- AUD/USD remains a sell-on-rallied play, for now

- Recent underperformance largely reflects homegrown factors in Australia

- So dramatic has the recalibration in US interest rate expectations been, it may be hard for US yields to push higher near-term, starving the USD rally of oxygen

AUD/USD remains a sell-on-rallies prospect for now, continuing to slide on the back of softer domestic data and rethink of when the RBA may begin cutting interest rates relative to the US Federal Reserve. However, with the USD and shorter dated US yields looking toppy after their run higher, the bearish playbook for AUD/USD may not be the right one for traders in the not-too-distant future.

AUD/USD battling homegrown headwinds

Rather than offshore factors which typically drive AUD/USD movements, the latest bout of weakness largely reflects homegrown factors, especially if neighbour New Zealand is included. Australia’s inflation indicator for January undershot expectations, continuing the disinflationary trend seen in the second half of last year. The expected surge in retail sales in January also never materialised, coming in well under expectations after a soft December quarter.

Across in New Zealand, the RBNZ delivered a dovish surprise for markets still looking for another rate hike this year, lowering its implied probability of another move while sounding more confident demand and supply are now better aligned. Having been one of the last holdouts when it comes to hawkish outlooks, the move from the RBNZ was immediately extrapolated across to the RBA, another central bank who, for now, retains a weak tightening bias.

