- USD/JPY traders should expect a volatile week

- US rates outlook remains primary driver of USD/JPY movements

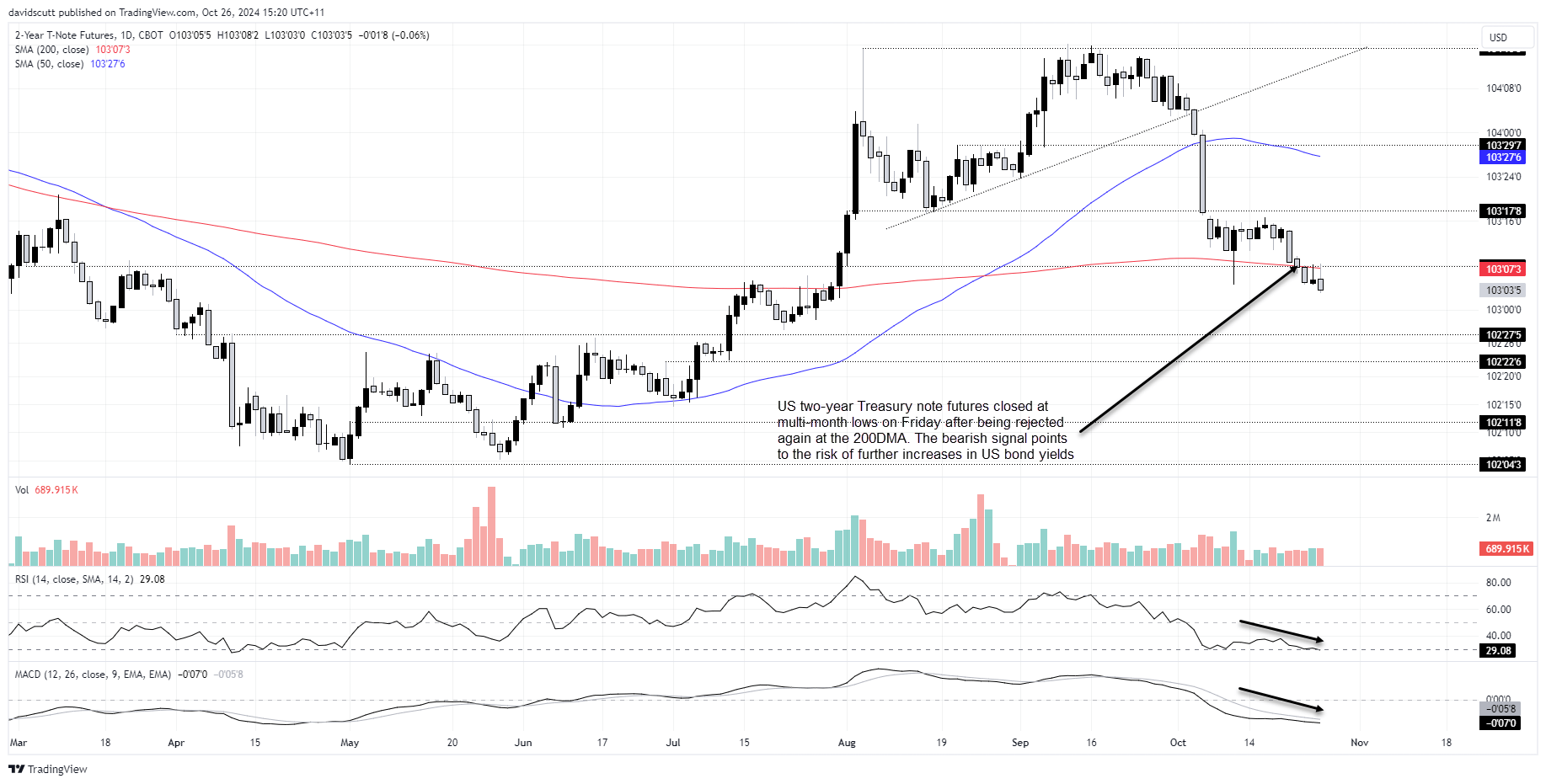

- US rates futures close at multi-month lows, pointing to upside risks for US bond yields and USD/JPY

Overview

Significant political, economic and corporate earnings uncertainly collide this week, creating a tricky environment for USD/JPY traders to navigate. The key message remains that US interest rate fluctuations continue to dictate direction, putting the spotlight on polls, profitability and payrolls over the coming days.

