- Dollar outlook hinges on NFP as Fed’s decision is data-dependant

- Mixed NFP leading indicators and what are analysts expecting

- Wage inflation in services still a problem for the Fed

- Dollar analysis: Will USD continue pressing higher anyway?

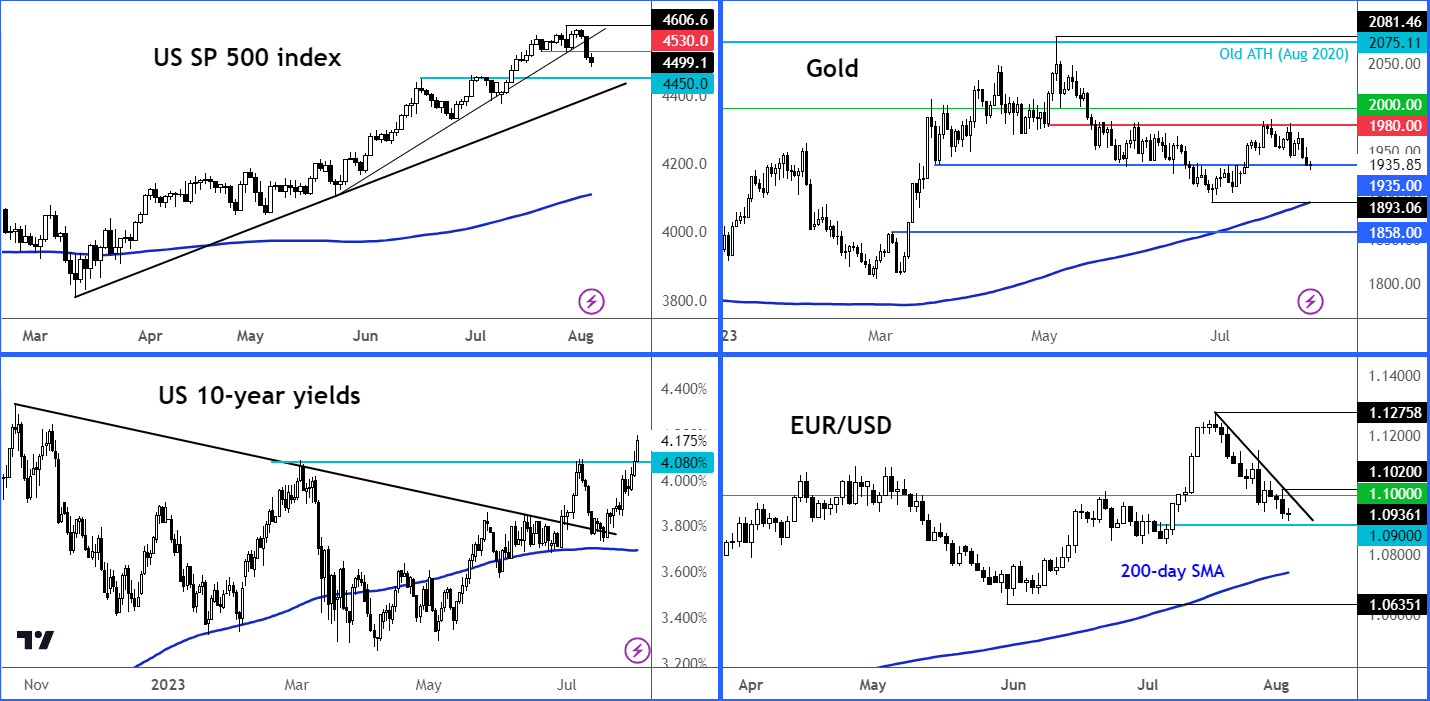

- NFP trade ideas: EUR/USD, Gold and S&P 500

All eyes will turn to the US jobs report on Friday, as the market refocuses on Fed policy after the Fitch downgrade of US credit rating caused a risk off response in the markets, which sent the dollar and long-dated bond yields surging higher. The US dollar, gold and EUR/USD outlook could be impacted if we see a jobs report that deviates significantly from expectations.

Why is this jobs report going to be important?

Employment reports are almost always important anyway, but this one is going to be even more so. Coming in a week before the CPI report, Friday’s jobs data is going to influence Fed’s policy, as Powell has made it quite clear that US monetary policy is now restrictive enough and that the next decision in September would be entirely data dependent. Until then, we will have two more inflation and a couple of jobs reports to consider, including this one. While the focus is clearly on inflation as employment is still very strong, any potential weakness in jobs data could cement expectations of a policy hold. But another surprisingly strong employment report would keep the threat of further Fed hikes alive. So, the dollar could move quite sharply this week, as the Fed is now watching data very closely in determining its next move on monetary policy.

