For about a month the logical scenario had started to play out. But, along with it came considerable collateral damage and suddenly several major publications were talking about the carry trade; or, more precisely, the unwind of the carry trade that was being accused of a de-leveraging driver across global equity markets.

When the carry trade is in-force it can be one of the most attractive venues in any market, especially for FX traders. The interest rate differential can allow for near-daily rollover payments, so, like a dividend but more frequent. And as others crowd that side of the trade to buy the higher-yielding currency while selling the lower-yielder, a trend can develop in that direction, allowing for principal gains on top of the swap or rollover earned.

In USD/JPY this started back in 2021, well before the Fed started hiking rates. The simple act of US CPI moving higher was enough to drive anticipation of eventual rate hikes from the Fed, which started to push the long side of the pair. When the Fed began to open the door to hikes in Q4 of 2021, USD/JPY got a boost; and another larger boost in March of 2022 as the Fed began to hike rates. This was the initial build of the carry trade and for USD/JPY, it drove the pair from below 105 in early-2021 to 150.00 in Q4 of 2022.

The carry trade was so logical and clear that other problems started to percolate. The Japanese Ministry of Finance worried about the repercussions of unchecked Yen-weakness, so they intervened in Q4 of that year to try to balance the matter. Because the move had become so incredibly one-sided the corresponding pullback was fast and aggressive with USD/JPY shedding more than 2400 pips in just a few short months. This was 50% of the prior bullish trend, and it held support in early 2023 as buyers jumped back on the long side of the pair, in the direction of the carry.

In November of that year, the same prior high was already back in-play at 151.95. And, again, worries began to show around the Japanese Ministry of Finance around the consequences of unchecked Yen-weakness. And much like we saw the year before a sell-off developed with that price holding as the yearly high. But this time the sell-off was less severe as price only retraced 23.6% of the 2021-2022 major move.

USD/JPY Weekly Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

2024

As we came into 2024 it was still unclear as to whether the Fed would be able to cut rates, as this is something that would have a direct impact on the interest rate differential between Japan and the U.S. and in-turn, the carry trade.

We can see USD/JPY price action mirroring rate cut hopes or expectations in the US quite well earlier in the year. As inflation remained high, USD/JPY pushed right back up to the same 151.95 level that had held the highs for the prior two years. In April, just after an above-expected US CPI release, USD/JPY broke out above that price, setting a fresh 33-year high in the process.

It didn’t take long for USD/JPY to ascend to the next major psychological level of 160.00, which was in-play just a few weeks later. But, again, worries from the Japanese Finance Ministry drove an intervention that entailed USD-selling and JPY-buying from the Bank of Japan in effort of producing a reversal in the pair.