US rates remain key USD/JPY driver

To recap what’s been influencing USD/JPY moves recently, the chart below looks at the rolling 20-day correlation with numerous financial market variables. What stands out immediately is just how strong the relationship remains with movements in interest rate differentials between the United States and Japan, especially between five to 30-year bonds.

While there is no evidence of crude or LNG prices influencing USD/JPY moves despite Japan’s standing as a major energy importer, there has been a modestly positive relationship with US stock index futures over the past month. While it’s no longer a pure risk proxy, there’s still some influence from risker asset classes.

Source: TradingView

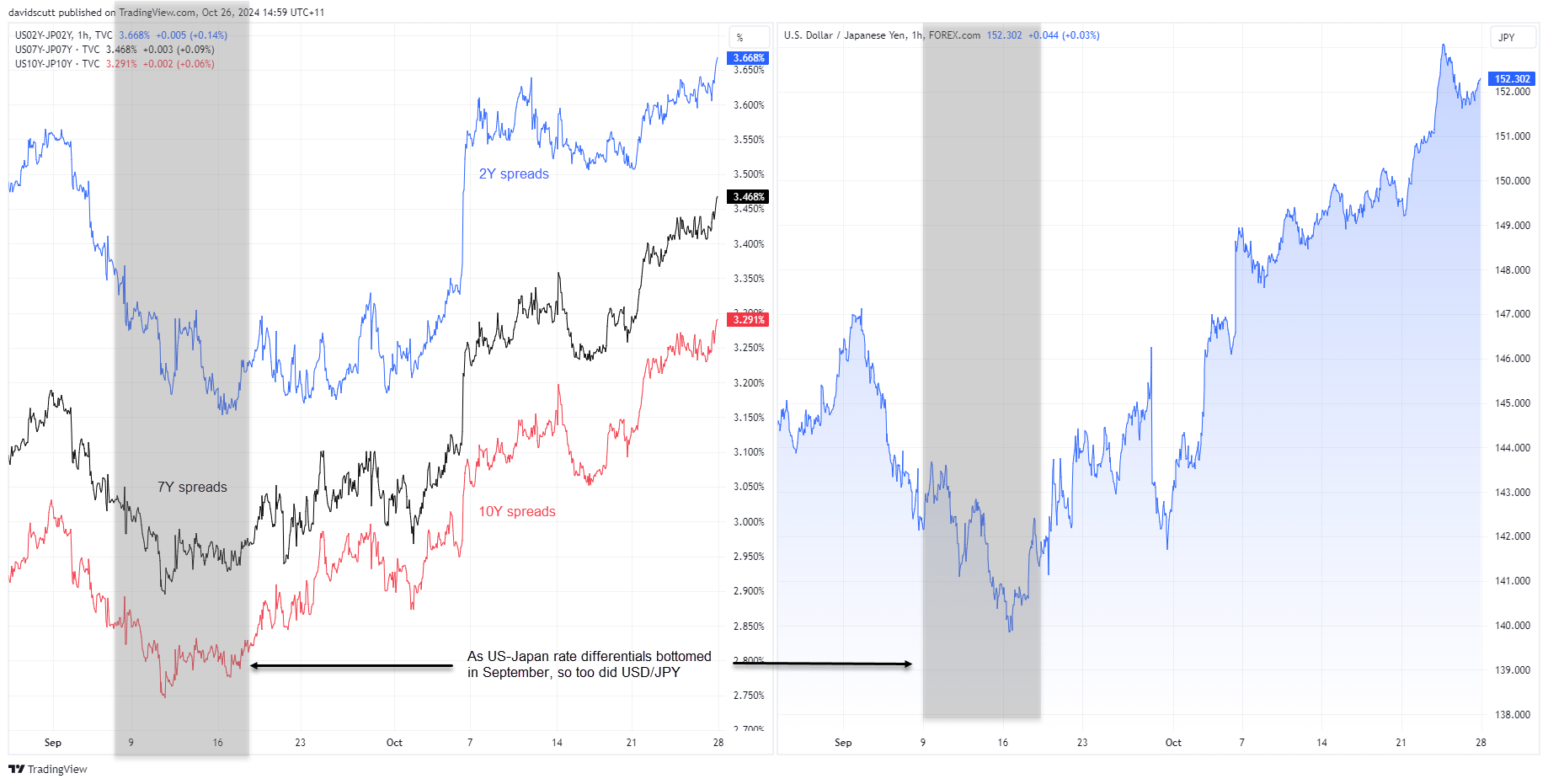

To underline the influence rate differentials are having on USD/JPY, the next chart looks at yield spreads over two, seven and 10-year terms in the left-hand pane with movements in the FX cross. When spreads bottomed in mid-September, it coincided with the bounce in USD/JPY from below 140.

