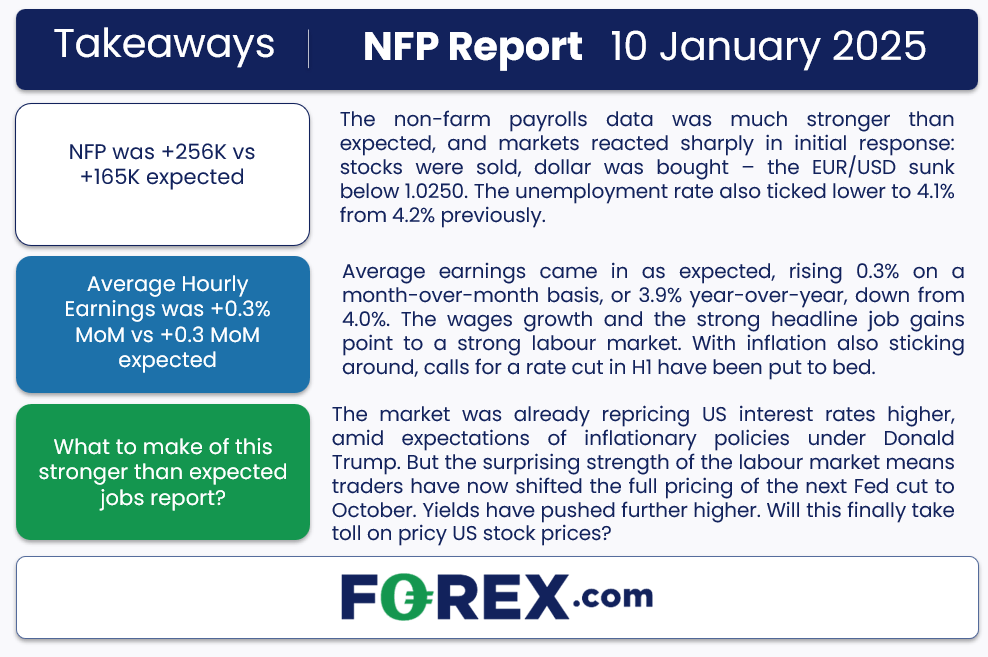

The market was already repricing US interest rates higher in recent days and week, amid expectations of inflationary policies under Donald Trump, when he takes office later this month. But the surprising strength of US labour market means traders have now shifted the full pricing of the next Fed rate cut to October. As a result, yields have pushed further higher, causing the dollar to further extend its advance. It will be interesting to see whether rising yield will finally take toll on pricy US stock markets, especially growth stocks. Our S&P 500 outlook has been quite cautious since the turn of the year amid sky high valuations and the hawkish repricing of US interest rates.

How strong was the jobs growth?

Very strong. Though revisions took away about 8K from the prior two months’ data, the December payrolls report was still much stronger than expected, and markets reacted sharply in initial response: stock index futures were sold, and the dollar was bought – the EUR/USD, for example, sunk below 1.0250.

The unemployment rate also ticked lower to 4.1% from 4.2% previously, further strengthening the case for a lengthy pause.

Meanwhile, average earnings came in as expected, rising 0.3% on a month-over-month basis, or 3.9% year-over-year, down from 4.0%. The wages growth and the strong headline job gains point to a strong labour market. With inflation also sticking around, calls for a rate cut in H1 have been put to bed.

Valuation concerns in focus

Valuation worries have been back in the spotlight this week. According to analysis from Bloomberg a couple of days ago, US stocks were approaching their most overvalued levels in nearly 20 years compared to corporate credit and Treasuries. The earnings yield—a key indicator of profitability relative to stock prices—had slipped to 3.7%, marking its lowest point against Treasuries since 2002. The story isn’t much better when compared to BBB-rated corporate bonds, which were yielding 5.6%. By this measure, stocks were already at their weakest relative position since 2008, according to Bloomberg’s estimates. Historically, when equity yields lag behind bond yields, trouble often looms for the stock market, as seen in the early 2000s. Yet, despite these warning signs, Wall Street had remained surprisingly resilient. The real question is whether the start of 2025 will finally turn the tide. Price action today certainly points that way, even if this ultimately proves to be a short-lived dip.

