November 1, 2023 12:29 PM

- Dollar analysis: All eyes on FOMC

- ISM manufacturing PMI bucks trend of hotter US data

- Focus will turn to NFP and ISM services PMI

The resilience of US data we have seen over the past couple of weeks hasn’t led to any further appreciation in interest rate expectations, keeping the dollar in an overall holding pattern with a slight bullish tilt, especially against the weaker currencies like the JPY and EUR. But the likes of the AUD and previously CHF have shown some resilience, perhaps suggesting that most of the positivity may be priced in for the greenback. Therefore, for the dollar to accelerate again from here, it may take a lot more effort than was the case previously. By the same token, it will take less effort to knock it down. This is exactly what happened earlier today when the US manufacturing PMI came out much weaker than expected, which caused a sharp, albeit short-lived, intraday sell-off in the dollar. However, it is the trend of the data that is more important in the eyes of the Fed, and so far, the trend has remained overall positive as we have found out in recent weeks. But if we now start to see a few cracks starting to show in US economy then we could see an accelerated move lower in the dollar. The ever-important nonfarm payrolls report and the ISM services PMI will be released on Friday. But now it is all about the Fed…

Dollar analysis: All eyes on FOMC

In a couple of hours’ time, the Fed will decide on interest rates. No one is expecting a rate hike at this meeting, so the rate decision itself should not move the markets, but the Fed’s language regarding the future meetings will be scrutinized. Following the release of some more forecast-beating data earlier this week, the probability of a final hike in the next meeting in December increased to around 26% from around 20% last week, before dropping back to the same level on the back of that manufacturing PMI data and a soft ADP payrolls report. The Fed will likely keep the door to one more rate hike open, given the resilience of the US economy and the potential for inflation to remain high for longer. But any dovish tilt could see the dollar take a sharp plunge.

ISM manufacturing PMI bucks trend of hotter US data

The run of forecasting-beating US data continued earlier this week, but today we had some mixed-bag data. The surprisingly soft manufacturing PMI data overshadowed a stronger JOLTS report, and several other hotter-than-expected data released earlier this week and through much of October.

Yesterday, the Conference Board’s consumer confidence index, two measures of house prices and employment cost Index all came in ahead of expectations. Last week saw the UoM’s consumer sentiment, pending and new home sales, GDP and both manufacturing and services PMIs all top expectations. The week before it was retail sales, industrial production and jobless claims data that had beaten expectations. So, the US economy is showing continued resilience in the face of high interest rates, putting the Fed in a slightly difficult position as to whether it should tighten its belt even further, or just keep rates at these current levels for a longer-than-expected period of time. A growing number of analysts and economists seem to agree with the latter approach. Let’s see if this is something that the Fed alludes to at this meeting, and how this will impact the dollar. One reason why the Fed is unlikely to raise rates again is the recent rise in long-term bond yields, which effectively is equivalent to a couple of additional rate hikes.

As mentioned, the manufacturing PMI came in very soft today. It printed 46.7 vs. 49.0 expected and last. This slowdown is in line with the global manufacturing activity. But there were some eye-catching details in the report, and not for good reasons. The employment index, for example, fell to 46.8 versus 50.3 expected and down from 51.2 in previous month. This bodes ill for the official nonfarm payrolls report on Friday. What’s more, new orders printed 45.5, falling sharply from 49.2 prior. It looks like the strength of the US dollar is starting to hurt the economy. This was emphasised in the S&P Global manufacturing PMI report (which was left unrevised at 50.0), highlighting that “new international sales fell further and at a slightly sharper pace than in September."

The softer manufacturing data has raised some doubts over the “higher for longer” narrative. Things can unravel very quickly given how weak the global economy outside of the US has been of late. This narrative will be put to the test again later in the week with Friday’s release of the October US jobs report and the ISM services PMI data that would be released later in the day. And with the Fed decision taking place later on today, the US dollar should be in for a roller-coaster ride as we enter the business-end of the week.

So, if upcoming US data were to start disappointing more, the US dollar’s downside reaction may well be more pronounced than its upside would in reaction to positive data.