Source: TradingView

Data impact must be assessed through election filter

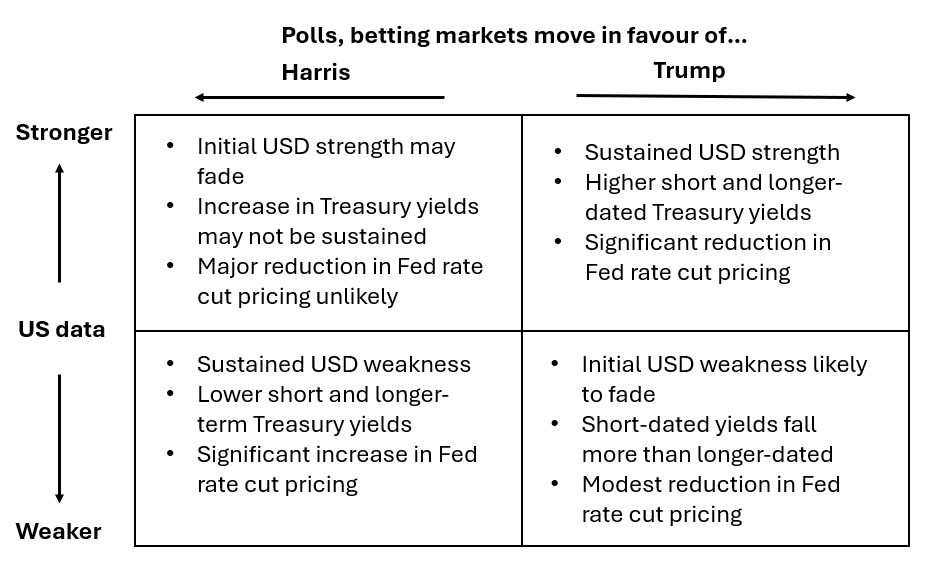

Before we look at the events calendar, it’s important to view upcoming data through the lens of US election uncertainty to gauge the likely market impact. The matrix below is a rough guide on what to anticipate depending on how the polls, betting markets and data prints relative to expectations.

Source: David Scutt

For USD/JPY, the most ponent combination for upside would be Trump to poll strongly with persistent US data strength. For downside, it would be the polls to swing towards Harris and persistent data weakness. Other combinations point to the likelihood of initial market moves being faded as the fiscal outlook overrides near-term considerations for the Federal Reserve.