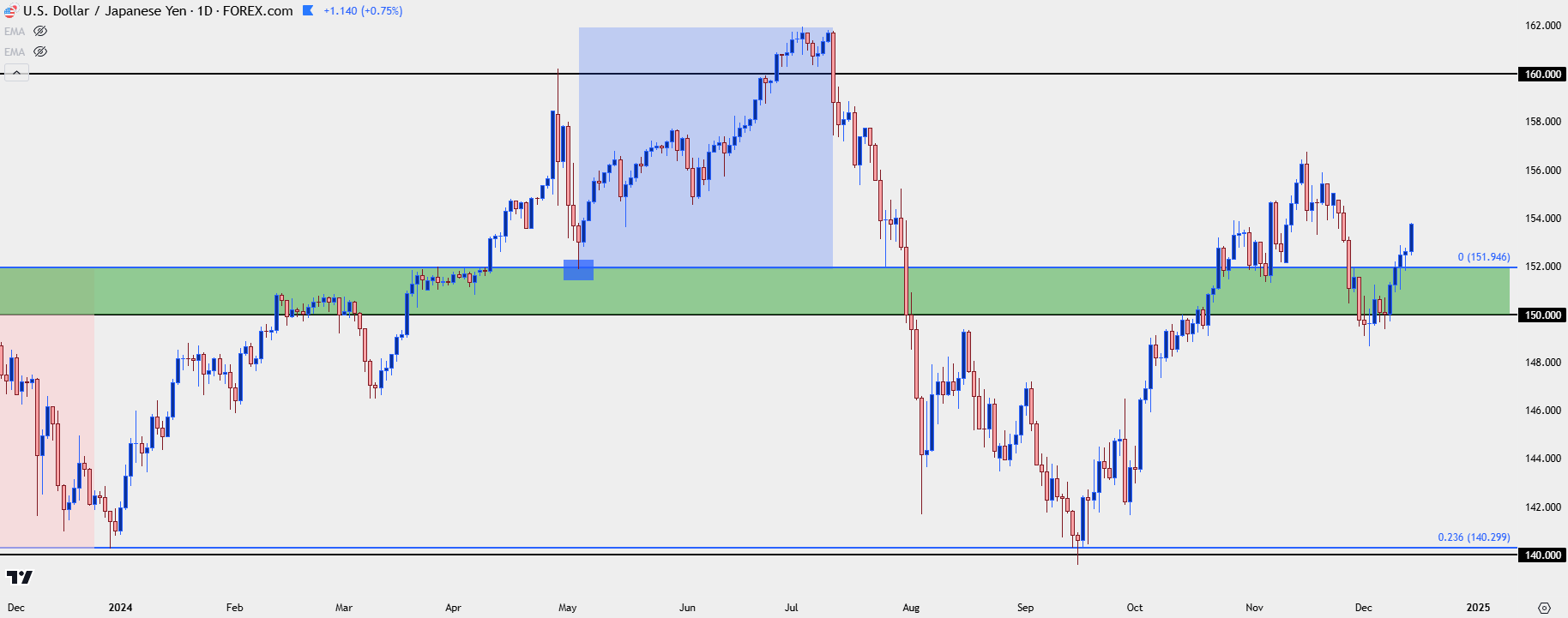

That’s when the 151.95 level came in as support. And then bulls did the same thing they had done for much of the prior three years, they priced in the direction of the rate differential. In June USD/JPY was back above the 160.00 level again, and that strength held into July.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

Carry Comes Undone

It was the morning of July 11th when matters began to unravel. That was the morning of a US CPI print and this time, the data came in below expectations. This gave hope that the Fed would actually be able to cut rates and along with that would be rate compression between the US and Japan, a factor that would not be positive for carry traders on the long side of the pair.

But that didn’t seem to be enough for the Bank of Japan as they also intervened that morning. And while prior intervention efforts fell flat as carry traders were there to buy support and push the bullish trend, this time there was the worry that the carry trade was over.

And when you have a crowded trade that’s starting to unwind, the smelling smoke in the crowded movie theater example comes to mind, where you might not want to wait around as the exit door is only so wide.

USD/JPY showed an aggressive sell-off that spanned into August and along the way global equities took a major hit as well, with many fingers being pointed at the Bank of Japan and the unwind of the carry trade as a culprit behind the volatility. But what doesn’t match in that scenario is the fact that the S&P 500 hit a fresh high the week after the CPI print, after USD/JPY had started to reverse. So while the unwind of the carry may have removed some leverage from global equity markets, it’s unlikely that it was the sole culprit of the sell-off.