What are analysts expecting?

- Headline jobs growth of 200K expected vs. 209K in June

- Unemployment rate is seen steady at 3.6%

- Average Hourly Earnings are seen printing +0.3% m/m vs. +0.4% last month or 4.2% y/y vs. 4.4% previously

Mixed NFP leading indicators

The leading indicators we have had this week have been quite mixed. While the ADP private sector payrolls report was strong, the employment components of both the ISM Services and Manufacturing PMIs weakened.

1. ISM Services PMI

- Headline: 52.7, Exp. 53.0, down from 53.9

- Employment 50.7, down 2.4 points from 53.1 in June

- (Also, disinflation is already evidently ending in the services sector: Prices Paid was up - 56.8 from 54.1)

2. ISM manufacturing

- Headline 46.4, Exp. 46.9, down from 46.0

- Employment 44.4, down 3.7 points from 48.1 in June

3. ADP private payrolls 324K vs. 191K eyed and 455K last

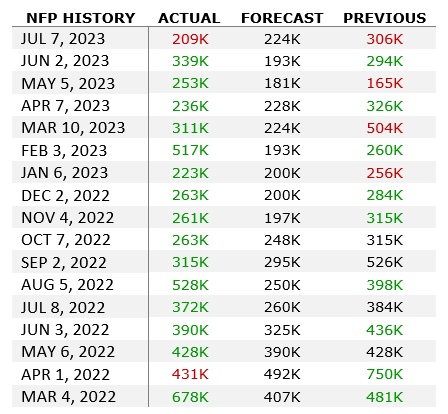

The overall picture from the pre-NFP leading indicators point to a jobs report roughly in line with expectations. But if you look at the recent history of the nonfarm payrolls report, we have consistently seen better-than-expect results, although lately they have either been subsequently revised lower or in the case of the June report, missed expectations…

Wage inflation in services still a problem for the Fed

It is important to consider the whole picture and take into account average hourly earnings when it comes to trading the NFP. On the latter front, we have seen earnings increase by 4.4% year-on-year in April, May and June 2023. This shows that wage inflation is still going strong, and it is a concern for the Fed. This is especially the case for the services sector – which was also highlighted by the rise in prices paid index of the ISM services PMI. Another strong showing in wages data would be considered a dollar-bullish jobs report, even if we see a small miss in headline employment.

Dollar analysis: Will USD continue pressing higher anyway?

The further strengthening of the US dollar so far this week has nothing to do with the Fed’s expected policy decision. It has a lot to do with the sell-off in US bond market, especially at the long end of the curve. This has been triggered by that rating downgrade by Fitch, causing investors to demand more for the increased risks associated with holding Treasurys. While a US debt default is unthinkable, it could happen at some future point in time. So, we wouldn’t rule out the possibility of further increases in US bond yields in the near-term. It will be interesting to watch next week’s $103 billion bond auction. This will tell us a lot about investors’ willingness to hold government debt. That said, the correction potential for the dollar is now high, and investors may soon start selling USD once the dust settles down – and especially if Friday’s jobs report comes in weaker.

What else will markets focus on?

Once the jobs report is out of the way, investors will turn their attention towards more inflation data, due in the following week. As mentioned, we will have already had the wages data from the employment report, but CPI is going to be important next Thursday. US inflation has fallen sharply in recent times, printing below-forecast readings in each of the past 4 months. Annual CPI fell to just 3.0% in June from around 6.5% at the start of the year, increasing the likelihood that interest rates have now peaked.

The Fed’s policy decision in September will be entirely data dependent. Until then, we will have one more inflation and jobs report after this. Any further weakening of CPI could cement expectations of a policy hold.

NFP trade ideas: EUR/USD, Gold and S&P 500

If the employment and wages data come in lower, we would favour looking for long setups in gold or the EUR/USD, while a stronger report would boost the appeal of the USD/CHF. A goldilocks report is what stock market investors would be looking for – something not too hot to warrant a rate increase, and not too cold to raise recession alarm bells.

Source: TradingView.com

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Latest NFP articles

December 6, 2024 05:13 PM

December 5, 2024 03:26 PM

October 31, 2024 06:41 PM

October 31, 2024 01:30 PM