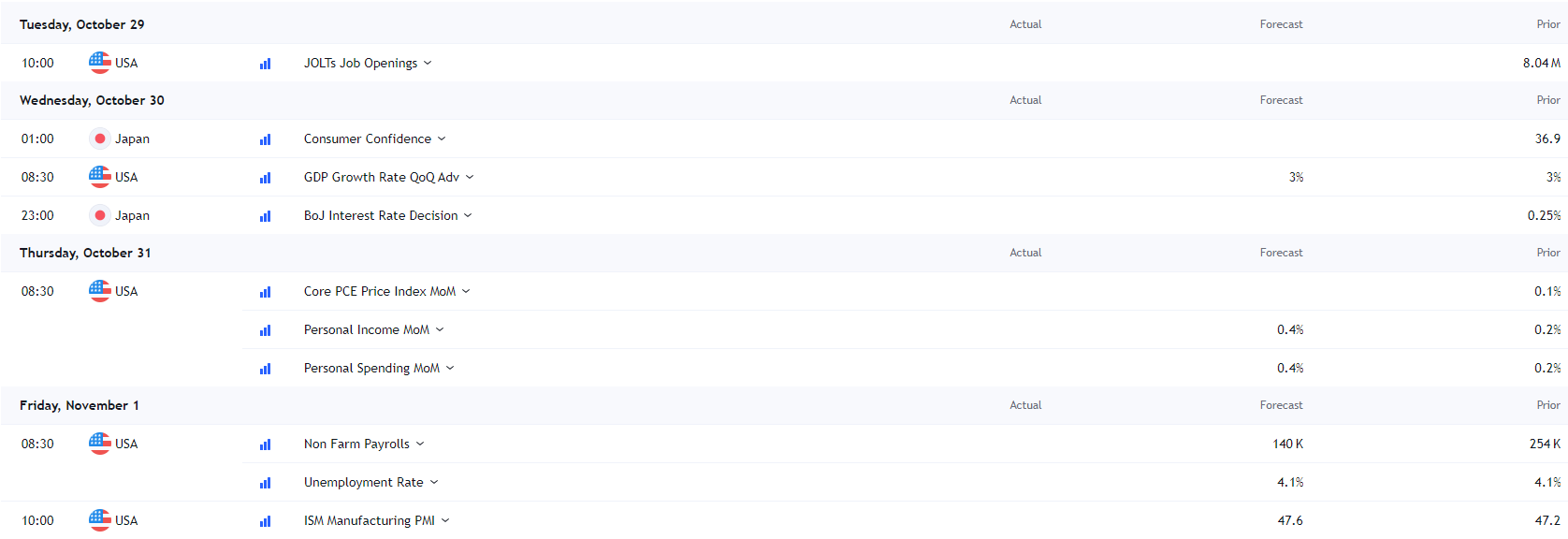

Payrolls headline major risk events

Source: TradingView (Times US ET)

Labour market reports will take precedence over other events, including Thursday’s core PCE deflator. Even though the latter is the Fed’s preferred underlying inflation measure, it rarely delivers market surprises given how well forecasters have been able map trends from US CPI and PPI reports released earlier in the month.

Friday’s non-farm payrolls report is the biggest risk event for the week. While the initial reaction is likely to be driven by the payrolls beat or miss relative to forecasts, the unemployment rate is ultimately the number the Federal Reserve cares most about. If we were to receive another blowout report like September’s where payrolls, hourly earnings and unemployment all beat expectations, it would likely spark another violent unwind in Fed rate cut pricing.

Other events that carry the potential to create volatility include the Conference Board’s consumer confidence report on Tuesday, ADP National Employment report on Wednesday, along with the Employee Cost Index (ECI) which is a closely watched measure of wage pressures.

QRA, auctions may exacerbate rates volatility

It’s not shown on the calendar, but another important event is the US Treasury’s Quarterly Refunding Announcement (QRA). It’s a closely watched event as it outlines government borrowing plans and impacts interest rates and liquidity.

The QRA financing estimates are released on Monday with the official policy statement following on Wednesday. These releases are key for understanding US debt supply and could drive market moves, especially in bonds and the dollar.

Alongside the QRA, the US Treasury will also auction two and five-year notes on Monday and seven-year notes on Tuesday. While these events usually come and go with little market impact, at a time of elevated fiscal and economic uncertainty, any shifts in demand carry the potential to generate volatility in Treasury yields, hence USD/JPY.

Tech earnings create gap risk

Adding a further layer of event risk, the US earnings calendar reaches its crescendo with Alphabet and AMD out Tuesday, Microsoft and Meta on Wednesday, with Apple and Amazon on Thursday. As shown in the correlation analysis earlier, USD/JPY has been moderately correlated with S&P 500 futures over the past month, suggesting we may see some volatility just after market close on Wall Street.

Source: TradingView

BOJ, Japan election headline Japan calendar

As for Japanese event risk, the Bank of Japan (BOJ) monetary policy decision on Thursday is one that traders need to keep an eye on. Markets don’t expect any policy changes even with release of updated economic forecasts, suggesting that if there is to be any volatility, it may come from Governor Ueda’s press conference following the meeting.

As a reminder, there is no set release time for the decision. The press conference is scheduled to start at 3.30pm in Tokyo.

The other major risk event is Japan’s election held on Sunday with the ruling LDP and Komeito coalition no certainty to secure a majority, according to latest polls.

A fragmented outcome where more partners are required to form government may complicate the Bank of Japan’s plans to tighten monetary policy further, adding to uncertainty in the political and economic landscape.

US Rates futures pointing to higher yields

Before looking at the technical picture for USD/JPY, it’s noteworthy US two-year Treasury note futures closed at the lowest level since late July on Friday after being rejected at the 200-day moving average for a second consecutive session. While oversold on RSI (14), the path of least resistance for this key short-dated futures contract appears lower, implying higher yields.

Given the message from the correlation analysis earlier, that points to upside risks for USD/JPY.

