EUR/USD Talking Points:

- Since the Euro came into inception in 1999 there’s been just one instance of EUR/USD trading below the parity level of 1.0000.

- That instance was relatively brief as there were just two monthly closes below that price, and both the FOMC and ECB responded with the former getting less-hawkish and the latter going less dovish. Soon the ECB was hiking in 75 bp increments and a strong reversal developed in the pair.

- After that reversal from the parity test, EUR/USD was range-bound for almost two full years – until the Q4 breakdown last year. The big question now is whether the trend can continue to push to allow for another parity test in 2025 trade.

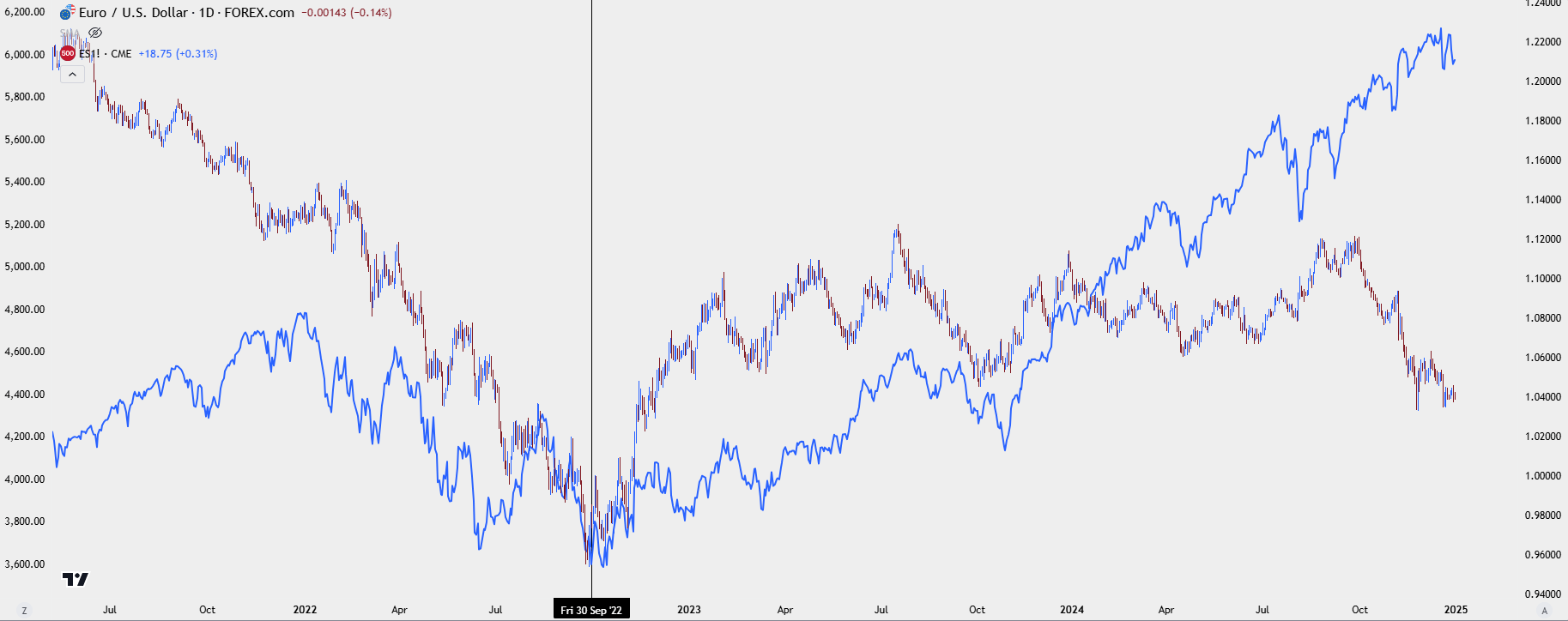

EUR/USD is nearing completion of its most bearish quarter since Q3 of 2022, which was when the current all-time-low was set for the pair. With the Euro representing 57.6% of the DXY quote, such imbalance can bring vulnerability and risk to both European and U.S. economies. In the 2022 episode, as USD strength was taking over global equity markets were in a dire state, and it was as the U.S. Dollar sold off and the Euro snapped back that global stocks set lows and embarked on a massive rally that largely ran through the end of this year.

This isn’t to imply a directly perfect relationship between EUR/USD and equity markets, however, as the EUR/USD pair has spent the better part of the past two years in a range-bound mode as US stocks have been flying higher. But – the extremes of US Dollar strength can bring strain to American corporates, making it more difficult to sell products outside of the United States given that additional US Dollar strength while also making imports in the US more competitive from a price perspective. A stronger currency is, in essence, attempting to whittle down inflation which can also bring hindrance to economic growth.

And because this is currencies that we’re talking about, where currencies are the base of the financial system – there’s no way to value a currency than with other currencies. So if we have a strong U.S. Dollar that means we probably have a weak Euro or Japanese Yen and/or British Pound, which would have ramification, as well.