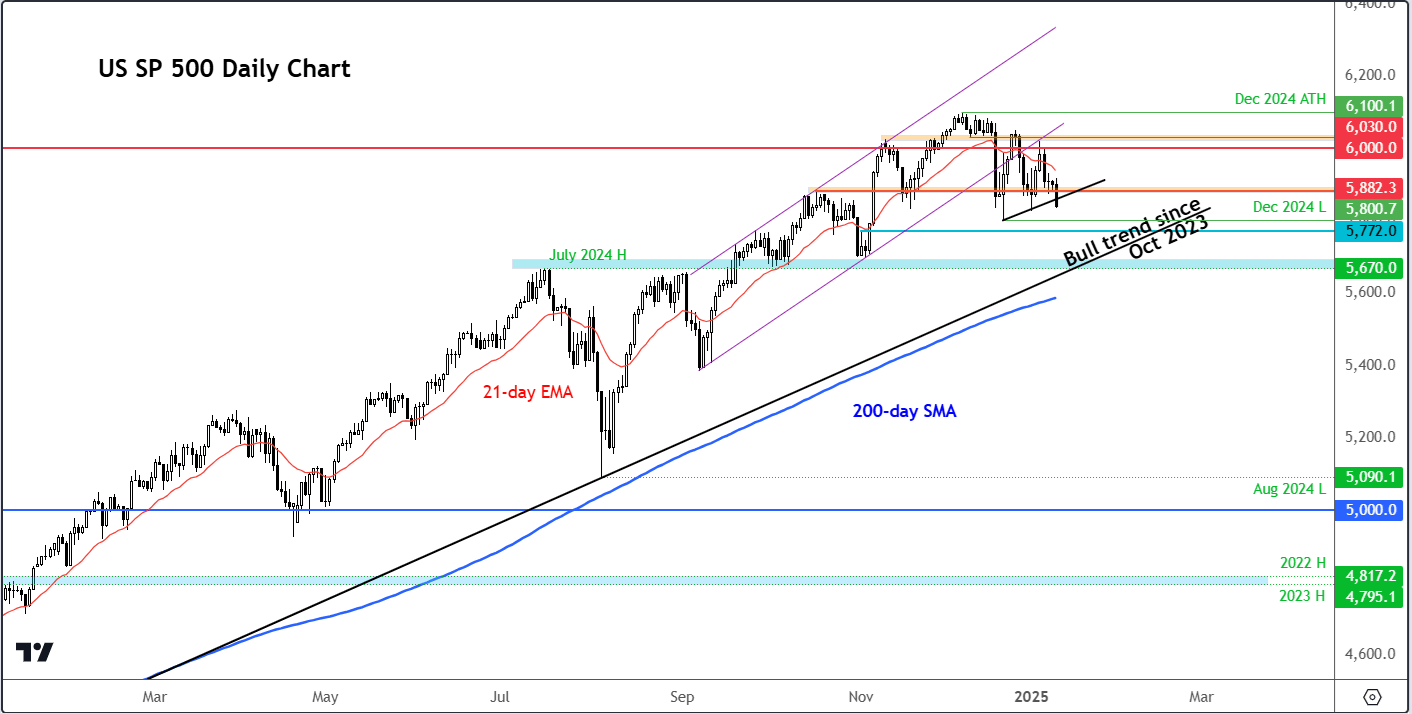

S&P 500 key levels to watch

Source: TradingView.com

Having already broken below its bullish channel in mid-December, the technical S&P 500 outlook has turned a little bearish. Yet downside follow-through has been missing so far. Let’s see if today’s break of support at 5880/82 area will trigger follow-up technical selling in the hours and days ahead now.

The next downside target is liquidity resting below the December low at 5800, followed by support at 5772. But could the selling potentially take us to the long-term trend line, or even the 200-day average? Both of these come in around or slightly below the July high of 5670, making the area around this level, a significant support to watch.

S&P 500 outlook: Looking ahead to next week

Following the very strong US labour market report, attention will shift to inflation data in the week ahead, when we will also have CPI data from the UK as well as key Chinese figures. The S&P 500 outlook is subject to volatility should we see surprising results from the inflation data.

UK CPI

Wednesday, January 15

UK’s headline CPI has been on the rise again since October, printing +2.6% y/y readings in each of the past two months. Services inflation and strong wage growth seem to be sticking around, putting pressure on bond prices. But if CPI cools down more than expected then the pricing of BoE rate cuts should come back forward a little and ease the pressure on UK assets.

US CPI

Wednesday, January 15

Investors have been pushing back their rate cut expectations in recent weeks amid resilience in US data, rising yields and owing to Trump’s expected inflationary policies (tax cuts and tariffs). Therefore, CPI will have to be significantly weaker to cause a major dent in the dollar’s bullish trend.

Chinese GDP

Friday, January 17

As well as GDP, we will get the latest retail sales and industrial production data from the world’s second largest economy on Friday. China’s bleak economic outlook has sparked a surge in demand for Chinese bonds, causing their yields, local stocks and yuan to drop. We need to see stronger data to ease fears of a deflationary spiral in the world’s second-largest economy.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 05:39 PM

Today 04:50 PM

Today 02:44 PM

Today 04:56 AM

Latest articles

Yesterday 04:00 PM

Yesterday 01:00 PM

January 8, 2025 12:31 AM