- AUD/USD fully embraced the risk-off tone during its worst week since November at -2%

- A carry-trade unwind saw AUD/JPY plunge -4.3% during its worst week since the pandemic

- AUD/USD may have snapped a 9-day losing streak on Friday, thanks to a bounce on Wall Street, gold and copper prices

- But the bruised and battered Aussie may struggle to gain bullish traction without a broad risk-on rally and weaker US dollar

- We could be in for a choppy week after such a strong selloff

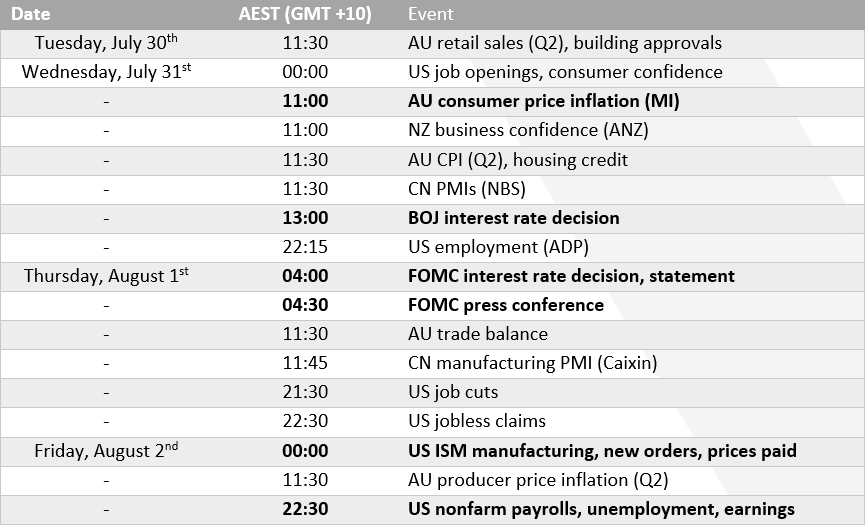

Australia’s Q2 inflation report on Wednesday is the key domestic event next week. While producer prices are released on Friday, markets would likely have decided already whether the RBA will hike again in August, based on the CPI data alone. Firm employment and rising monthly inflation data have kept the RBA’s hawkish tone in their statement, although bets of multiple Fed cuts and a slightly dovish RBNZ have alleviated the pressure of any RBA action. Although a hot set of inflation figures could quickly change things and see markets reprice a potential hike. Still, there is hope with NZ inflation data coming in softer than expected, given it tends to move in tandem with AU inflation data over the longer term. What the RBA really want to see is lower services inflation. RBA cash rate futures currently imply a 20% chance of a hike, down from 44% a few weeks ago.

Bets have been rising that the BOJ could hike rates next week. That’s all well and good, but when AUD/JPY has already fallen -9% over the past 2 weeks, it leaves little in the room for a surprise. And with the BOJ consistently falling short of expectations in meetings this year, no action would not be a huge shock. Which could spur yen weakness after a rare bout of strength. Either way, AUD/JPY and of course AUD/JPY could get caught in the crossfire of the BOJ and FOMC next week.

The Fed may need to signal cuts next week to keep current market pricing in place. Fed funds futures imply up to three cuts by December, but there are only four meetings remaining until the end of the year. And that means we need to hear a relatively dovish tone (if not a cut) next week to justify the current market pricing. Failure to do so could strengthen the US dollar and weaken AUD/USD.

The potency of ISM and NFP reports are contingent on the FOMC meeting. If the Fed come out swinging and cut, or even signal a cut, the ISM and NFP reports are less relevant. But if they keep us guessing as to what the September meeting will bring, these reports will take centre stage on Friday. And the usual rules should apply: Weak data justifies cuts, strong data doesn’t, and AUD/USD will likely move inversely to the data.

