In the wake of the Great Financial Crisis, Federal Reserve Chairman Ben Bernanke introduced a number of unconventional policies, including Quantitative Easing, one of the most controversial programs in the history of central banking…but the more lasting and undeniably effective policy has been ushering in the era of “communication-as-a-policy-tool.”

Over the past decade, there have been 83 FOMC meetings, with the interest rate decisions and market-implied pricing playing out in the following way:

- In 72 meetings, the market was anticipating no interest rate change, and the Fed left rates unchanged.

- In 9 meetings, the market was expecting a 25bps hike and the Fed delivered a 25bps hike.

- In 2 meetings (July and September), the market was expecting a 25bps cut and the Fed delivered a 25bps cut.

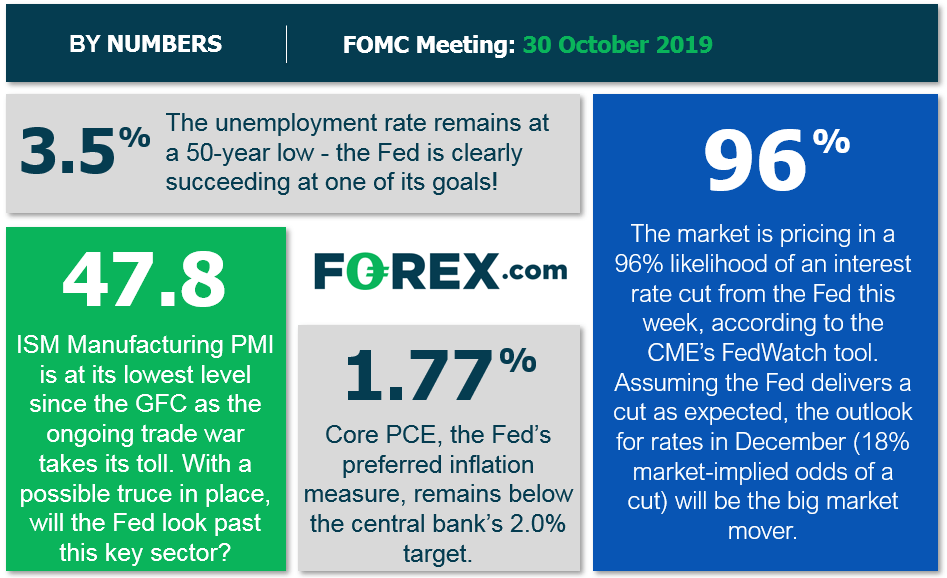

In other words, the Fed hasn’t gone against the market’s pre-meeting “conventional wisdom” even once in the past decade. With traders pricing in a 96% chance of a 25bps rate cut tomorrow according to the CME’s FedWatch tool, the FOMC will almost certainly cut interest rates 25bps and run the streak to 84 consecutive meetings.

Source: FOREX.com

Even though the immediate interest rate decision is “known” in advance, changes to the central bank’s statement and the tone of Chairman Powell’s press conference could still lead to a volatile market reaction based on how they impact the implied odds of a rate cut in December. As of writing, the CME’s FedWatch tool is showing about 15% odds of another interest rate reduction in six weeks’ time.

In terms of specifics, traders will key in on the committee’s characterization of international trade in the wake of progress between the US and China on trade, as well as any comments about the recently-slowing growth in job creation. In addition, the central bank’s decision last month featured three dissents (Bullard in favor of a 50bps cut, and George/Rosengren in favor of leaving rates steady); any further “dissension in the ranks” would introduce an element of uncertainty to the future outlook for policy.

In Powell’s testimony, the key topic to watch will be the Fed’s recent (re)introduction of asset purchases (which the central bank has definitively characterized as “NOT Quantitative Easing”). After the recent turmoil in the short-term funding market, traders will be keen for an update on the stability of this critical function of the financial system. If Powell indicates the program could expand from here or expresses pessimism about any other aspect of the economy, the US dollar could retrace last week’s gains and stock indices could surge further into record territory on the potential for further monetary support into the end of the year.

While its unlikely to be the most market-moving central bank meeting in recent memory, traders will still have plenty to digest tomorrow afternoon!

Related Analysis:

DXY and EUR/USD Retreat From Key Levels Ahead Of Fed

Latest market news

Today 04:00 PM

Yesterday 08:00 PM

Yesterday 02:00 PM

Yesterday 07:00 AM

Yesterday 02:00 AM

December 24, 2024 08:00 PM

Latest articles

December 23, 2024 11:30 PM

December 17, 2024 04:12 PM

December 17, 2024 06:28 AM

December 13, 2024 10:13 AM