- Investor risk appetite is strengthening with the soft landing narrative remaining in place, helping to boost cyclical asset classes

- The ASX 200 and AUD/JPY are two markets that have benefitted from the favourable environment

- Outside geopolitical risks, the macro calendar isn’t laden with events that could upend the prevailing narrative, although the Bank of Japan (BOJ) rate decision is one risk event to watch

With risk appetite back in full swing and market indicators on US recession risk providing a green light for the soft landing narrative, cyclicals such as Australia’s ASX 200 and AUD/JPY recovered last week, returning to the uptrend they’ve been in since the risk rival revival took hold in late October.

And with no Federal Reserve speakers due to the pre-meeting media blackout, and with advanced release of Q4 US GDP and December PCE deflator highly likely to bolster the case for soft landing narrative, there’s every likelihood the prevailing trends will continue this week in the absence of an unexpected market shock, be it known such as the BOJ, Bank of Canada or ECB meetings or otherwise.

Investor sentiment boosting cyclicals

Be it US stocks surging to fresh highs, US consumer sentiment lifting by the most since 2005 as inflation expectations continued to moderate, or the US 2s-10s curve bear steepening, an outcome that usually signals strengthening economic activity, there is plenty of evidence to suggest the soft landing narrative remains entrenched in investor psyche. And while the US is not representative of everything happening in the global economy, as long as its growth prospects remain solid, concerns about the outlook for activity in other major economies, such as China and the eurozone, are unlikely to derail the bullish backdrop.

For cyclical assets like the AUD or ASX 200, this is the kind of environment in which they would usually benefit.

Events calendar not laden with major risk events

Looking at the near-term outlook, the question becomes what could potentially change the environment for the worse? Looking at the known risk event calendar, nothing stands out as likely to cause serious damage to risk-positive environment this week.

Markets will receive the latest batch of flash PMI report cards from around the world, but it’s unlikely they’ll deliver any insights we don’t already know: Europe is struggling as are most parts of Asia with the US slowing down.

Elsewhere, with the Atlanta Fed GDPNow forecast model pointing to above-trend US GDP growth in Q4, and the relatively reliable Cleveland Fed Inflation Nowcast suggesting core PCE inflation rose by 0.25% in December, unless there’s a big deviation from those expectations, the soft landing narrative will likely remain intact.

With the ECB and Bank of Canada comfortably on hold with rates, the only obvious sticking point that could upset things is further disruptions to shipping activity in the Middle East, carrying the potential to break or buckle supply chains which may increase inflation and slow economic growth.

BOJ could surprise with favourable backdrop, but probably won’t

The Bank of Japan’s (BOJ) monetary policy meeting and New Zealand Q4 consumer price inflation report are other events that are of relevance to the ASX 200 and AUD/JPY in the coming days. While both carry the potential to deliver surprises, they would have to be significant to generate a meaningful market reaction.

Regarding the BOJ, with recent inflation and wages data continuing to weaken, policymakers have yet to receive the kind of evidence that Japan is now experiencing a virtuous cycle between wage pressures and higher inflation, making it risky to begin lifting rates preemptively. But with policymakers elsewhere pushing back hard against large and rapid rate cut expectations while market risk appetite remains buoyant, the macro environment is kinder for the BOJ to consider lifting rates than only a month ago. Given the BOJ will release updated economic forecasts including for inflation, there is scope for the bank to deliver a hawkish surprise. However, while the BOJ has done so previously, it comes across as unlikely given the downside risks involved this time.