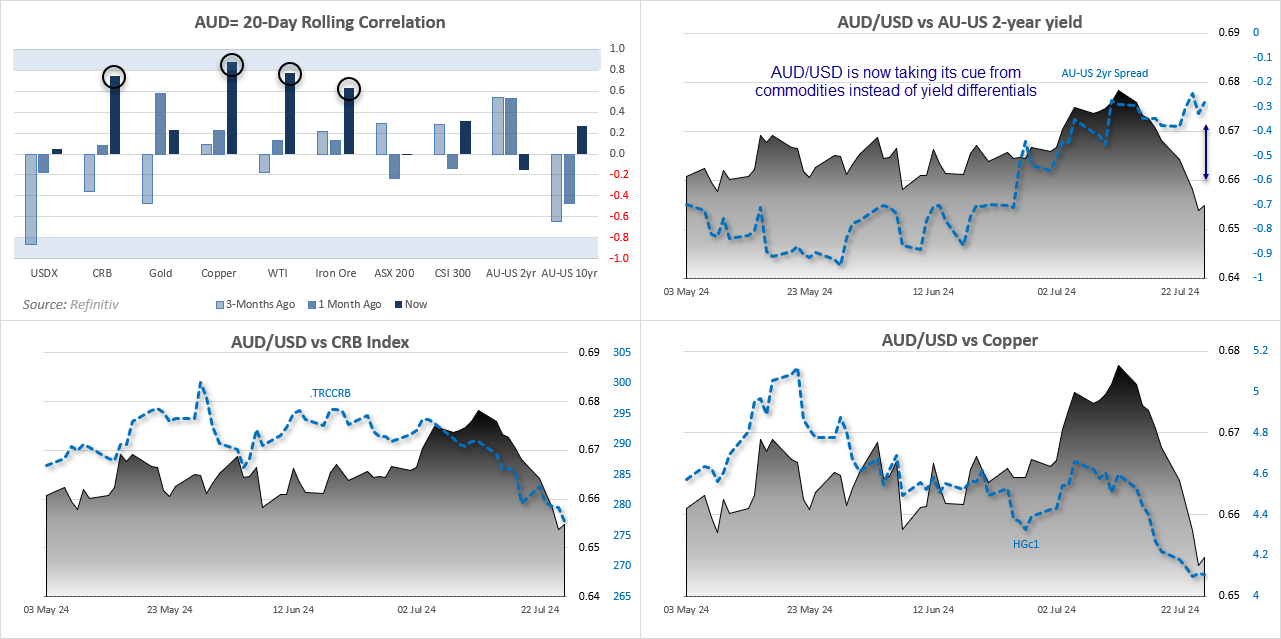

AUD/USD 20-day rolling correlation

- Last week I wrote how that yields differentials and Fed policy were no longer the key drivers of sentiment, and the correlation charts perfectly encapsulate this

- The correlation between the US dollar index (USDX) and AUD/USD is non-existent

- Yet AUD/USD now shares a strong correlation with commodity prices, particularly copper (0.88) and WTI crude oil (0.77)

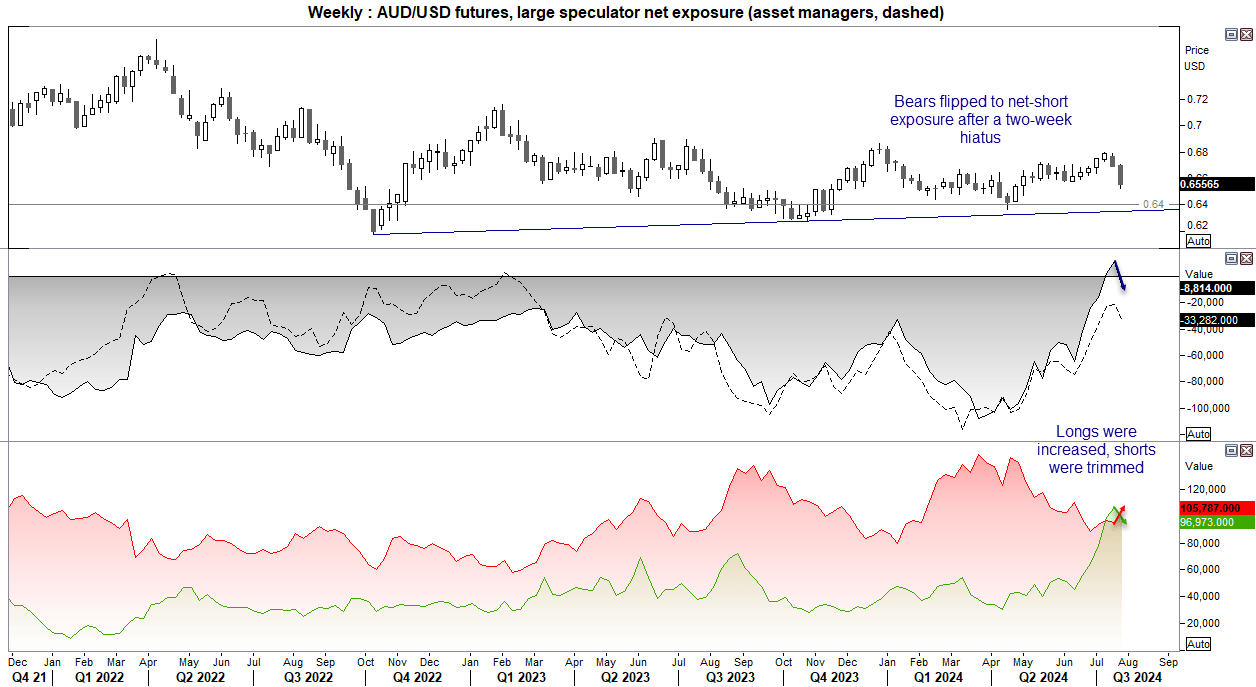

AUD/USD futures – market positioning from the COT report:

It seems asset managers were correct to remain net-short AUD/USD futures, looking at how large speculators reverted to net-short exposure after a two-week hiatus. Bears added 10.6k contracts and bulls removed 9.4k, and with momentum now behind the bear camp then a move towards 64c over the coming weeks seems plausible.

