- The events calendar is scare locally and internationally for AUD/USD this week

- NIvidia earnings loom as a risk for broader markets

- AUD/USD was heavily influenced by Chinese stocks and USD/CNH before Lunar New Year holidays. The return of those markets may influence how the AUD/USD fares

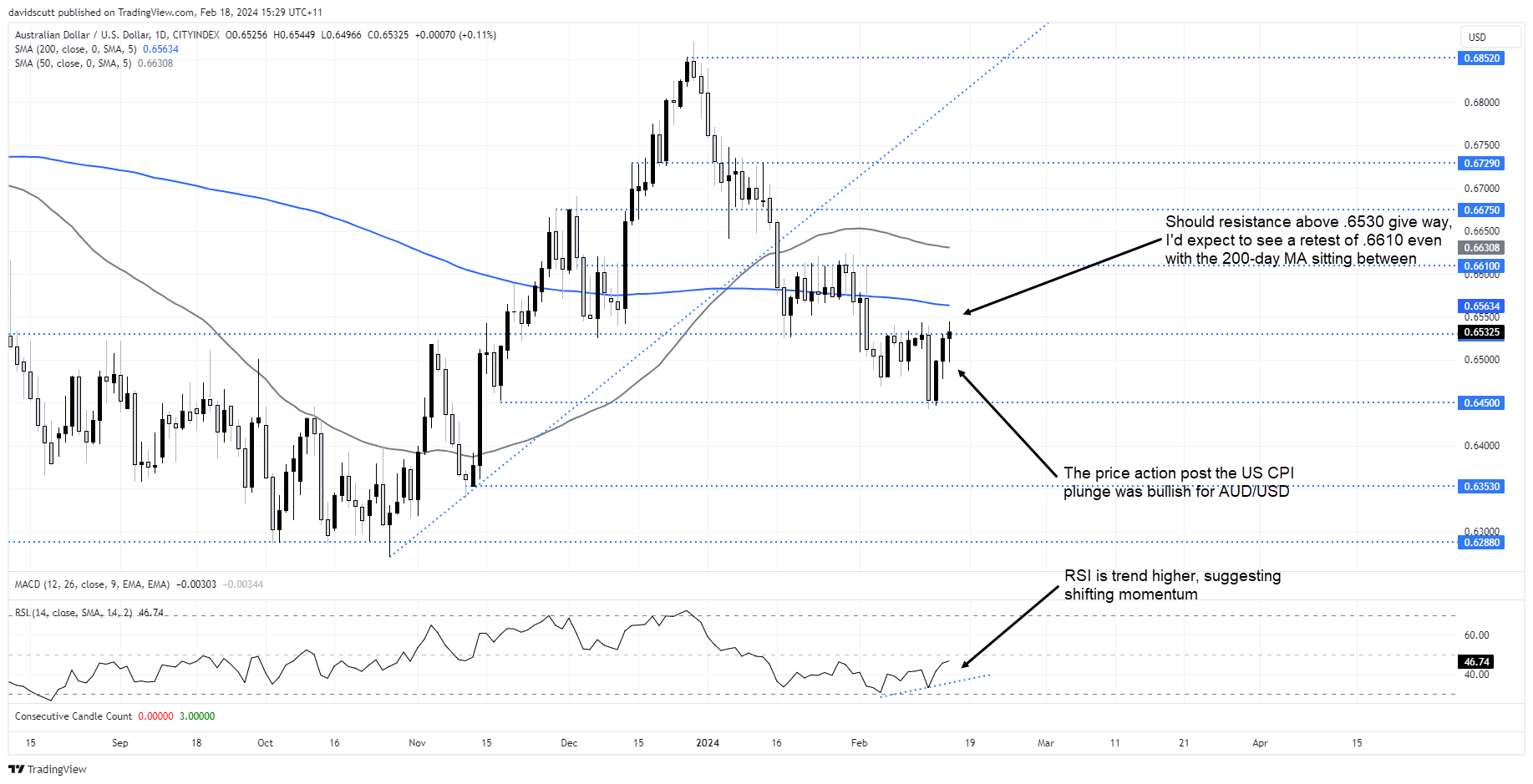

The near-term fortunes of AUD/USD look set to be dictated by offshore factors given a lack of domestic drivers. The performance of Chinese markets may be influential, especially during Asian trade. With the US dollar unable to find traction despite shorter-dated US yields rising to the highest level since mid-December, there age grounds to suggest AUD/USD may be able to break stubborn resistance located above .6530 in the days ahead.