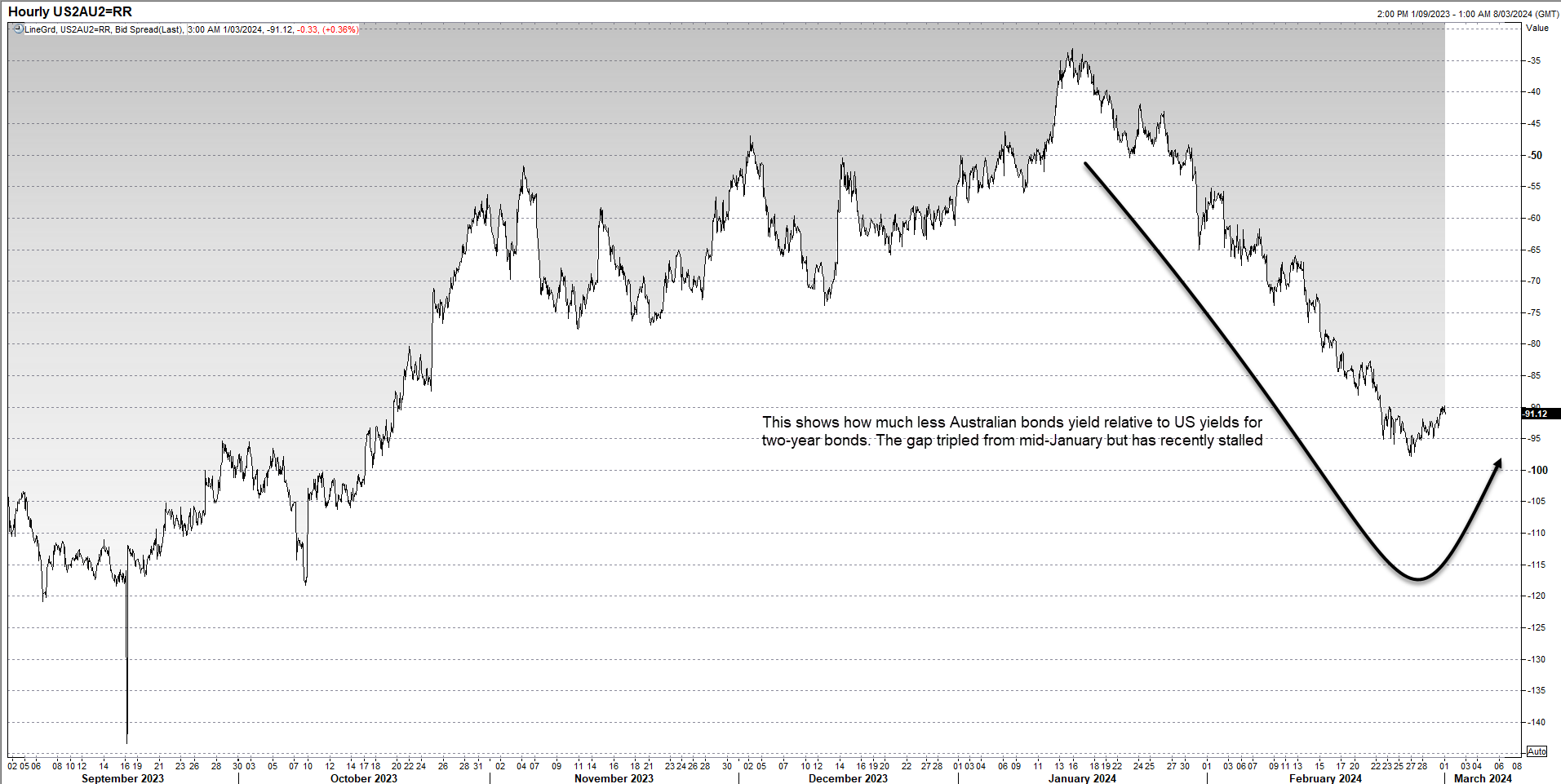

Central bank rate outlooks are converging

Right now, overnight index swaps see the first RBA rate cut arriving in August with a meaningful risk it could be in June or even May. The Federal Reserve is tipped to begin its easing cycle in June, with a risk it could be delayed until July. Three and a half cuts are currently priced into the US curve, just half the amount seen just six weeks ago.

The convergence in rate outlooks has seen the yield differential between US and Australian two-year yields balloon out to over 90 basis points in favour of the former, contributing to the soggy AUD/USD performance.

