S&P 500, Treasuries Talking Points:

- The past two weeks have been busy on the economic calendar and we’ve seen some fast changes in price action over that period.

- The large move from last week showed after the FOMC rate decision, with Treasury Yields falling fast as Equities put in a major jump. This begs the question as to whether the FOMC is done with rate hikes for this cycle. I explore further below.

- I’ll be discussing these themes in-depth in the weekly webinar on Tuesday at 1PM ET. It’s free for all to register: Click here to register.

Last week saw a major reversal develop in equities and price caught a strong push after the FOMC meeting on Wednesday. This happened alongside a rally in bonds which has led to the scenario of equities rallying as yields have fallen, leading many to claim that the Fed is finished with rate hikes.

This may be the case: But there also may be something else going on here as each of those markets were pretty stretched around last week’s open. Equities were looking very bearish, to the degree that some were calling for a ‘black Monday’ like opening over the past couple of weeks. US Treasuries had just hit 15-year highs for 2-, 10- and 30-year yields. So, collectively it looked like a ‘higher rates driving stocks down’ type of theme.

Of note, the net of last week’s Treasury activity was a deepening of yield curve inversion. The curve had been moving towards flattening since June and this coincided with the bearish run in equities. As I’ve shared before, yield curve normalization can be a challenge for equities because that’s usually coming alongside strength in long-term bonds, which also spells lower yields.

On the below chart, I’m looking at the 10-2 spread, which is simply the 10 year treasury yield subtracting the two year treasury yield. The zero-line indicates equality, with both the two and 10 year treasury yielding the same. Of note is how this began to normalize this summer, around the same time that stocks had topped. I’ve added a red box for last week to indicate the deeper inversion that showed after last week’s moves in Treasuries.

US Treasuries, 10-2 Yield Spread, Monthly Chart (indicative only)

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

Curve Inversion

Spanning back to the year 2000 there’ve been a few different episodes of 10-2 curve inversion, when two-year treasuries carried stronger yields than ten-year issues.

The curve inversion itself didn’t seem to be an overwhelming bearish factor: But normalization of the curve has seemed to coincide with bearish backdrops in equities. And if we think about what’s happening to the Treasury market during those periods it can make sense.

For the curve to normalize we need to see short-term yields going down and long-term yields going up. This is the type of activity that can often come along with a rise in fear in markets, as investors duck for safer harbors in short-dated Treasuries.

On the below chart, I’m highlighting ‘peak inversion’ for two of the prior cycles that aligned with broader bearish backdrops in the equity space. I’ve added ‘SPY’ to this chart, which is an Exchange Traded Fund for the S&P 500 index.

US Treasuries, 10-2 Yield Spread with SPY, Monthly Chart (indicative only)

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

Treasury Yields and Has the Fed Finished?

If we take a step back we have to consider the context, where the FOMC is essentially debating the efficacy of one more hike. This can change, of course, but from the Fed’s own projections it seems that the bank is comfortable with the fact that we’re nearing the end of this hiking cycle.

That can certainly motivate behavior into the long side of bonds: As I’ve written before, when the Fed does signal that they’re done this could create a swell of demand into Treasuries. Because not only can investors lock in a higher yield before rate cuts come into play, they can also see principal appreciate in a falling rate environment. That can actually be the more attractive part of the trade and one item that denotes that from the past week was performance in TLT, which is an ETF that covers Treasuries with 20 years or more to maturity.

Last week saw a strong bounce from a big level of longer-term support. But, the monthly chart below helps to put that move into scope. This may be the start of something more but it’s still very early for that theme.

TLT – Treasuries 20+ Years to Maturity, Monthly Chart (indicative only)

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

Have Yields Topped?

This seems to be a more contentious question at the moment.

It’s important to remember that the Fed does not control Treasury yields; that’s for the market to determine. They do control Fed Funds, which is ultra short-term; but the further we move out on the curve the more is up for debate from market participants.

This is governed by supply and demand, and the Treasury department is going to have to issue a considerable amount of longer-term debt next year to refinance debt that’s maturing. This will be at a higher rate, and also presents the potential for greater supply in long-dated Treasuries, which can impact prices as the greater supply pushes price lower. And given that these are Treasuries, lower prices mean higher yields.

So, the question as to whether yields have topped and whether the FOMC is done with rate hikes can actually carry two very different answers.

In the 10-year, we saw a strong response at 5%, indicating buying demand coming online as that yield was hit. But, there’s also been support at 4.5% and it would be too early to definitively say that this has topped.

