Traders will keep a close eye on the outcome of the second round of the French elections at the Asian open next week, as it could have a direct impact on European markets. Given that the far right failed to secure a majority government, there are upside risks for the euro if they do not perform as well as currently expected. Jerome Powell will also address the Senate Banking Committee ahead of a key inflation report next week. Both events have the potential to shape policy expectations for 2025. NZ dollar traders should closely monitor the RBNZ meeting to see if they maintain the hawkish stance that surprised markets in their prior meeting.

The week ahead calendar

The week ahead: Key themes and events

- French election (round two)

- Jerome Powell testifies to congress

- US CPI

- RBNZ interest rate decision

French election (round two)

Once again, we begin the trading week with our eyes on the French election, which could create some volatility for European markets. Because the first round failed to deliver an outright majority, the top two candidates will battle it out in the second round. If we consider that euro pairs gapped higher after the first round revealed that the far right failed to secure an outright majority, there’s a risk of another rise for euro pairs should they fail to win this round as well. However, for a real rally in the euro to commence, the left needs to come out victorious and hold on to power in the National Assembly. If this outcome is combined with softer US inflation data and a dovish Fed, the euro could become the strongest major currency of the week.

Trader’s watchlist: EUR/USD, EUR/GBP, EUR/CHF, EUR/JPY, EUR/AUD, AUD/CAD, EUR/NZD, DAX 40, CAC 40, STOXX 50

Jerome Powell testifies to the Senate banking committee

On Tuesday the Fed Chair will speak with the Senate Banking Committee. When Jerome Powell last spoke with them in March he warned that the road back to their inflation target will likely be bumpy, even though it had moderated. I type this ahead of a key nonfarm payroll report, but over the past two weeks Fed doves have been treated to soft PCE inflation, ISM manufacturing and services report. A softer-than-expected NFP report would be the icing on the cake and potentially allow Powell strike a move dovish tone for rates in 2025. Particularly if unemployment rises to 4.1% or higher given his recent comment that unemployment still remains “very low” 4%.

Trader’s watchlist: EURUSD, USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones, VIX, bonds

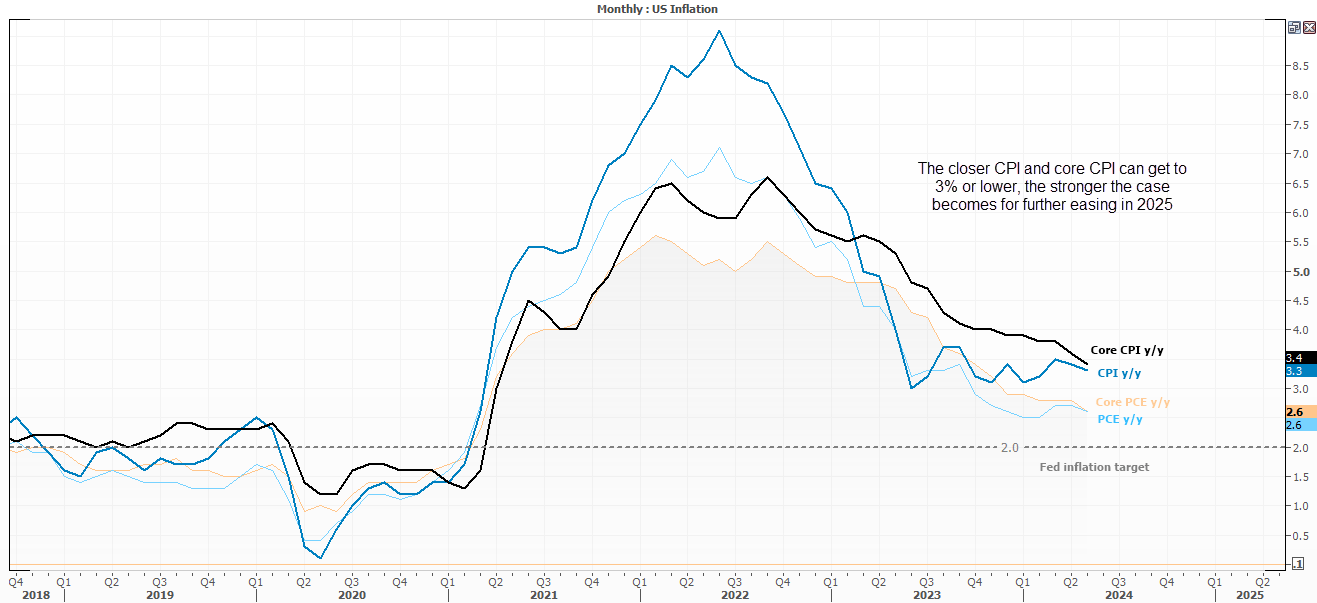

US consumer price index (CPI)

Last week’s soft core PCE inflation report generated some excitement that price pressures were falling faster than the Fed anticipated. Not only did core PCE come in much softer than expected, but so did the Fed’s so-called ‘super core PCE’, with both rising just 0.1% month-on-month.