Source: Refinitiv

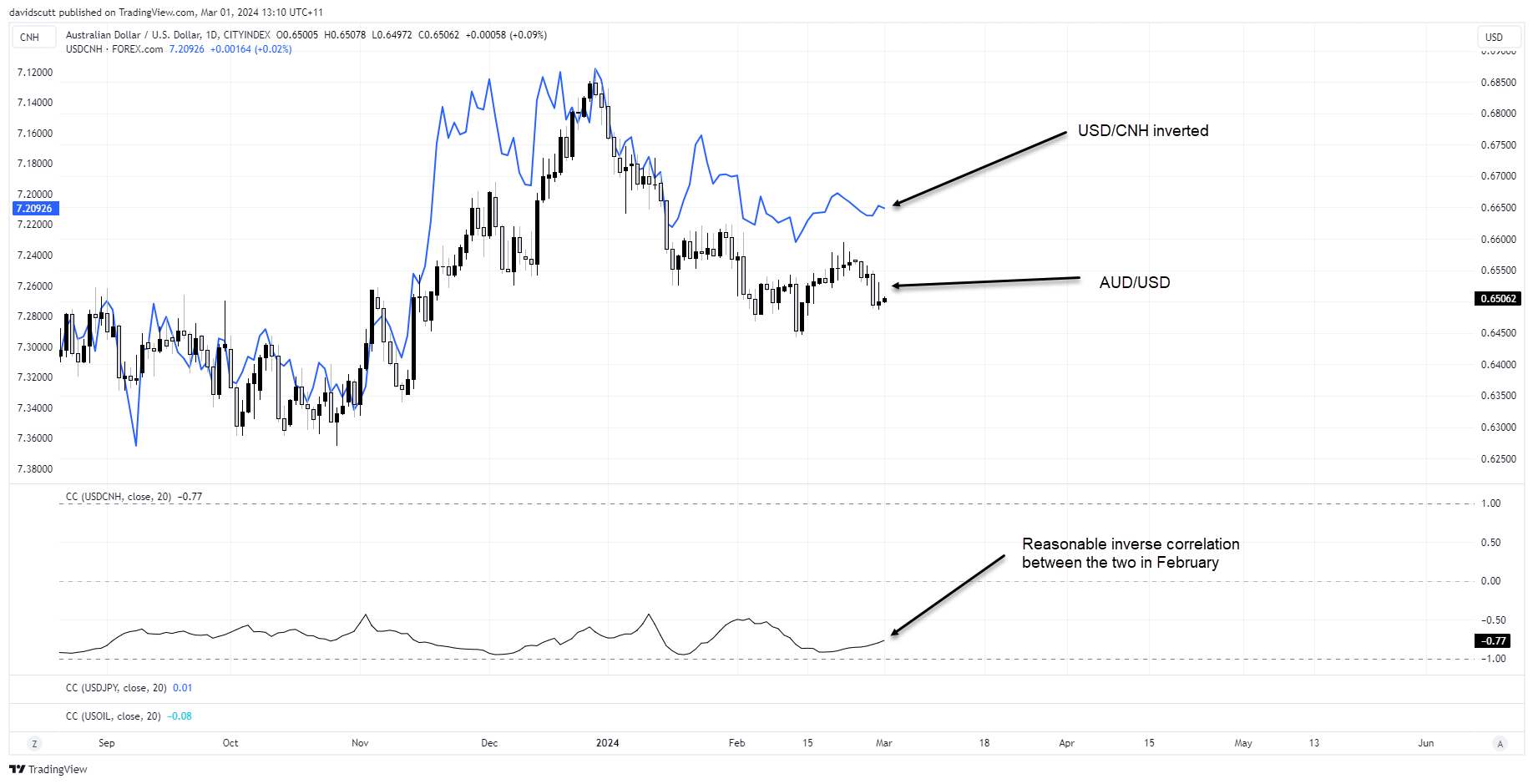

AUD remains a China proxy

The inability of other Asian currencies to find traction against the USD is also hindering the Aussie with the daily correlation between AUD/USD and USD/CNH sitting in the mid-0.7s in February. Clearly, AUD traders are still using it as a China proxy.

The fundamental headwinds, combined with the weak technical picture on the charts that I’ll touch on shortly, suggests AUD/USD remains a sell-on-pops play.

But I can’t get too bearish around these levels given the repricing of US inters rate expectations has already been significant. It will likely take the data to push Fed officials to stop talking about rate cuts to deliver another leg higher for yields. And if yields can’t push higher, it’s a stretch to say the USD rally will continue in the absence of a major risk-off event.