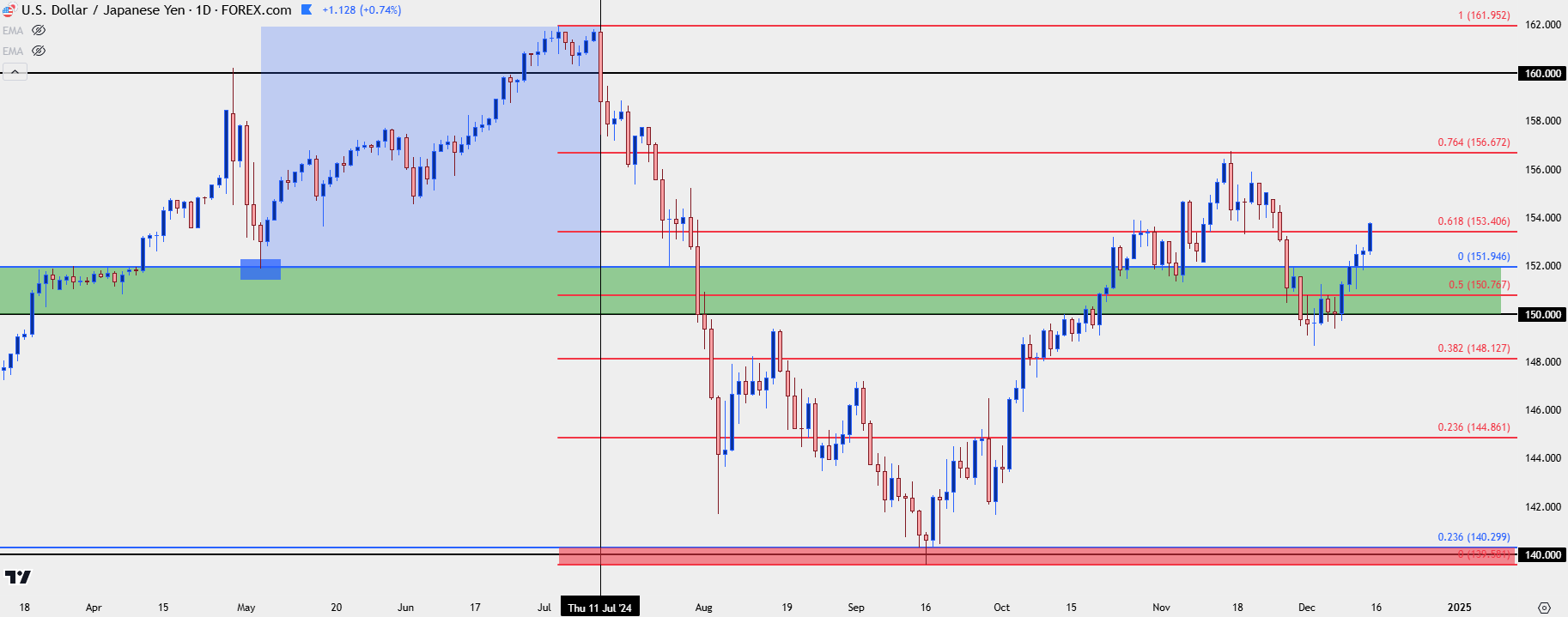

Now on to the surprise: In the month of September as the Fed was preparing to cut rates, the move in USD/JPY had started to stall. There was one single morning of tests below the 140.00 handle, but like we saw in the US Dollar in Q4, a massive reversal developed; and for USD/JPY, that entailed a 76.4% retracement of the July-September sell-off.

I’m surprised at how aggressively that move priced-in, and the degree to which the sell-off had retraced. I was expecting carry unwind to come back on a re-test of the 150.00 level, or perhaps even the 151.95 price. But that didn’t happen as the post-election run in the Greenback simply drove the USD and related pairings to fresh highs.

But, with that said, this story isn’t over yet, and USD/JPY remains a hot button for 2025 trade, especially if the US Dollar is going to remain within its longer-term mean-reverting backdrop. It was the 140.00 level that stifled sellers in September, leading to the reversal that showed in Q4. And that’s the area that bears will need to take-out if they want to drive a larger reversal in the pair while unwinding the carry trade that built into and around the FOMC’s rate hike campaign of 2022 and 2023.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

--- written by James Stanley, Senior Strategist

For about a month the logical scenario had started to play out. But, along with it came considerable collateral damage and suddenly several major publications were talking about the carry trade; or, more precisely, the unwind of the carry trade that was being accused of a de-leveraging driver across global equity markets.

When the carry trade is in-force it can be one of the most attractive venues in any market, especially for FX traders. The interest rate differential can allow for near-daily rollover payments, so, like a dividend but more frequent. And as others crowd that side of the trade to buy the higher-yielding currency while selling the lower-yielder, a trend can develop in that direction, allowing for principal gains on top of the swap or rollover earned.

In USD/JPY this started back in 2021, well before the Fed started hiking rates. The simple act of US CPI moving higher was enough to drive anticipation of eventual rate hikes from the Fed, which started to push the long side of the pair. When the Fed began to open the door to hikes in Q4 of 2021, USD/JPY got a boost; and another larger boost in March of 2022 as the Fed began to hike rates. This was the initial build of the carry trade and for USD/JPY, it drove the pair from below 105 in early-2021 to 150.00 in Q4 of 2022.

The carry trade was so logical and clear that other problems started to percolate. The Japanese Ministry of Finance worried about the repercussions of unchecked Yen-weakness, so they intervened in Q4 of that year to try to balance the matter. Because the move had become so incredibly one-sided the corresponding pullback was fast and aggressive with USD/JPY shedding more than 2400 pips in just a few short months. This was 50% of the prior bullish trend, and it held support in early 2023 as buyers jumped back on the long side of the pair, in the direction of the carry.

In November of that year, the same prior high was already back in-play at 151.95. And, again, worries began to show around the Japanese Ministry of Finance around the consequences of unchecked Yen-weakness. And much like we saw the year before a sell-off developed with that price holding as the yearly high. But this time the sell-off was less severe as price only retraced 23.6% of the 2021-2022 major move.

