Oil prices have been falling sharply for the past five weeks or so and the poor run of form has continued for another day today. The last time I looked at crude oil was on October 12 in an aptly-titled article: Crude sell-off pauses but outlook is bleak. As I noted then, we were quite bearish on oil prices because of the recent fundamental developments being far from positive for crude, with reputable oil forecasters such as the International Energy Agency (IEA), for example, lowering their demand growth forecasts owing in part to the recent emerging market currency crisis, reducing their buying power. At the same time, both OPEC and non-OPEC supply of oil has been on the rise. The cartel has been pumping extra oil in order to help offset the potential shortages arising from Iran, in preparation to the US re-instating tough economic sanctions on Tehran – which came into force this week. However, the US intends to allow several large oil consumer nations to continue importing crude from Iran for another 180 days. These countries include South Korea, Japan, India, China, Turkey, Taiwan, Italy and Greece. In other words, Iranian oil exports will continue to remain around their current levels for a good few months still. Added to this, crude oil production in Russia climbed to a record high level and in the US, too, supply has been on the increase in recent months.

Downward pressure could ease

However, with prices falling, you’d expect the supply excess to start dwindling again. After all, it is becoming cheaper for consumer nations to ramp up their crude purchases, pushing up demand, while it becomes increasingly costly for inefficient producers to maintain output at current levels, thereby reducing supply. But while we continue to remain bearish on oil prices long-term, it is important to note that prices have now fallen close to levels where we had anticipated. As such, we expect the selling pressure to potentially ease in the coming weeks.

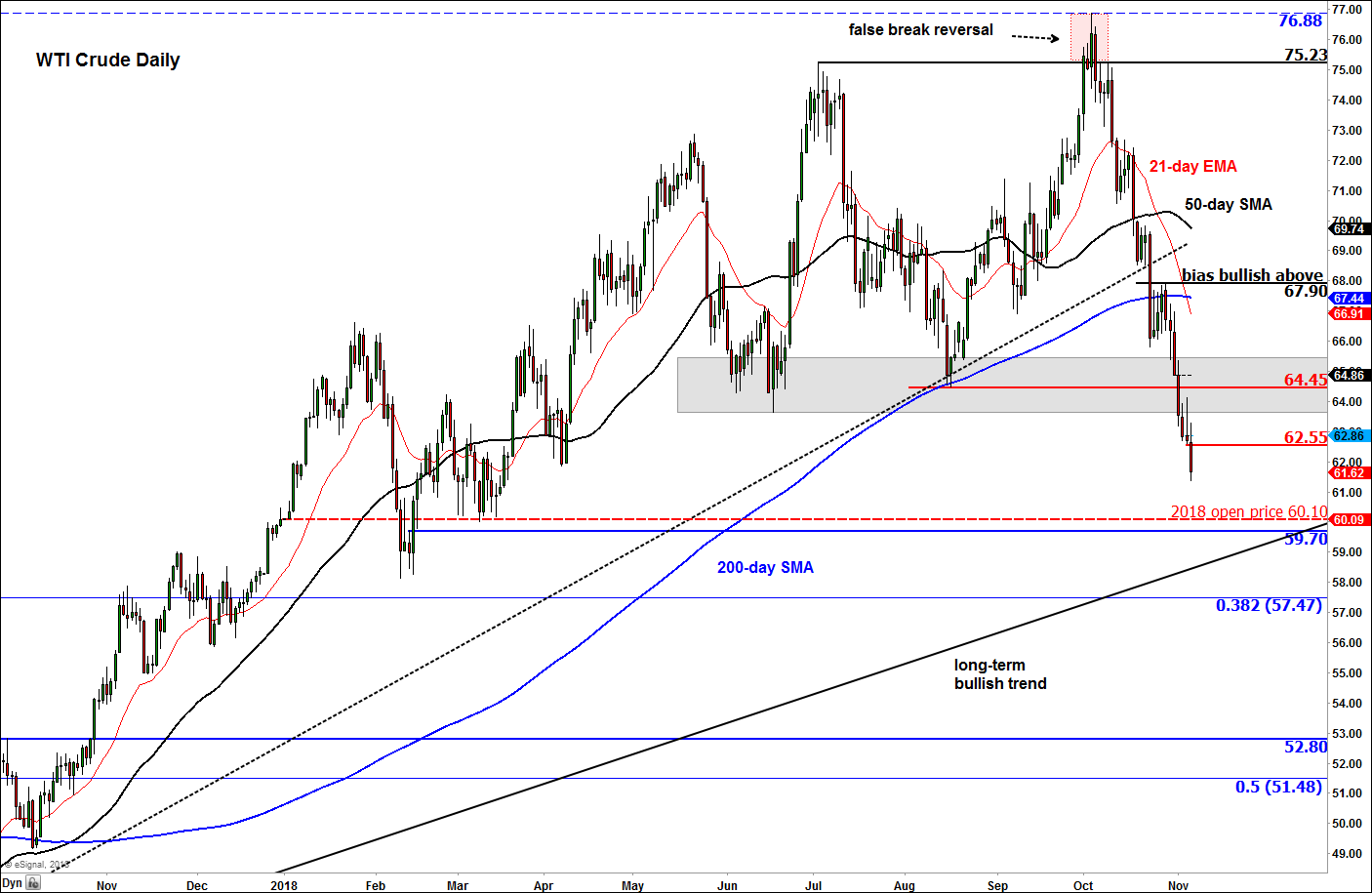

WTI approaching key technical support levels

But for the time being, the downward pressure remains intact and the path of least resistance is still to the downside. WTI’s key short-term resistance level to watch is around $62.55, a level which marks the low of the inverted hammer daily candle from yesterday. Additional resistance comes in around the shaded region on the chart, with $64.45 within this zone being a particularly interesting level as it was the most recent swing low (which could turn into resistance on future re-tests). In terms of potential support, the area around $60 is very important to watch. Not only is this a psychologically-important level, but we have this year’s opening price level of $60.10 converging there, while an old untested resistance level at $59.70 comes in close proximity to that $60 handle. Below this $60 area, we have the long-term bullish trend line to watch as the next major support. Depending on if and when price gets there, the trend line comes in around $58.50-$59.00.

Source: eSignal and FOREX.com. Please note, this product is not available to US clients

Latest market news

Today 04:07 PM

Latest articles

January 12, 2025 01:00 PM

January 10, 2025 05:39 PM

January 8, 2025 04:30 PM

January 7, 2025 09:34 AM