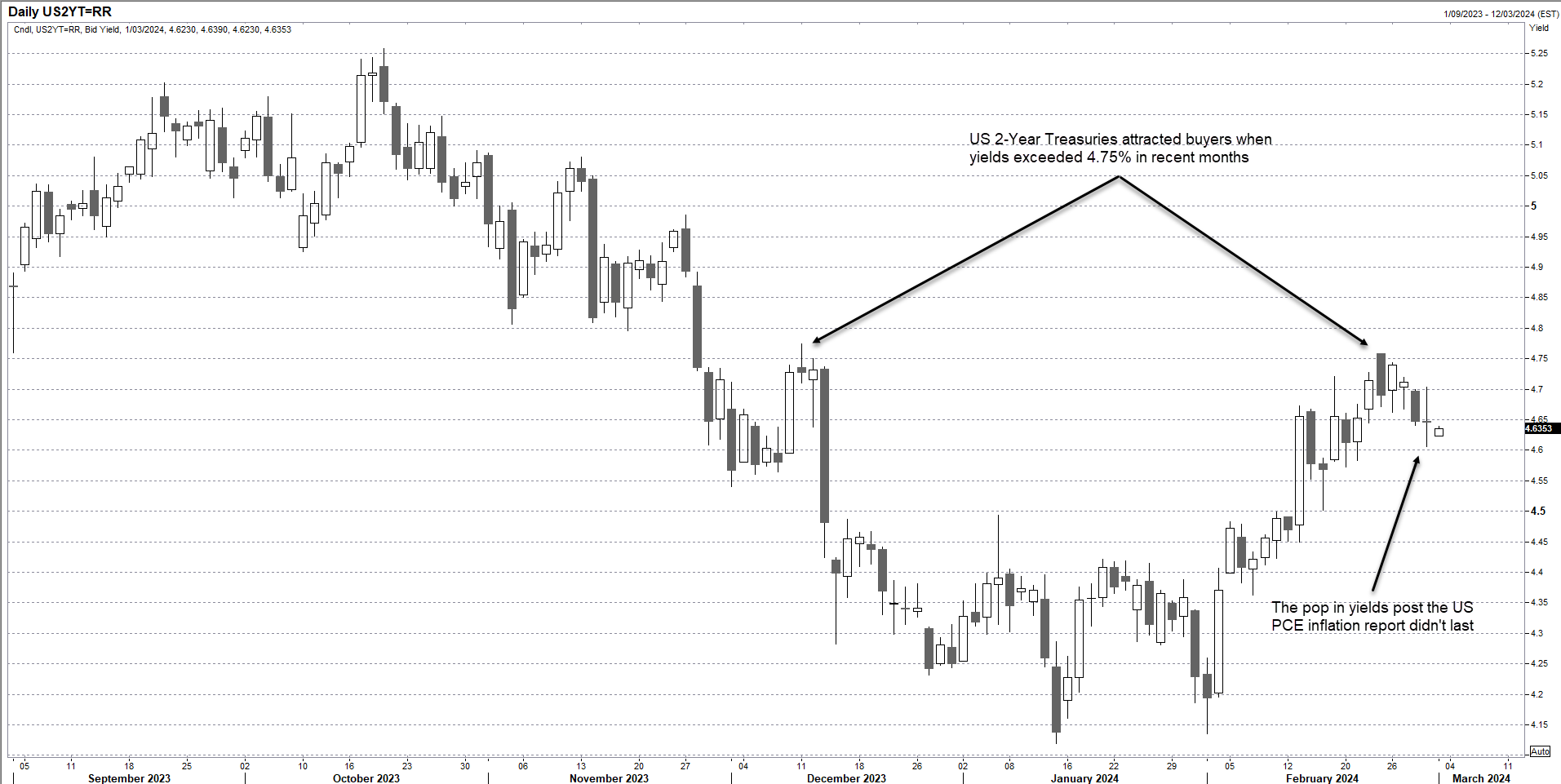

US yields looking toppy after rate recalibration

There’s already signs we may have seen the top for shorter-dated US yields near-term. Just look at the performance on Thursday to the hottest increase for the Fed’s preferred underlying inflation in the past year. They fell and extended the move into Friday. While there are numerous known risk events ahead next week, including appearances from Jerome Powell and February non-farm payrolls, none screen as particularly influential when it comes to the near-term US rate outlook unless we see a big deviation from the data or Fed messaging, That’s unlikely.

As for what that means for the AUD/USD, while there may be further modest downside near-term given how poorly it’s traded recently, the time to revert to buying dips rather than selling rallies may not be far away.