USD/JPY Weekly Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

2024

As we came into 2024 it was still unclear as to whether the Fed would be able to cut rates, as this is something that would have a direct impact on the interest rate differential between Japan and the U.S. and in-turn, the carry trade.

We can see USD/JPY price action mirroring rate cut hopes or expectations in the US quite well earlier in the year. As inflation remained high, USD/JPY pushed right back up to the same 151.95 level that had held the highs for the prior two years. In April, just after an above-expected US CPI release, USD/JPY broke out above that price, setting a fresh 33-year high in the process.

It didn’t take long for USD/JPY to ascend to the next major psychological level of 160.00, which was in-play just a few weeks later. But, again, worries from the Japanese Finance Ministry drove an intervention that entailed USD-selling and JPY-buying from the Bank of Japan in effort of producing a reversal in the pair.

That’s when the 151.95 level came in as support. And then bulls did the same thing they had done for much of the prior three years, they priced in the direction of the rate differential. In June USD/JPY was back above the 160.00 level again, and that strength held into July.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Carry Comes Undone

It was the morning of July 11th when matters began to unravel. That was the morning of a US CPI print and this time, the data came in below expectations. This gave hope that the Fed would actually be able to cut rates and along with that would be rate compression between the US and Japan, a factor that would not be positive for carry traders on the long side of the pair.

But that didn’t seem to be enough for the Bank of Japan as they also intervened that morning. And while prior intervention efforts fell flat as carry traders were there to buy support and push the bullish trend, this time there was the worry that the carry trade was over.

And when you have a crowded trade that’s starting to unwind, the smelling smoke in the crowded movie theater example comes to mind, where you might not want to wait around as the exit door is only so wide.

USD/JPY showed an aggressive sell-off that spanned into August and along the way global equities took a major hit as well, with many fingers being pointed at the Bank of Japan and the unwind of the carry trade as a culprit behind the volatility. But what doesn’t match in that scenario is the fact that the S&P 500 hit a fresh high the week after the CPI print, after USD/JPY had started to reverse. So while the unwind of the carry may have removed some leverage from global equity markets, it’s unlikely that it was the sole culprit of the sell-off.

Now on to the surprise: In the month of September as the Fed was preparing to cut rates, the move in USD/JPY had started to stall. There was one single morning of tests below the 140.00 handle, but like we saw in the US Dollar in Q4, a massive reversal developed; and for USD/JPY, that entailed a 76.4% retracement of the July-September sell-off.

I’m surprised at how aggressively that move priced-in, and the degree to which the sell-off had retraced. I was expecting carry unwind to come back on a re-test of the 150.00 level, or perhaps even the 151.95 price. But that didn’t happen as the post-election run in the Greenback simply drove the USD and related pairings to fresh highs.

But, with that said, this story isn’t over yet, and USD/JPY remains a hot button for 2025 trade, especially if the US Dollar is going to remain within its longer-term mean-reverting backdrop. It was the 140.00 level that stifled sellers in September, leading to the reversal that showed in Q4. And that’s the area that bears will need to take-out if they want to drive a larger reversal in the pair while unwinding the carry trade that built into and around the FOMC’s rate hike campaign of 2022 and 2023.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

--- written by James Stanley, Senior Strategist

For about a month the logical scenario had started to play out. But, along with it came considerable collateral damage and suddenly several major publications were talking about the carry trade; or, more precisely, the unwind of the carry trade that was being accused of a de-leveraging driver across global equity markets.

When the carry trade is in-force it can be one of the most attractive venues in any market, especially for FX traders. The interest rate differential can allow for near-daily rollover payments, so, like a dividend but more frequent. And as others crowd that side of the trade to buy the higher-yielding currency while selling the lower-yielder, a trend can develop in that direction, allowing for principal gains on top of the swap or rollover earned.

In USD/JPY this started back in 2021, well before the Fed started hiking rates. The simple act of US CPI moving higher was enough to drive anticipation of eventual rate hikes from the Fed, which started to push the long side of the pair. When the Fed began to open the door to hikes in Q4 of 2021, USD/JPY got a boost; and another larger boost in March of 2022 as the Fed began to hike rates. This was the initial build of the carry trade and for USD/JPY, it drove the pair from below 105 in early-2021 to 150.00 in Q4 of 2022.