Earlier this week, Jerome Powell acknowledged that disinflation was on the right path, even if he deems the 4% unemployment rate as “very low”. Translated, it suggests the Fed is in no rush to cut rates unless unemployment rises notably from here. But if Fed doves are treated to a rising unemployment rate of 4.1% or higher (released later today), then it sets the stage nicely for hopes of a soft CPI report next week.

And if that materializes, it could prompt Powell to revisit his outlook that inflation could reach the ‘mid to lower 2s’ by the end of 2025. Currently, CPI sits at 3.3% and core CPI at 3.4%. The closer they can get to 3% next week, the stronger the case for Fed cuts next year becomes, and a more bearish reaction could be expected for the US dollar, to the delight of risk appetite.

Trader’s watchlist: EURUSD, USD/JPY, WTI Crude Oil, Gold, S&P 500, Nasdaq 100, Dow Jones, VIX, bonds

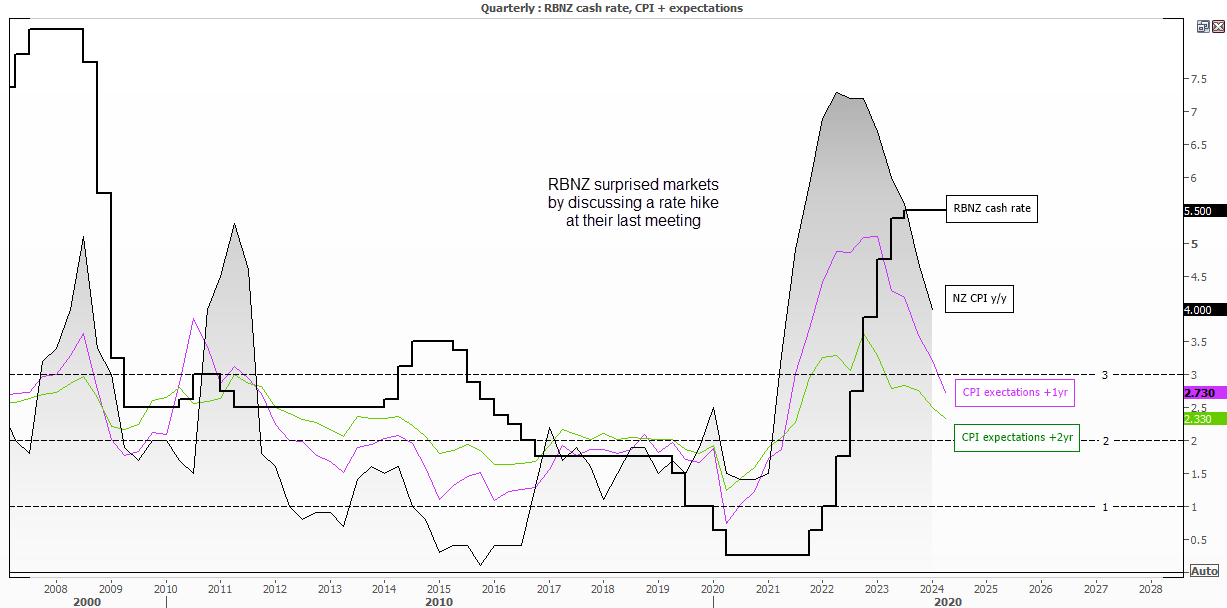

RBNZ interest rate decision

Whilst it remains highly unlikely the RBNZ will signal a change of policy next week, I’m intrigued to see if they walk back their hawkish twist from their last meeting. Markets were positioned for the central bank to switch from a neutral to slightly dovish stance, not deliver the talk of a hike that they went on to divulge.

Since the last meeting, retail sales, manufacturing and business PSIs and food prices came in below expectations and contracted. Knowing the RBNA this won’t be enough for then to scale back their threat of a hike, even if it remains an outside chance that one will materialise. Still, if they do revert to a neutral tone it could weigh on the NZ dollar and support AUD/NZD.

Trader’s watchlist: NZD/USD, NZD/JPY, AUD/NZD

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

Latest market news

Today 07:15 PM

Today 04:10 PM

Latest articles

December 15, 2024 01:00 PM

December 8, 2024 11:51 PM

December 1, 2024 01:00 PM

November 24, 2024 01:00 PM