EUR/USD and S&P 500 Futures from the Q4, 2022 Low

Chart prepared by James Stanley, EUR/USD on Tradingview

Chart prepared by James Stanley, EUR/USD on Tradingview

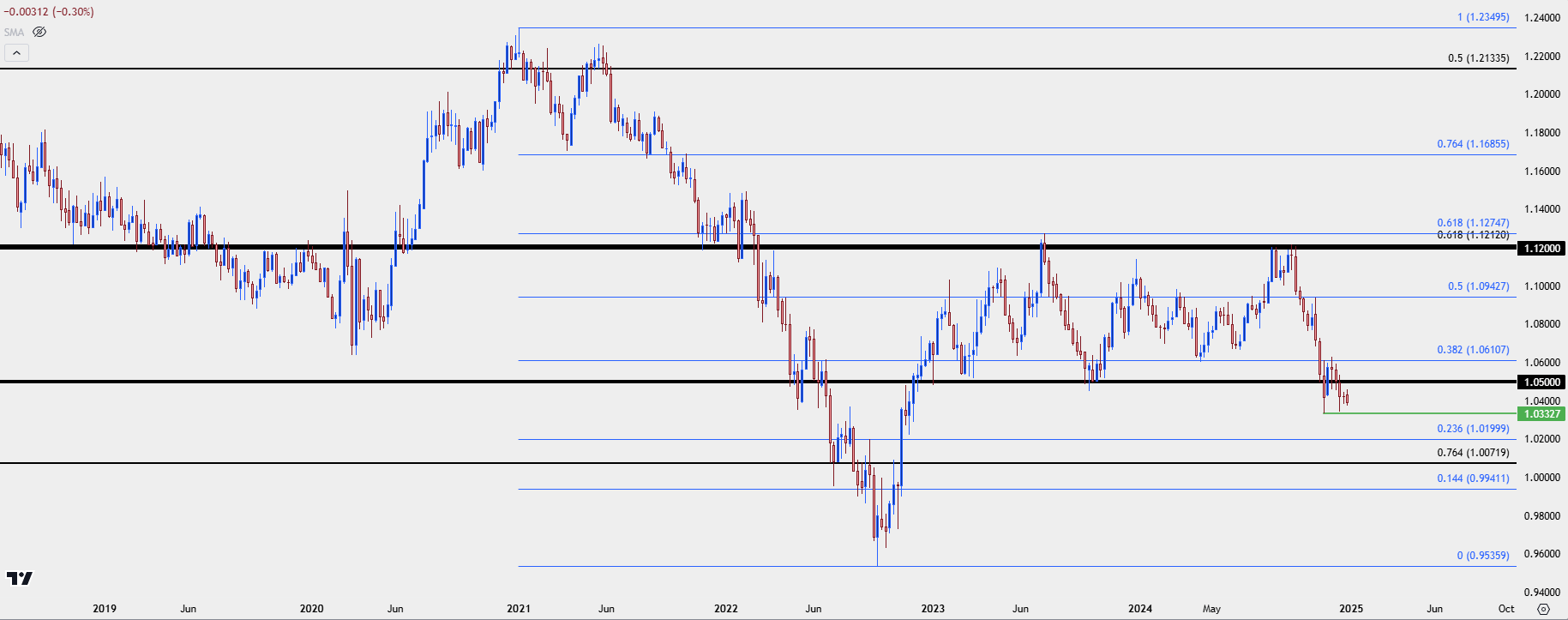

EUR/USD in Q4

For much of Q3 the US Dollar was very weak. Even with US inflation holding above the Fed’s target of 2%, the bank continued to talk up the prospect of rate cuts which eventually landed with a couple weeks left to go in the third quarter.

The Fed even biased towards the more-dovish option of cutting rates by 50 bps but interestingly, this did little for US Dollar price action and, in-turn, EUR/USD prices. The pair merely pushed back up to resistance that had set in August and then stalled. On the weekly chart, EUR/USD built an evening star pattern into the end of Q3 and the open of Q4 as sellers showed up at the open of the fourth quarter. That then led into a brutal move that saw bears break through the support side of the range at the 1.0500 handle.

But – much as we saw in Q3, where the bulk of the pair’s progress was built in the first two months of the quarter followed by stalling in the final month, the same happened on the other side for EUR/USD in Q4, where the low that was set in November held through December trade.

EUR/USD Weekly Chart

Chart prepared by James Stanley, EUR/USD on Tradingview

Chart prepared by James Stanley, EUR/USD on Tradingview

EUR/USD: Is Parity Possible?

First off it must be acknowledged that parity is a possibility, particularly after the EUR/USD pair put in a trend as strong as what we saw last quarter. But – it also must be noted that this would likely come with consequence, as a weakening Euro and a stronger U.S. Dollar would make economic growth and, in-turn, equity gains in the United States a more challenging prospect. When we saw the blistering run of US Dollar strength in 2022, global equities showed poor performance and that’s not in the best interest of any major central bank.