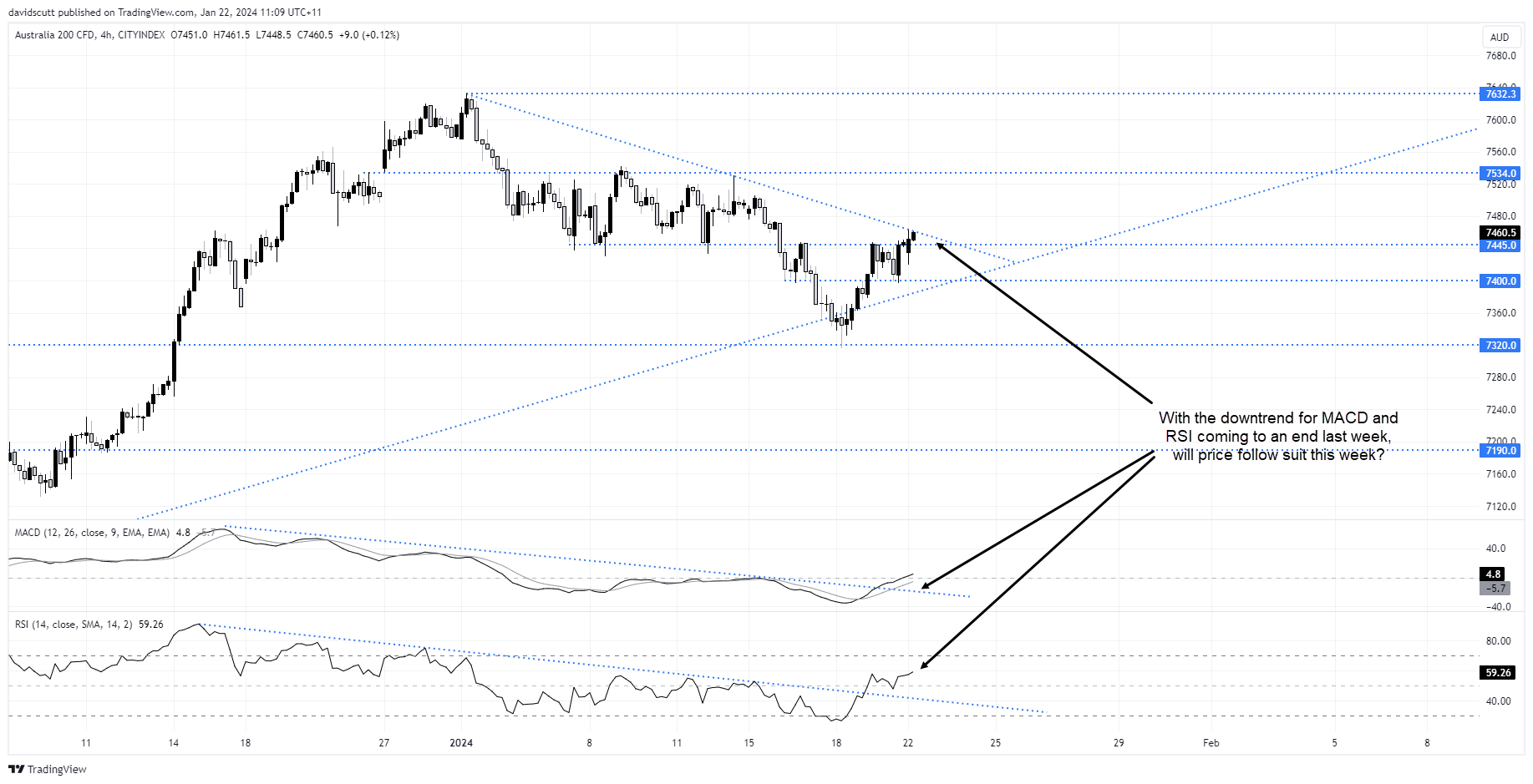

ASX 200 fights back into uptrend

With the downtrend in RSI and MACD having come to an end last week, the question for the ASX 200 is will price follow suit? Traders may get an answer to that question momentarily with the index now testing downtrend resistance dating back to the highs struck late last year. Having broken horizontal support located around 7445, a break of the downtrend may open the door for a push back towards 7534, a level it was unable to overcome earlier this year. If a topside break eventuates, a stop-loss order either below it or horizontal support at 7445 will offer protection.