US 10 Year Treasury Yields – Weekly Chart (indicative only)

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

Have Stocks Bottomed?

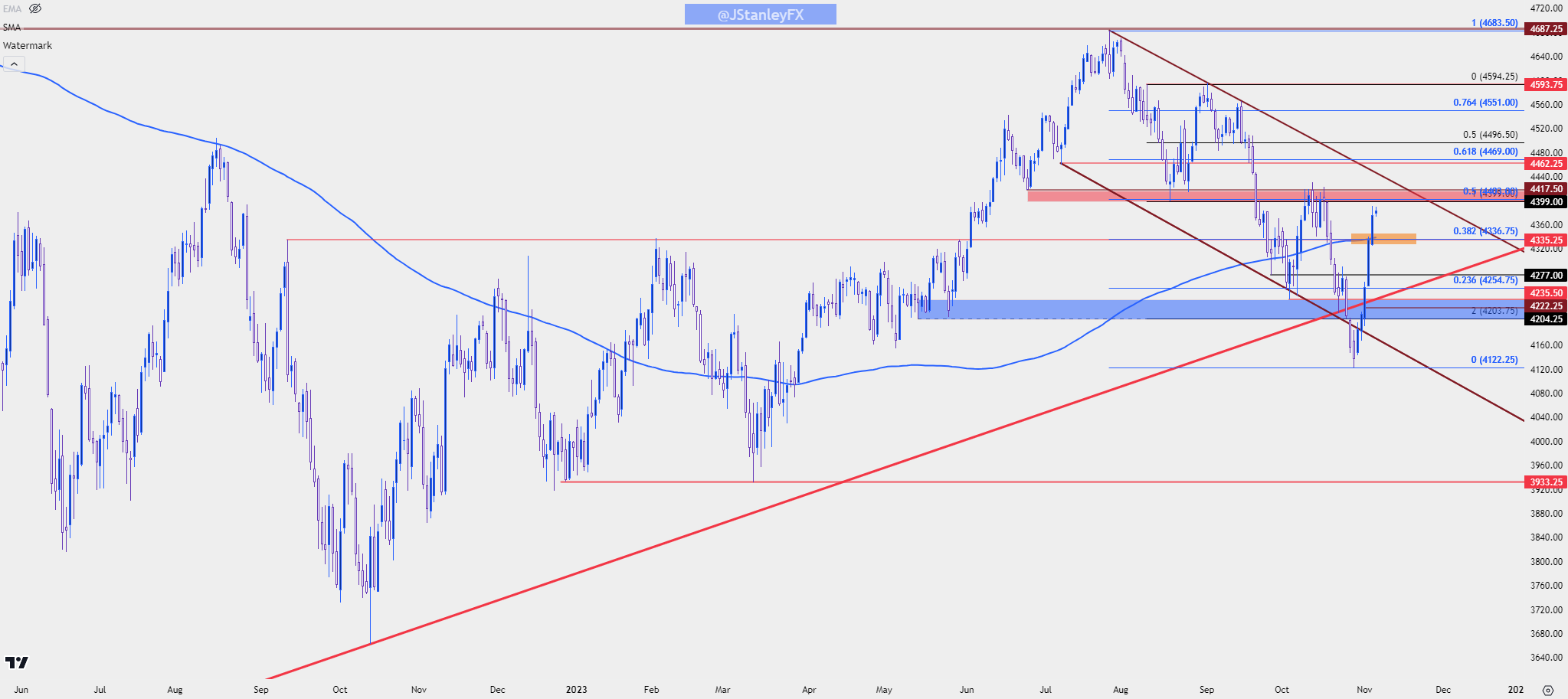

The S&P 500 put in its strongest week of 2023 last week, but it comes fresh on the heels of a stern sell-off that tested through a number of supports. Price is nearing re-test of a major zone of resistance, and this is the same spot that stopped bulls in their tracks in October, around the 4400-4417 area on the chart.

For support, there’s a Fibonacci level at 4336 that remains of interest, and if buyers show up to hold lows around that level, that could present as a higher-low for themes of bullish continuation.

S&P 500 Daily Price Chart (indicative only)

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

--- written by James Stanley, Senior Strategist

Latest market news

Today 04:10 PM

Today 12:30 PM

Today 09:44 AM

Today 09:34 AM

Latest Trade Ideas and Alerts articles

November 7, 2024 03:25 PM

May 1, 2024 04:50 PM

April 16, 2024 04:24 AM

April 15, 2024 06:08 AM