The Week Head CB Meetings and NFP

Monday 2nd September

- AU manufacturing PMI, company profits, business inventories

- NZ trade balance

- JP business capex, manufacturing PMI

- CN manufacturing PMI

- EZ, FR, DE, UK manufacturing PMI (final reads)

Tuesday 3nd September

- South Korean CPI and GDP

- AU current account, retail sales, RBA cash rate decision

- UK construction PMI

- EZ producer prices

- CA manufacturing PMI

- US ISM Manufacturing

Wednesday 4nd September

- AU services PMI, GDP

- CN Services PMI

- EZ, FR, DE, UK services PMI, EZ retail sales

- CA trade balance, BOC cash rate decision

Thursday 5nd September

- AU trade balance

- DE industrial orders

- US ADP employment/jobless claims, services PMI, ISM non-manufacturing PMI

Friday 6nd September

- AU construction

- JP household spending, leading/coincident indicator

- DE industrial output

- EZ employment (final), GDP (revised)

- US Nonfarm payroll

- CA employment

{kind=link}

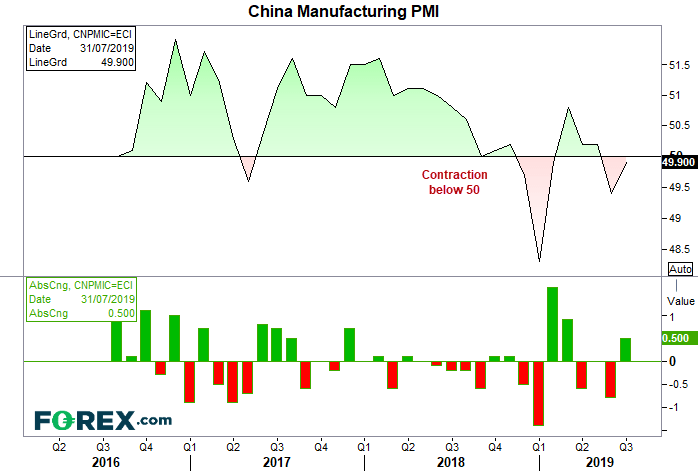

Chinese Manufacturing PMI: USD/CNH, AUD, NZD and JPY pairs, Copper, China A50, Hang Seng

China’s manufacturing sector has contracted two consecutive months, adding to the chorus of calls for a global slowdown. That said, the rate of contraction slowed in July, and if PMI is to climb back above 50, we’d expect a bout of risk-on for the session. AUD pairs are particularly sensitive to the data as they’re key trade partners, but Chinese indices and copper also make decent markets to monitor around the data’s release.

RBA Cash Rate Decision and Q3 GDP: AUD pairs, ASX200

At time of writing, the RBA rate indicator expects just an 11% chance of a 25 cut on Tuesday. This moves to 74% for a cut in October and a 115% cut (ie fully priced in) for November. This is no major surprise, given they cut by 25 bps in June and July and their August minutes provided a ‘steady as she goes’ approach, whilst emphasising external risks such as the trade war. Moreover, GDP data is out on Wednesday and they’d likely want this data on hand before easing further. Yet this still could be a high volatility event if there is a notable shift in tone with their statement.

As for GDP, RBA expect growth to average around 2.5% this year. With Q1 GDP hitting 1.8%, it’s not off to a great start and, with ANZ expecting it to drop to 1.1% in Q2 and the consensus at 1.4%, economists seem doubtful that RBA are on track to achieve their 2019 growth target. Expect AUD to remain under pressure and bring forward easing expectation should it hit 1.3% YoY or less.

{kind=link}

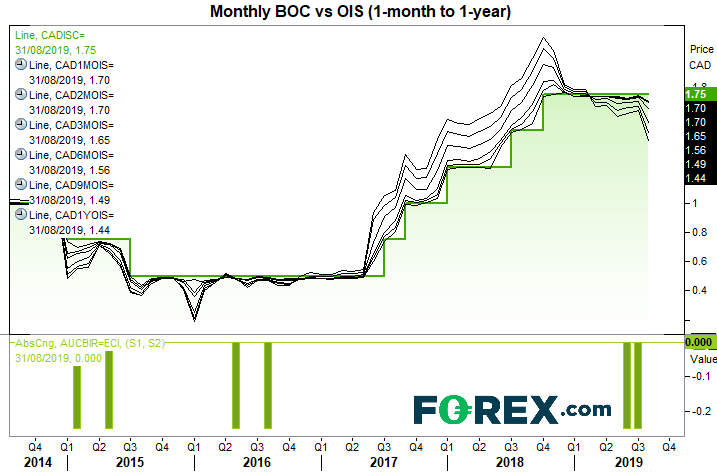

BoC Rate Decision

It’s unlikely BoC will change policy next week, given inflation remains around 2% has not ‘dipped’ as expected. Moreover, the 1-month OIS suggests less than a 20% chance of a cut at their next meeting. Still, markets suspect the next direction will be a cut, with 6-month OIS pricing in around 74% chance and a 25bps cut being bullish priced in by April next year. So we’ll keep a close eye on the statement to see if there is a dovish twist, although chances are it will reiterate their need to monitor the energy sector and the impact of ‘trade conflicts’ whilst remaining optimistic over domestic growth.