The carry trade was so logical and clear that other problems started to percolate. The Japanese Ministry of Finance worried about the repercussions of unchecked Yen-weakness, so they intervened in Q4 of that year to try to balance the matter. Because the move had become so incredibly one-sided the corresponding pullback was fast and aggressive with USD/JPY shedding more than 2400 pips in just a few short months. This was 50% of the prior bullish trend, and it held support in early 2023 as buyers jumped back on the long side of the pair, in the direction of the carry.

In November of that year, the same prior high was already back in-play at 151.95. And, again, worries began to show around the Japanese Ministry of Finance around the consequences of unchecked Yen-weakness. And much like we saw the year before a sell-off developed with that price holding as the yearly high. But this time the sell-off was less severe as price only retraced 23.6% of the 2021-2022 major move.

USD/JPY Weekly Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

2024

As we came into 2024 it was still unclear as to whether the Fed would be able to cut rates, as this is something that would have a direct impact on the interest rate differential between Japan and the U.S. and in-turn, the carry trade.

We can see USD/JPY price action mirroring rate cut hopes or expectations in the US quite well earlier in the year. As inflation remained high, USD/JPY pushed right back up to the same 151.95 level that had held the highs for the prior two years. In April, just after an above-expected US CPI release, USD/JPY broke out above that price, setting a fresh 33-year high in the process.

It didn’t take long for USD/JPY to ascend to the next major psychological level of 160.00, which was in-play just a few weeks later. But, again, worries from the Japanese Finance Ministry drove an intervention that entailed USD-selling and JPY-buying from the Bank of Japan in effort of producing a reversal in the pair.

That’s when the 151.95 level came in as support. And then bulls did the same thing they had done for much of the prior three years, they priced in the direction of the rate differential. In June USD/JPY was back above the 160.00 level again, and that strength held into July.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Carry Comes Undone

It was the morning of July 11th when matters began to unravel. That was the morning of a US CPI print and this time, the data came in below expectations. This gave hope that the Fed would actually be able to cut rates and along with that would be rate compression between the US and Japan, a factor that would not be positive for carry traders on the long side of the pair.

But that didn’t seem to be enough for the Bank of Japan as they also intervened that morning. And while prior intervention efforts fell flat as carry traders were there to buy support and push the bullish trend, this time there was the worry that the carry trade was over.

And when you have a crowded trade that’s starting to unwind, the smelling smoke in the crowded movie theater example comes to mind, where you might not want to wait around as the exit door is only so wide.

USD/JPY showed an aggressive sell-off that spanned into August and along the way global equities took a major hit as well, with many fingers being pointed at the Bank of Japan and the unwind of the carry trade as a culprit behind the volatility. But what doesn’t match in that scenario is the fact that the S&P 500 hit a fresh high the week after the CPI print, after USD/JPY had started to reverse. So while the unwind of the carry may have removed some leverage from global equity markets, it’s unlikely that it was the sole culprit of the sell-off.

Now on to the surprise: In the month of September as the Fed was preparing to cut rates, the move in USD/JPY had started to stall. There was one single morning of tests below the 140.00 handle, but like we saw in the US Dollar in Q4, a massive reversal developed; and for USD/JPY, that entailed a 76.4% retracement of the July-September sell-off.

I’m surprised at how aggressively that move priced-in, and the degree to which the sell-off had retraced. I was expecting carry unwind to come back on a re-test of the 150.00 level, or perhaps even the 151.95 price. But that didn’t happen as the post-election run in the Greenback simply drove the USD and related pairings to fresh highs.

But, with that said, this story isn’t over yet, and USD/JPY remains a hot button for 2025 trade, especially if the US Dollar is going to remain within its longer-term mean-reverting backdrop. It was the 140.00 level that stifled sellers in September, leading to the reversal that showed in Q4. And that’s the area that bears will need to take-out if they want to drive a larger reversal in the pair while unwinding the carry trade that built into and around the FOMC’s rate hike campaign of 2022 and 2023.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

--- written by James Stanley, Senior Strategist

For about a month the logical scenario had started to play out. But, along with it came considerable collateral damage and suddenly several major publications were talking about the carry trade; or, more precisely, the unwind of the carry trade that was being accused of a de-leveraging driver across global equity markets.

When the carry trade is in-force it can be one of the most attractive venues in any market, especially for FX traders. The interest rate differential can allow for near-daily rollover payments, so, like a dividend but more frequent. And as others crowd that side of the trade to buy the higher-yielding currency while selling the lower-yielder, a trend can develop in that direction, allowing for principal gains on top of the swap or rollover earned.

