europe and Japan along with overall global macro. But, this is key for our discussion in today’s article.

When the USD stretches to such depths as oversold or overbought on the weekly chart, there’s something profound taking place as we’re also seeing similarly stretched moves press in currencies such as the Euro and/or the Japanese Yen; and the DXY basket is merely a reflection of that.

For Q3 of this year that impact is obvious, as we had the initial stages of carry unwind from the USD/JPY carry trade pushing both USD/JPY and DXY lower. This is something that could continue in Q4 as there’s likely more carry trade left to unwind, as we haven’t yet seen the 38.2% retracement of the trend produced by that theme taken-out.

But the bigger question there is timing.

With the Fed cutting rates and the BoJ talking about more possible rate hikes, that could further compress the rate divergence in the USD/JPY pair, thereby leading to even more motivation for longer-term longs to scale out of that trade. And as we saw in Q3 that could have an incredibly forceful impact in both markets.

But at this stage USD/JPY is holding on to near-term bullish potential as the pair held a test of the 140.00 support zone after last week’s open, and since the FOMC rate cut there’s been a build of bullish context in the pair.

There’s also a falling wedge formation which is often approached with aim of bullish reversal. The resistance side of that formation has already been tested but buyers haven’t been able to drive through, not yet at least.

If they can, the move would seemingly come at odds to the fundamental backdrop but that’s not necessarily a surprise, especially considering the more-forceful impact of sentiment. It takes buyers and sellers, supply, and demand to push prices. While fundamentals will often have a push on that dynamic, if a market is deeply oversold, such as we saw in USD/JPY’s daily chart in August, it’s rationale to think there could be more room for the pullback to run.

As of right now there’s also a case of RSI divergence on the daily chart as price tests resistance in the falling wedge, both items that could point the potential for a larger retracement.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

The Euro

The Euro is the largest component of DXY at 57.6% and, like I mentioned above, I’m dubious about any direct relationships to price from fundamentals and this is another illustration of that.

EUR/USD has been in a strong up-trend through Q3 and if we look at the underlying fundamentals there’s not a great explanation for that. The European Central Bank continues to cut rates, and will probably need to continue doing so alongside the Fed. Yet, if we look at the chart which set yet another fresh yearly high this morning, there’s little rationale to explain the trend.

This is something that could take on more attention in Q4, especially if we are going to see a USD bullish backdrop develop after those oversold conditions showed on the longer-term chart in August.

There’s also a long-term resistance level now in-play on the pair. Below I’m looking at the monthly chart of EUR/USD and the 1.1212 price has had an impact on price action in numerous ways over the past decade.

EUR/USD Monthly Price Chart

Chart prepared by James Stanley, EUR/USD on Tradingview

In yesterday’s webinar I spoke of possible ‘capitulation scenarios’ in EUR/USD in the event that buyers didn’t show up to support fresh highs. And that’s something that can remain of interest, and likely something that would need to come into play for the US Dollar to hold above the yearly high that was defended earlier this morning.

At this point, we can see the early stages of what might turn out to be a capitulation scenario. EUR/USD broke out to a fresh yearly high this morning before finding resistance at 1.1212, and since then prices have start to pull back.

It’s still too early to say for certain that this is what we have but if sellers can defend this morning’s high, while driving through support at 1.1110, that scenario will start to look more attractive.

Below that, the 1.1000 psychological level was well-defended ahead of the ECB’s rate cut and that similarly retains some interest. And below that, 1.0943 comes into the picture as this is the 50% mark from the same Fibonacci retracement that set last year’s high at 1.1275 (the 61.8% retracement) and, so far, this year’s low at 1.0611 (the 38.2% retracement).

If bears can produce that – defense of the high, and then tests through those supports – the intermediate-term would appear as though we have range continuation in EUR/USD, which could further point to a similar theme in USD and that would keep the door open for bigger picture bounces in the US Dollar.

EUR/USD Daily Price Chart

Chart prepared by James Stanley, EUR/USD on Tradingview

--- written by James Stanley, Senior Strategist

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Latest articles

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM