Second inflation wave

The US could experience a second wave of inflation, perhaps starting as soon as the next Consumer Price Index (CPI) data to be reported, according to StoneX market strategist Vincent Deluard. Inflation could pick up to a 3.5% annual rate in July due to base effects and a rally in the oil price, now over $80 per barrel from under $70 earlier this year. Such a second wave would echo history. Moreover, identifiable economic shocks could take inflation higher.

Traders expecting the Fed not to raise rates this year, and to enact progressive interest cuts next year, could well be disappointed in inflation rises. The Fed has made it clear that rate increases or cuts will be driven by inflation outcomes. To the extent that the rally in equity markets – with new peaks in the Dow, S&P500 and Nasdaq – have been driven by the expectation of rate cuts, this analysis highlights potential risks.

Deluard argues history supports this view: inflation has seldom gently fallen back to the Fed’s 2% target, following spikes above 7% such as that seen recently. The last few points of inflation reduction are hard to achieve. A black swan event could mar this gradual decline in inflation, such as a higher oil price or soft commodity prices, or an escalation or conflicts in progress or simmering around the globe.

Deluard believes that inflation could eventually stabilize at a long-term plateau of 4%, corresponding to the growth in blue-collar wages. Would this be the worst outcome? Structural inflation of 4% would help finance deficits, reduce wealth inequalities, and boost growth. Unfortunately, the US Federal Reserve is on record targeting 2% inflation.

Criticism of Deluard’s “inflationary waves” scenario, if focused on the 1970s – when US inflation formed three ascending peaks of 6.2% in 1969, 12.3% in 1974, and 14.8% in 1980 – are that maybe this is too short a time period. To counter this criticism, he analyses much longer time periods and identifies persuasive evidence of inflation waves.

UK inflation

Bank of England data shows repeated inflation spikes, with multiple “echo peaks” following the first spike of inflation above 7%.

Historical UK inflation

Source: The Bank of England, A Millennium of Macroeconomic Data. StoneX analysis.

- Inflation rose to a first peak of 10.5% in 1694 after the Bank of England was nationalized to help fund the government’s colonial expenses

- The start of the war of Spanish succession led to a re-acceleration of inflation in the early 1700s, which culminated at 13.5% with the extension of the Poor Law, a very primitive and crude attempt at social welfare

- Inflation rebounded to 16.3% during the Great Frost of 1709 (known as Le Grand Hiver in France), which caused widespread famine

- The fortunes made and destroyed by the South Sea Bubble caused three smaller echo waves of inflation in the late 1710s and early 1720s

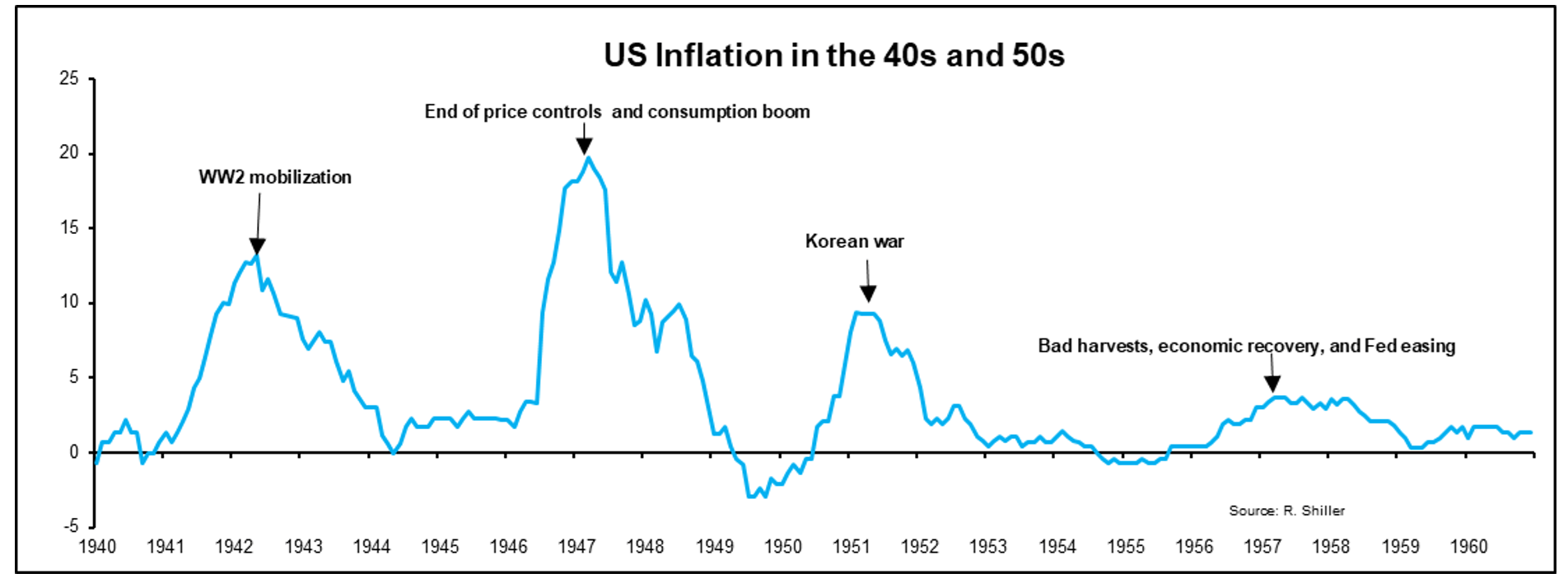

US inflation

Robert Shiller’s reconstruction of US CPI inflation also shows “echo peaks” following the first spike of inflation above 7%.

Historical US inflation

Source: Robert Shiller, Yale University. StoneX analysis.

- Inflation peaked at 13% in 1942 as the US economy mobilized for the war effort

- The end of price controls, global commodity shortages, and the return of victorious soldiers led to a second peak of almost 20% in 1947

- Inflation accelerated to 9.4% during the Korean War

- Inflation rebounded to a plateau of 3-4% in 1957-1958 due to bad harvests and Fed easing

What could cause this second wave of inflation?

Deluard is a disinflation sceptic. He believes that underlying inflation, driven by wages growth, will plateau of 4-6%, and he argues that base effects, recent dollar weakness, and a commodity rally, will see higher inflation.

Additional risk factors include:

- A spike of oil prices above $100 a barrel as the Chinese recovery gains momentum, US growth remains robust, and strategic inventories have been depleted. (Oil is now over $80 per barrel)

- An escalation of the Russia/Ukraine war leading to a nuclear disaster, and more stringent sanctions on Russian production. (With Russian bogged down in trench warfare, the outcome is highly uncertain)

- A second surge in the US money supply to offset the impact of soaring deficits on global liquidity. (We would note that broad US money supply recently turned negative for the first time since the 1960s)

- Bad harvests caused by extreme weather events, and shortages of Russian and Ukrainian fertilizers (Russia is blockading Ukrainian exports)

- The surge of a populist candidate in the 2024 US presidential election as an alternative to two extremely unpopular politicians. (S/he might dangle tax cuts to win power)

- Civil unrest and generalized strikes in Europe and China. (China’s poor growth and high youth unemployment could spark unrest)

Global inflation

Finally, Deluard presents compelling international evidence. World Bank data shows that inflation begets higher inflation. A gentle return to the 2% target without any further spikes, as forecasted in the bank’s Summary of Economic Projection, happened with a probability of one in seventy, after inflation spiked above 7%. In other words, it hardly ever happens in any major developed economy.

Bottom-line: inflation above rates targeted by central banks could be here to stay for some time. That, in turn, could mean higher interest rates for longer. Equity markets, priced off long term discount rates, might not be pricing in this risk.

Analysis by: Vincent Deluard, CFA: [email protected]

Report edited by Paul Walton, Financial Writer: [email protected]

Latest market news

December 20, 2024 04:14 PM

December 20, 2024 02:45 PM

December 19, 2024 10:26 PM

December 19, 2024 05:22 PM

December 19, 2024 02:23 PM

December 19, 2024 01:56 PM

Latest articles

October 3, 2024 04:38 PM

October 2, 2024 04:15 PM

January 5, 2024 03:09 PM

January 4, 2024 06:55 PM