Few major events on the known risk calendar

While there’s a bit on the data calendar in Australia, none of the reports screen as major risk events in the absence of big upside or downside surprise.

The minutes of the RBA’s February monetary policy meeting will be released Tuesday but having already heard from Governor Michele Bullock on several occasions since it was held, they come across as stale. 24 hours later, the Q4 wage price index report will arrive to much fanfare but it’s unlikely to move the dial for AUD/USD. Having written about or traded around the ages report since inception, I can tell you it almost never strays too far from consensus and almost never moves the Aussie dollar.

The rest of the domestic calendar comes across as noise rather than potential signal generators.

Internationally, the events calendar is also quiet in the States, Europe and China. Unless China’s Loan Prime Rates (LPR) are lowered on Tuesday – which isn’t expected – there will be few implications for AUD/USD. The FOMC January meeting minutes on Wednesday has the potential to surprise, but just like the RBA minutes, are they still relevant given the data flow since? Probably not.

Flash PMIs in the States and Europe on Thursday may spice things up, especially if they suggest a reacceleration in momentum in the US economy. Elsewhere, there’ll be long bond auctions in the US, Japan and UK. While they haven’t shifted markets meaningfully in a while, you can never be quite sure whether demand will turn up with the fiscal trajectory of some governments.

While slightly left of field for FX forecasting, Nvidia’s earnings report after market close on Wednesday could easily be the biggest known risk event for the Aussie and broader markets given it’s the posterchild of the AI-led tech rally.