Source: TradingView

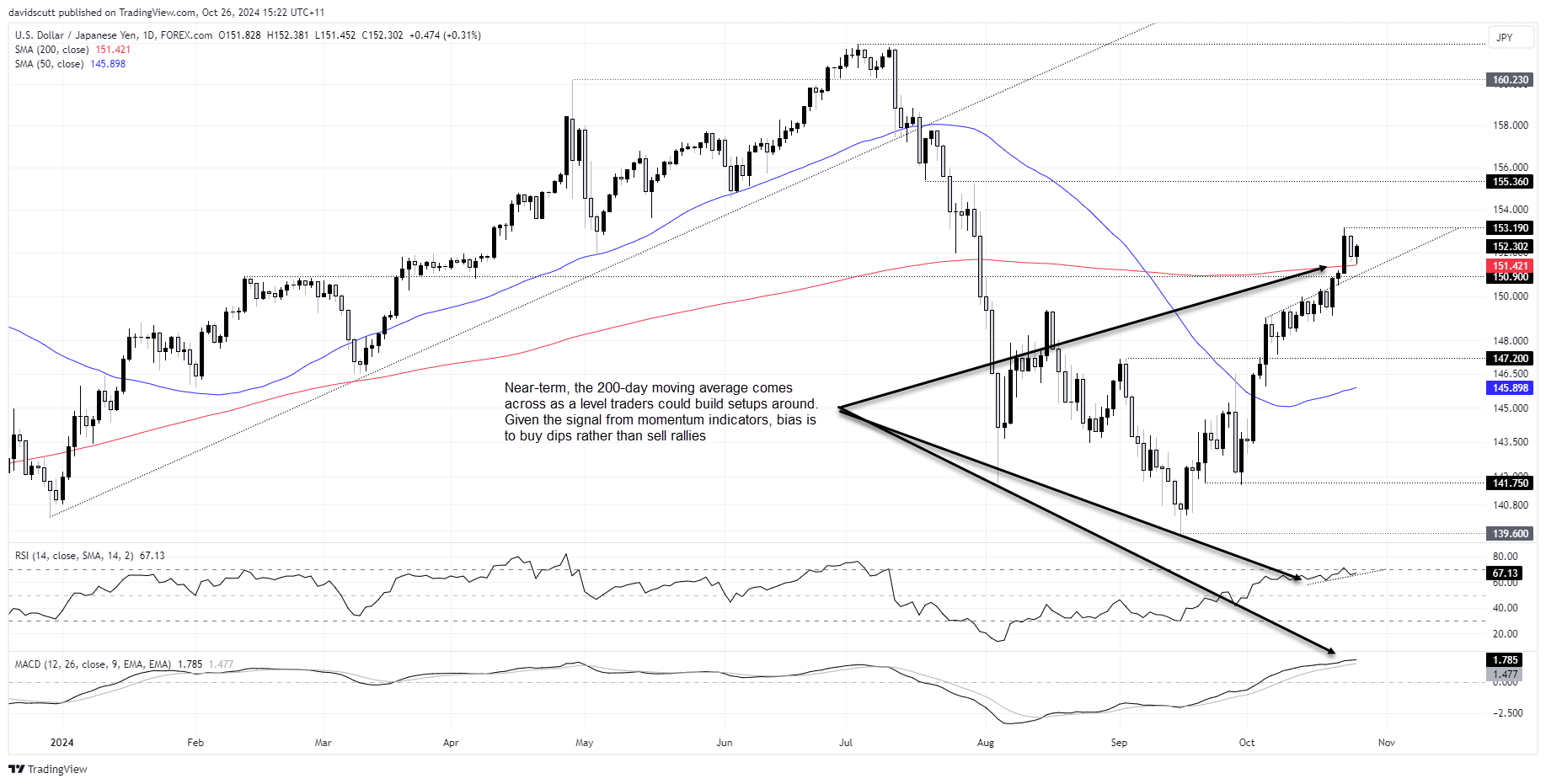

USD/JPY decimates resistance zone

Almost out of nowhere, the sharp increase in US Treasury yields early last week sent USD/JPY careening through multiple resistance levels, eventually seeing it top out at 153.19. That’s the first topside level for traders to note. Beyond, 155.36 and double-top of 157.75 set in July should be on the radar.

On the downside, the price tested and bounced from the 200-day moving average on Friday, suggesting it may offer support. Beneath, the uptrend dating back to October 4 located just above 151.00 and 150.90 are other levels to watch. If the price were to break those levels, dips below 149.50 were bought regularly earlier this month.

The signal from momentum indicators remains bullish, making the near-term inclination to buy dips over selling rallies.

Source: TradingView

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Latest APAC session articles

Today 12:31 AM

Yesterday 10:31 PM

January 2, 2025 06:30 PM