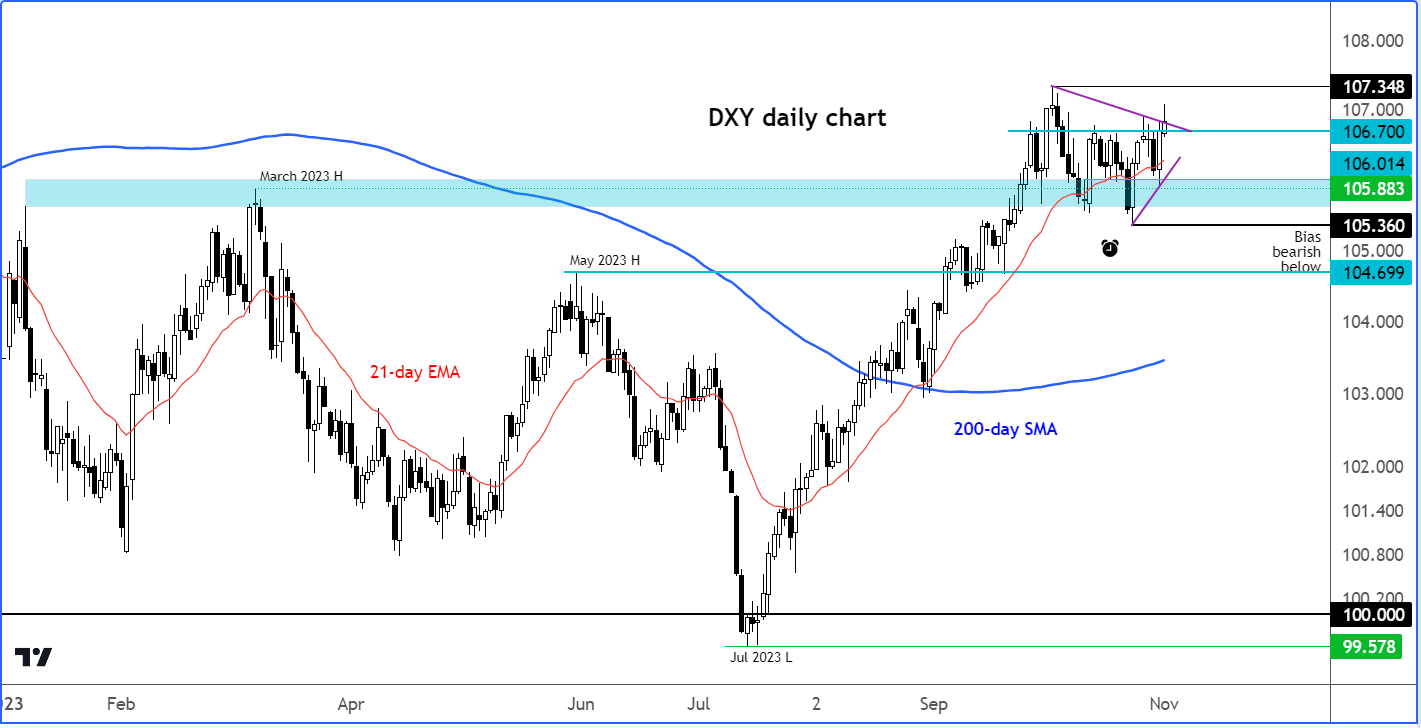

Dollar Index technical analysis

Source: TradingView.com

Ahead of the big macro events, the US dollar index was above short-term resistance at 106.70, testing the resistance trend of the triangle continuation pattern. A potential failed breakout scenario would be very interesting, and one that the dollar bears will be hoping to see today, or later in the week. The bulls, who still remain in control of overall price action, will be eyeing a daily close above 106.70. If seen, this could pave the way for the DXY to run towards a fresh high on the year above 107.35, keeping the bullish trend alive for yet another day.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 07:15 PM

Today 04:10 PM

Today 12:30 PM

Latest articles

Yesterday 04:20 PM

Yesterday 02:00 PM