AUD/USD eyes China market reopening

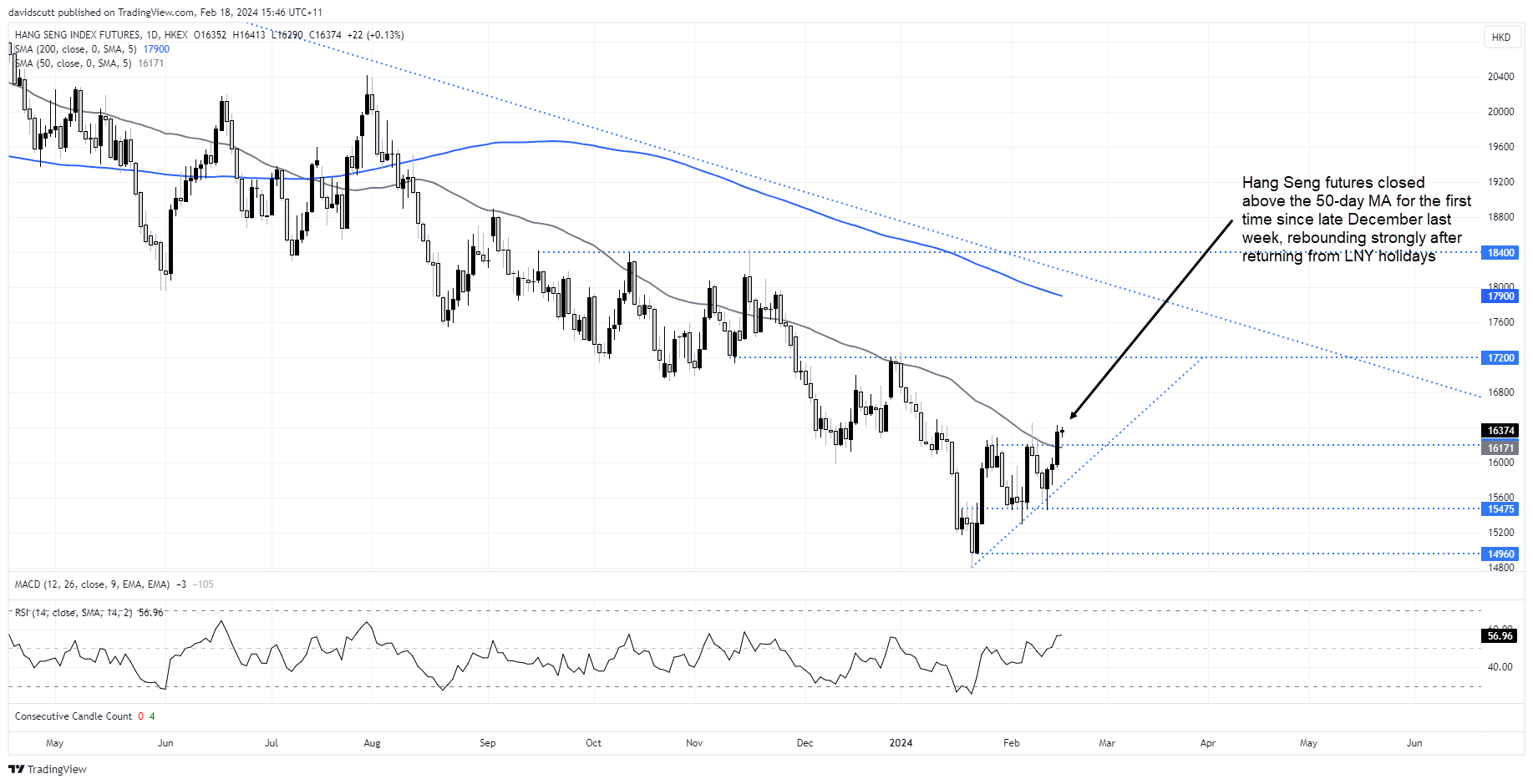

The great unknown for AUD/USD this week is how Chinese markets will return from the weeklong Lunar New Year holiday. Will stocks be able to extend their rebound, building confidence the rescue launched by the government is working? And will the People’s Bank of China push back against US dollar strength through the daily USD/CNY fix?

Given the relationship with Chinese markets prior to the New Year, the answer to those questions looms as potential answer to how the AUD/USD will perform. Hong Kong’s Hang Seng has rallied since returning on Wednesday, so perhaps that provides some clues on directional risks.