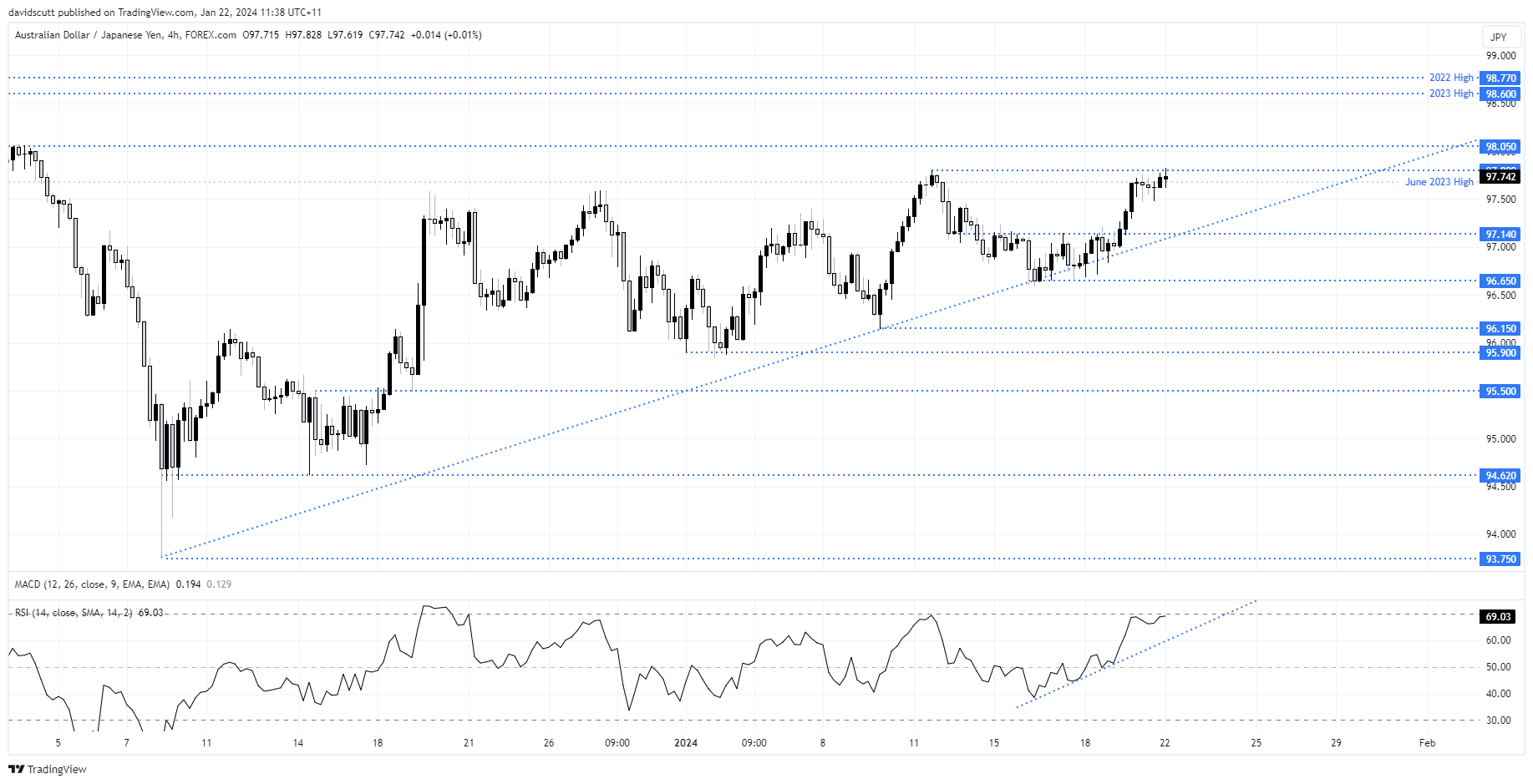

AUD/JPY eyeing off prior highs

The technical picture for AUD/JPY is not too dissimilar to the ASX 200, testing uptrend support last week before spring loading back higher. The price is battling horizontal resistance at 97.80 having attracted bids on several occasions late last week ahead of 97.50. This is another trade where you can let the price action tell you what to do with topside break of 97.80 opening the door to a retest of 98.05 and even the highs of 2023 and 2022 set above 98.60. Personally, I’d like to see a bust of 98.05 before initiating longs to allow for a stop to be placed below, improving the risk-reward of the trade.

On the downside, a failure at 98.05, bids ahead of 97.50 would likely be tested again before a potential larger pullback towards 97.14 and 96.65.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Latest articles

December 23, 2024 11:30 PM

December 12, 2024 09:30 PM

November 21, 2024 04:47 PM

November 18, 2024 03:56 PM