Ideally with currencies a degree of stability will take-over, allowing corporates to focus on their mission objectives rather than trying to constantly balance a shifting game of volatile currency prices. And with globalization as deeply intertwined into the American economy as it is, it would seem near impossible for both equities and the US Dollar to gain throughout 2025 trade.

The November rally in both markets showed on the back of the U.S. Presidential election of Donald Trump and there was a similar inter-play at his first election in 2016. In the aftermath of both, the US Dollar, and US equities ripped-higher. But in the prior instance, that USD strength did not last for long in 2017, and even as the Fed hiked rates three times for 25 bps each in that year, the US Dollar continued to sell-off through the 2018 open. Along the way, stock prices ripped-higher even as the Fed was tightening policy.

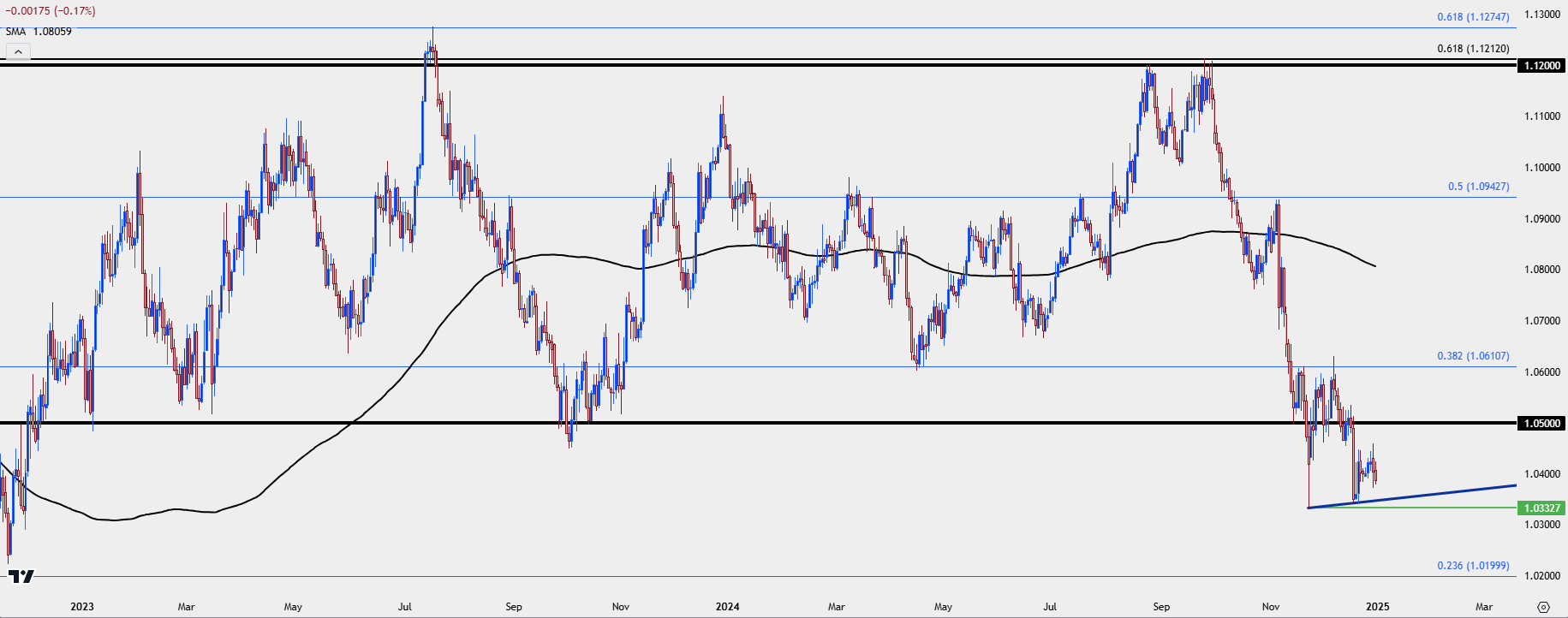

So, while trend continuation must be acknowledged as a possibility, I think the more desirable outcome for most parties involved would be EUR/USD mean reversion. And speaking to that case, December has produced a higher-low as sellers were unable to get down to the same 1.0333 level that held support in November.

On that theme, the 1.0500 level will be key as this prior range support would need to be re-claimed by bulls, after which the 1.0611 Fibonacci level comes into play which helped to hold the highs for the second-half of Q4.

EUR/USD Daily Price Chart

Chart prepared by James Stanley, EUR/USD on Tradingview

Chart prepared by James Stanley, EUR/USD on Tradingview

--- written by James Stanley, Senior Strategist

Latest market news

Yesterday 08:49 PM

Yesterday 08:32 PM

Yesterday 06:30 PM

Latest articles

Yesterday 04:02 PM

December 20, 2024 04:14 PM

December 12, 2024 08:54 PM

December 9, 2024 08:30 PM