USD not finding as mush support from higher US yields

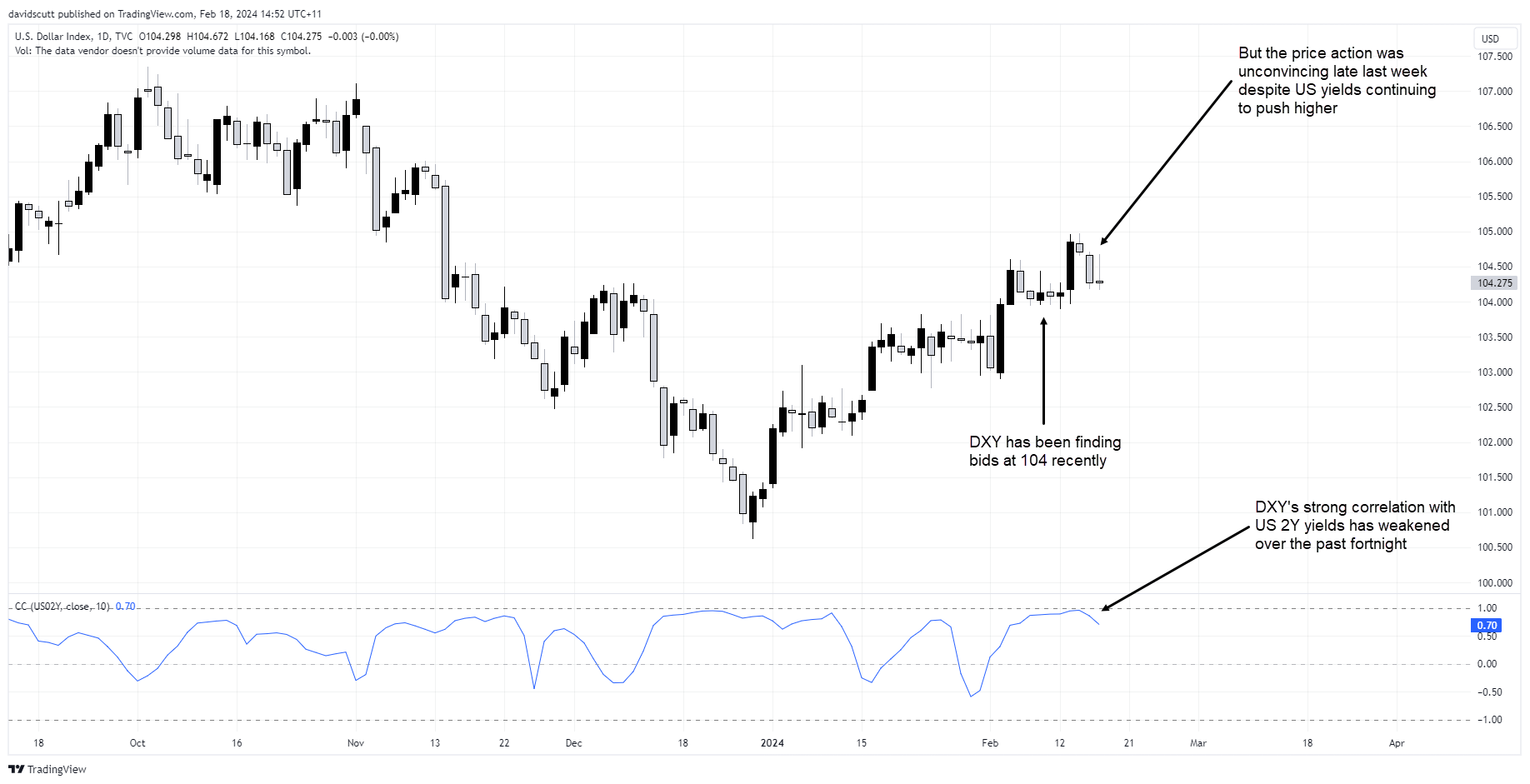

Another positive for the AUD/USD is the US dollar is showing signs of fatigue after rallying more than 4% since December, including in each of the past five weeks. For much of 2024, the US dollar index (DXY) was finding support from rising US shorter-dated yields, gaining against most major currencies as yield differentials widened. However, despite a hot CPI and PPI report for January, the DXY struggled late last week, easing lower on Friday despite two-year yields closing at the highest level since mid-December.

While technical support is evident at 104 on the daily, the unconvincing price action on Friday, coupled with the DXY’s correlation with US two-year yields declining to 0.7 over the past fortnight, suggests further upside in the big dollar may be tough near-term.