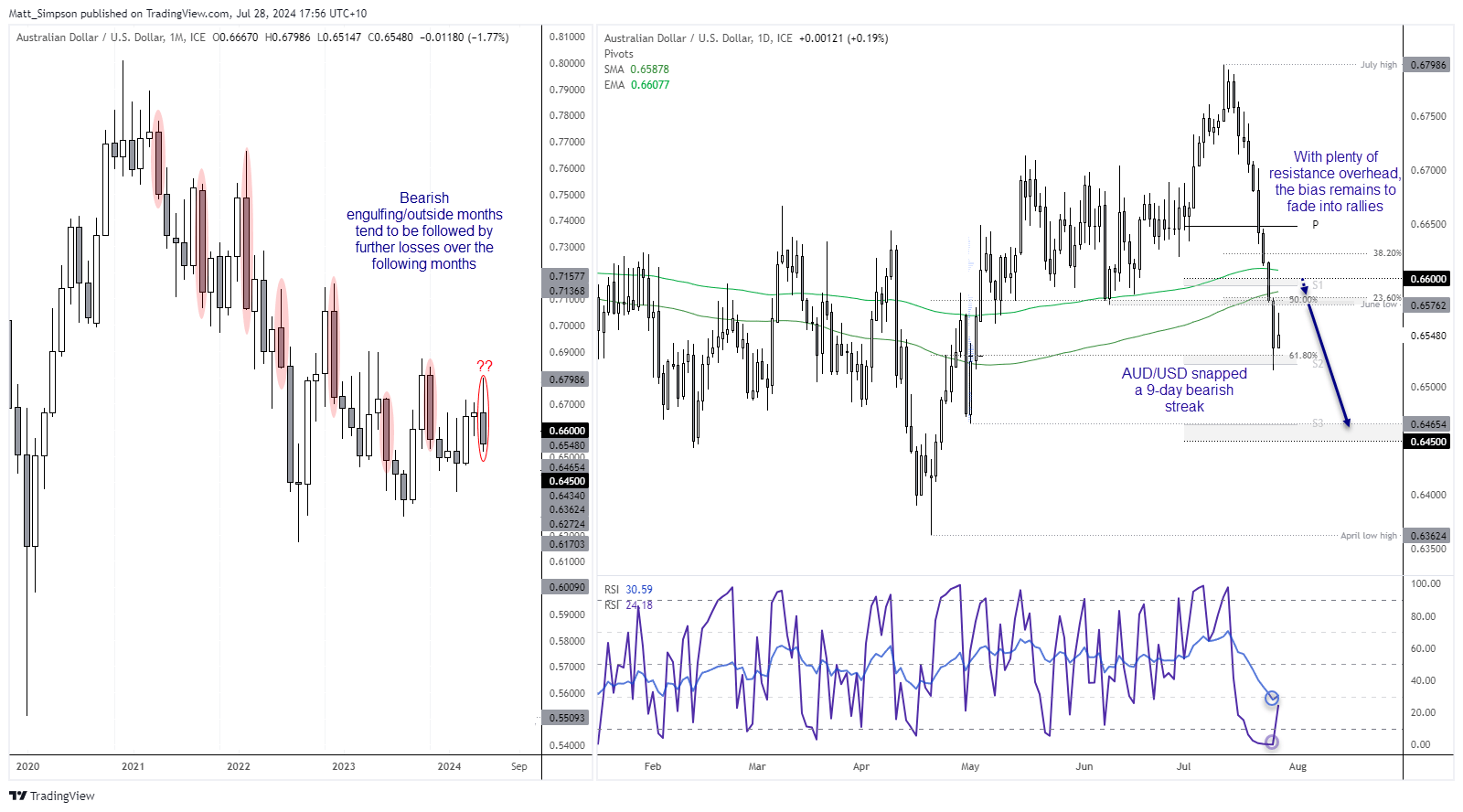

AUD/USD technical analysis

The Australian dollar is on track for its first bearish outside month since February 2023, when it went on to decline for the next three months. The prior bearish outside month in April 2022 marked the beginning of a -19.5% decline between the April 2022 high and the October low. For comparison, that would send AUD/USD below 55c if such a move were to be repeated from this month’s high. Thankfully, I do not expect this to be the case, but momentum is clearly favouring bears for now.

The daily chart shows support was found around the 61.8% Fibonacci level and monthly S2 pivot point. RSI (14) and (2) reached oversold on Thursday ahead of Friday’s sympathy bounce, which snapped a 9-day losing streak. Yet there is a plethora of resistance levels around the 0.6575 – 0.6600 zone, including the 200-day MA/EMA, 23.6% Fibonacci level, 50% retracement level, monthly S1 and 66c handle. The bias is to fade into rallies towards resistance in anticipation of a move down to 0.6550 and the 0.6450/65 support zone.

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Yesterday 07:31 PM

Latest AUD/USD Weekly Outlook articles

December 15, 2024 10:54 PM

December 8, 2024 11:51 PM

December 1, 2024 11:06 PM

November 25, 2024 12:31 AM