In USD/JPY this started back in 2021, well before the Fed started hiking rates. The simple act of US CPI moving higher was enough to drive anticipation of eventual rate hikes from the Fed, which started to push the long side of the pair. When the Fed began to open the door to hikes in Q4 of 2021, USD/JPY got a boost; and another larger boost in March of 2022 as the Fed began to hike rates. This was the initial build of the carry trade and for USD/JPY, it drove the pair from below 105 in early-2021 to 150.00 in Q4 of 2022.

The carry trade was so logical and clear that other problems started to percolate. The Japanese Ministry of Finance worried about the repercussions of unchecked Yen-weakness, so they intervened in Q4 of that year to try to balance the matter. Because the move had become so incredibly one-sided the corresponding pullback was fast and aggressive with USD/JPY shedding more than 2400 pips in just a few short months. This was 50% of the prior bullish trend, and it held support in early 2023 as buyers jumped back on the long side of the pair, in the direction of the carry.

In November of that year, the same prior high was already back in-play at 151.95. And, again, worries began to show around the Japanese Ministry of Finance around the consequences of unchecked Yen-weakness. And much like we saw the year before a sell-off developed with that price holding as the yearly high. But this time the sell-off was less severe as price only retraced 23.6% of the 2021-2022 major move.

USD/JPY Weekly Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

2024

As we came into 2024 it was still unclear as to whether the Fed would be able to cut rates, as this is something that would have a direct impact on the interest rate differential between Japan and the U.S. and in-turn, the carry trade.

We can see USD/JPY price action mirroring rate cut hopes or expectations in the US quite well earlier in the year. As inflation remained high, USD/JPY pushed right back up to the same 151.95 level that had held the highs for the prior two years. In April, just after an above-expected US CPI release, USD/JPY broke out above that price, setting a fresh 33-year high in the process.

It didn’t take long for USD/JPY to ascend to the next major psychological level of 160.00, which was in-play just a few weeks later. But, again, worries from the Japanese Finance Ministry drove an intervention that entailed USD-selling and JPY-buying from the Bank of Japan in effort of producing a reversal in the pair.

That’s when the 151.95 level came in as support. And then bulls did the same thing they had done for much of the prior three years, they priced in the direction of the rate differential. In June USD/JPY was back above the 160.00 level again, and that strength held into July.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Carry Comes Undone

It was the morning of July 11th when matters began to unravel. That was the morning of a US CPI print and this time, the data came in below expectations. This gave hope that the Fed would actually be able to cut rates and along with that would be rate compression between the US and Japan, a factor that would not be positive for carry traders on the long side of the pair.

But that didn’t seem to be enough for the Bank of Japan as they also intervened that morning. And while prior intervention efforts fell flat as carry traders were there to buy support and push the bullish trend, this time there was the worry that the carry trade was over.

And when you have a crowded trade that’s starting to unwind, the smelling smoke in the crowded movie theater example comes to mind, where you might not want to wait around as the exit door is only so wide.

USD/JPY showed an aggressive sell-off that spanned into August and along the way global equities took a major hit as well, with many fingers being pointed at the Bank of Japan and the unwind of the carry trade as a culprit behind the volatility. But what doesn’t match in that scenario is the fact that the S&P 500 hit a fresh high the week after the CPI print, after USD/JPY had started to reverse. So while the unwind of the carry may have removed some leverage from global equity markets, it’s unlikely that it was the sole culprit of the sell-off.

Now on to the surprise: In the month of September as the Fed was preparing to cut rates, the move in USD/JPY had started to stall. There was one single morning of tests below the 140.00 handle, but like we saw in the US Dollar in Q4, a massive reversal developed; and for USD/JPY, that entailed a 76.4% retracement of the July-September sell-off.

I’m surprised at how aggressively that move priced-in, and the degree to which the sell-off had retraced. I was expecting carry unwind to come back on a re-test of the 150.00 level, or perhaps even the 151.95 price. But that didn’t happen as the post-election run in the Greenback simply drove the USD and related pairings to fresh highs.

But, with that said, this story isn’t over yet, and USD/JPY remains a hot button for 2025 trade, especially if the US Dollar is going to remain within its longer-term mean-reverting backdrop. It was the 140.00 level that stifled sellers in September, leading to the reversal that showed in Q4. And that’s the area that bears will need to take-out if they want to drive a larger reversal in the pair while unwinding the carry trade that built into and around the FOMC’s rate hike campaign of 2022 and 2023.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

--- written by James Stanley, Senior Strategist