Commodity prices, AUD may rally if USD softens

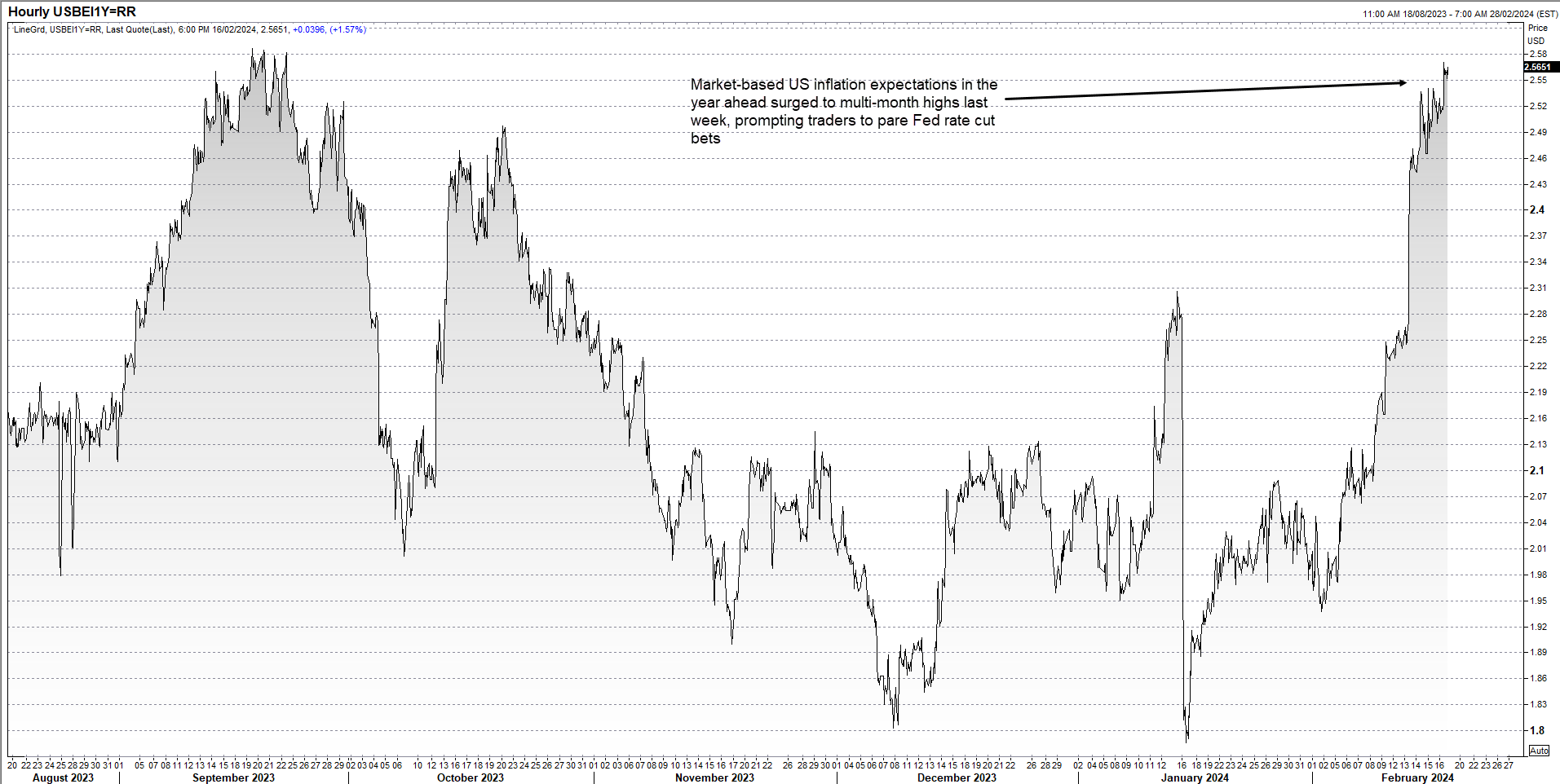

Should the DXY begin soften, it may also help commodity prices push higher, providing another positive for the Aussie. It was noteworthy to see base, precious and energy commodity prices rally on Friday as US one-year inflation expectations – which track market expectations on the average inflation rate over the next 12 months – surged to highs not seen since September. Typically, commodities tend to outperform during inflationary periods.

Source: Refinitiv

AUD/USD seeking higher range

After plunging over 1% following the US CPI report last Tuesday, the price action in AUD/USD since has been entirely bullish, rebounding strongly from horizontal support at .6450 to be back testing resistance parked above .6530.

While it was again thwarted above this level on Friday, the bullish hammer candle suggests there may be more conviction behind this latest attempt higher. With an expectation Chinese equities may rally when they come back online, we could see sellers above .6530 overwhelmed should that scenario play out.

Above, AUD/USD has a checkered track record at the 200-day moving average, sometimes respecting it while other times totally ignoring it. For mine, should we see an upside break, I’d expect to see resistance above .6610 tested before too long. On the downside, minor support is found at .6500 with more pronounced buying located 50 pips lower at .6450.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Yesterday 10:18 PM

Yesterday 10:16 PM

Yesterday 09:00 PM

Yesterday 08:00 PM

Yesterday 07:39 PM

Yesterday 07:00 PM

Latest AUD articles

May 6, 2024 06:05 AM

April 30, 2024 02:37 AM

April 24, 2024 06:51 AM

April 24, 2024 02:03 AM