{kind=link}

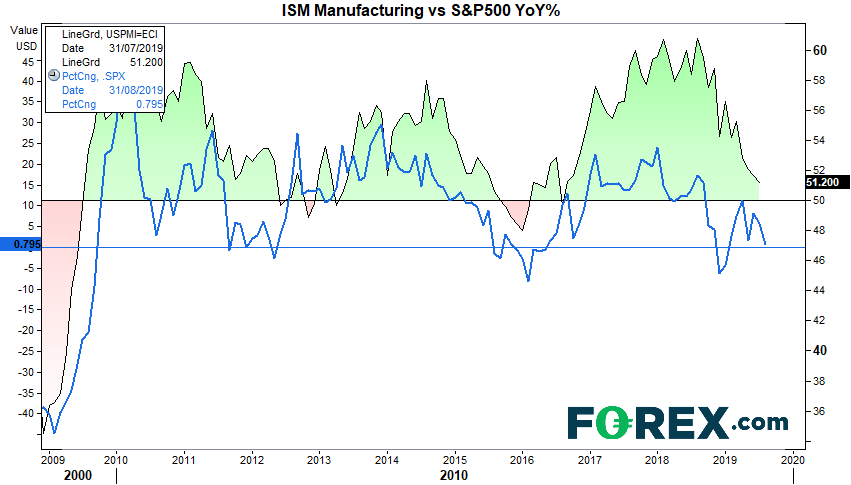

US ISM Manufacturing: USD pairs, US indices, WTI, Gold, Silver

Global PMI remain under pressure and traders are waiting to see if manufacturing PMI dips below the 50% threshold to show the sector contracting. It’s an important gauge for markets as it can lead GDP by 6-9 months, so any weakness here will translate to lower growth expectations, earnings for companies and therefor prices.

US and CA Nonfarm payroll: USD and CAD pairs, US indices, WTI, Gold, Silver

Employment is expected to soften to 155k, well below the 1-month average of 187.16 and unemployment is expected to hold steady at 3.7%. With ADP employment released on Thursday, and a 3-month correlation of 0.81, we could see NFP revised if ADP misses expectations. However, average hourly earnings may be the better read to follow as it has been trending notably higher on an annualised basis, so traders use it as an inflationary gauge (and therefor, a better read of how the Fed are likely to react). That said, as the CME FedWatch tool suggests 95.8% chance for Fed to cut 25bps in September, it’s hard to see any such data will remove this almost given event. For that, we’d need to see a solid breakthrough in trade talks which, at present, appear unlikely to appear on the horizon.

Take note that Canada release employment data alongside NFP, which places USD/CAD in the sights of the volatility crossbow. CAD/CHF and CAD/JPY are also pairs to consider, if you want to focus on the Canadian employment side of things.

The information on this web site is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement. The information and opinions in this report are for general information use only and are not intended as an offer or solicitation with respect to the purchase or sale of any currency or CFD contract. All opinions and information contained in this report are subject to change without notice. This report has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. Any references to historical price movements or levels is informational based on our analysis and we do not represent or warranty that any such movements or levels are likely to reoccur in the future. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness, nor does author assume any liability for any direct, indirect or consequential loss that may result from the reliance by any person upon any such information or opinions.

Futures, Options on Futures, Foreign Exchange and other leveraged products involves significant risk of loss and is not suitable for all investors. Losses can exceed your deposits. Increasing leverage increases risk. Spot Gold and Silver contracts are not subject to regulation under the U.S. Commodity Exchange Act. Contracts for Difference (CFDs) are not available for US residents. Before deciding to trade forex, commodity futures, or digital assets, you should carefully consider your financial objectives, level of experience and risk appetite. Any opinions, news, research, analyses, prices or other information contained herein is intended as general information about the subject matter covered and is provided with the understanding that we do not provide any investment, legal, or tax advice. You should consult with appropriate counsel or other advisors on all investment, legal, or tax matters. References to FOREX.com or GAIN Capital refer to StoneX Group Inc. and its subsidiaries. Please read Characteristics and Risks of Standardized Options.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

The products and services available to you at FOREX.com will depend on your location and on which of its regulated entities holds your account.

FOREX.com is a trading name of GAIN Global Markets Inc. which is authorized and regulated by the Cayman Islands Monetary Authority under the Securities Investment Business Law of the Cayman Islands (as revised) with License number 25033.

FOREX.com may, from time to time, offer payment processing services with respect to card deposits through StoneX Financial Ltd, Moor House First Floor, 120 London Wall, London, EC2Y 5ET.

GAIN Global Markets Inc. has its principal place of business at 30 Independence Blvd, Suite 300 (3rd floor), Warren, NJ 07059, USA., and is a wholly-owned subsidiary of StoneX Group Inc.

© FOREX.COM 2024