AUD/USD outlook

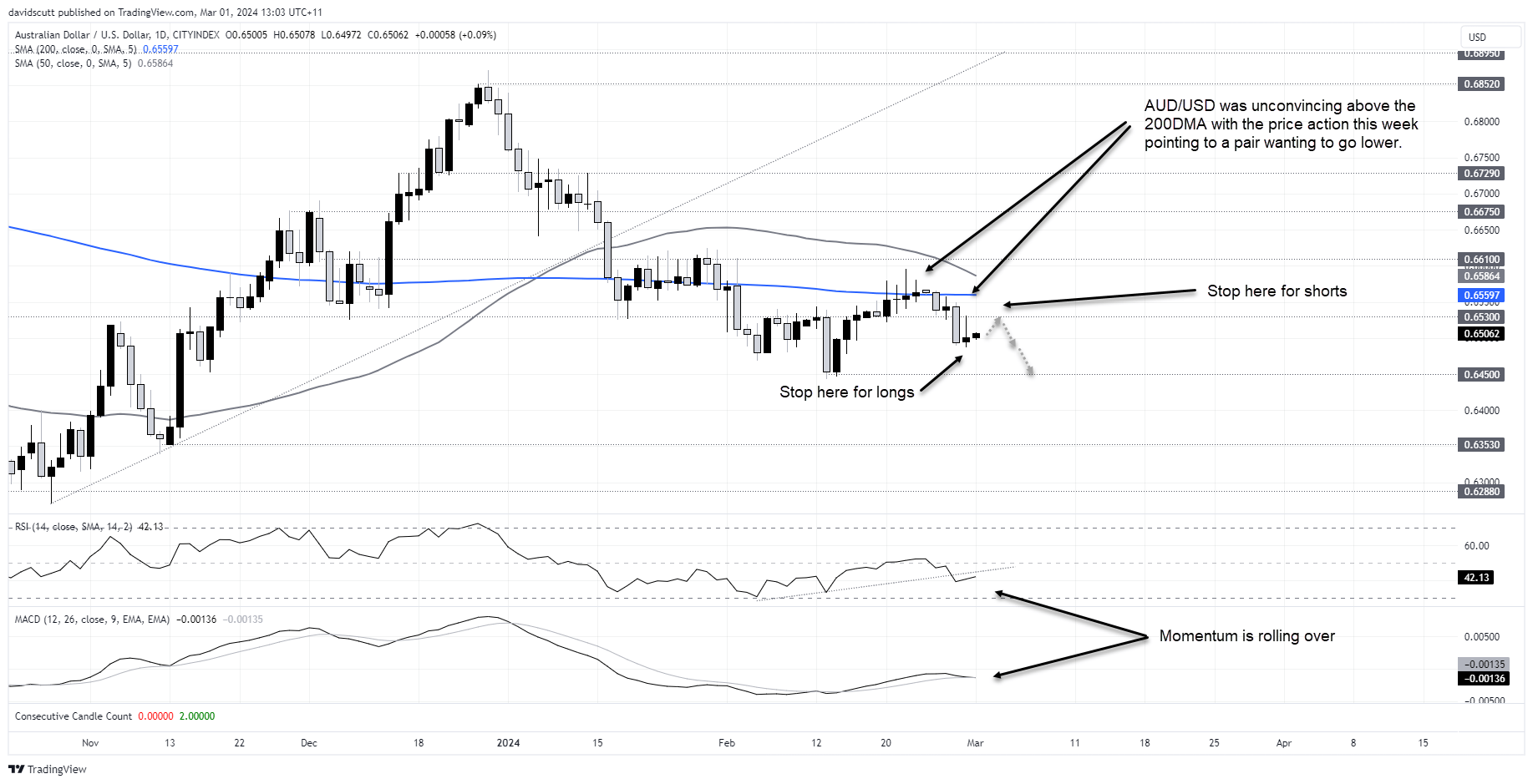

AUD/USD looked terrible at the 200-day moving average in February, making several probes above before getting smashed lower. And when it eventually managed to close above, it lasted just one session before sinking lower once more.

The bearish candle printed on the day the soft Australian inflation report and RBNZ rate decision were announced took AUD/USD straight through support at .6530. It followed that up with the inverse hammer candle on Thursday after failing to reclaim .6530. With the uptrend in RSI broken and MACD crossing from above, momentum appears to be shifting lower.

If we see another retest and failure at .6530, that gives a decent setup to go short targeting a move to .6450 with a stop above for protection. In between, AUD/USD has attracted bids recently around .6490, so that level should be on the radar. Traders not prepared to wait could also go long at .6500 targeting a move to .6530. A stop below .6490 would provide protection.

Unless the price action tells me otherwise, I’d be wary looking for downside beyond .6450 given my views on the US rate outlook. If that proves to be correct, the likely risk-on environment it would create argues for AUD outperformance.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Yesterday 10:18 PM

Yesterday 10:16 PM

Yesterday 09:00 PM

Yesterday 08:00 PM

Yesterday 07:39 PM

Yesterday 07:00 PM

Latest AUD articles

May 6, 2024 06:05 AM

April 30, 2024 02:37 AM

April 24, 2024 06:51 AM

April 24, 2024 02:03 AM