My hunch for a disappointing set of USD inflation data was incorrect, as traders enjoyed a double dose of softer inflation and retail sales figures. Even if data was mostly in line with expectations. Core CPI slowed to its slowest pace since April 2021 at 3.6% y/y, or 0.3% m/m – both as expected. Retail sales slowed to 0.3% m/m, compared to 0.4% prior and expected. Core retail sales was downgraded to 0.9% m/m from 1.1% although reached the 0.2% estimate. Whilst this is a step in the right direction, it should be remembered that prices are still rising and consumers are still spending.

Fed member Goolsbee added to the excitement of cuts by saying that “if decreases in housing inflation seen in April CPI data continues, that’s great”. Yet annual inflation levels remain well above the Fed’s 2% target, and we may have some more bumps in the road before they hit it. Still, for now traders got what they wanted, and that weighed on US yields and the dollar overnight.

USD dollar technical analysis:

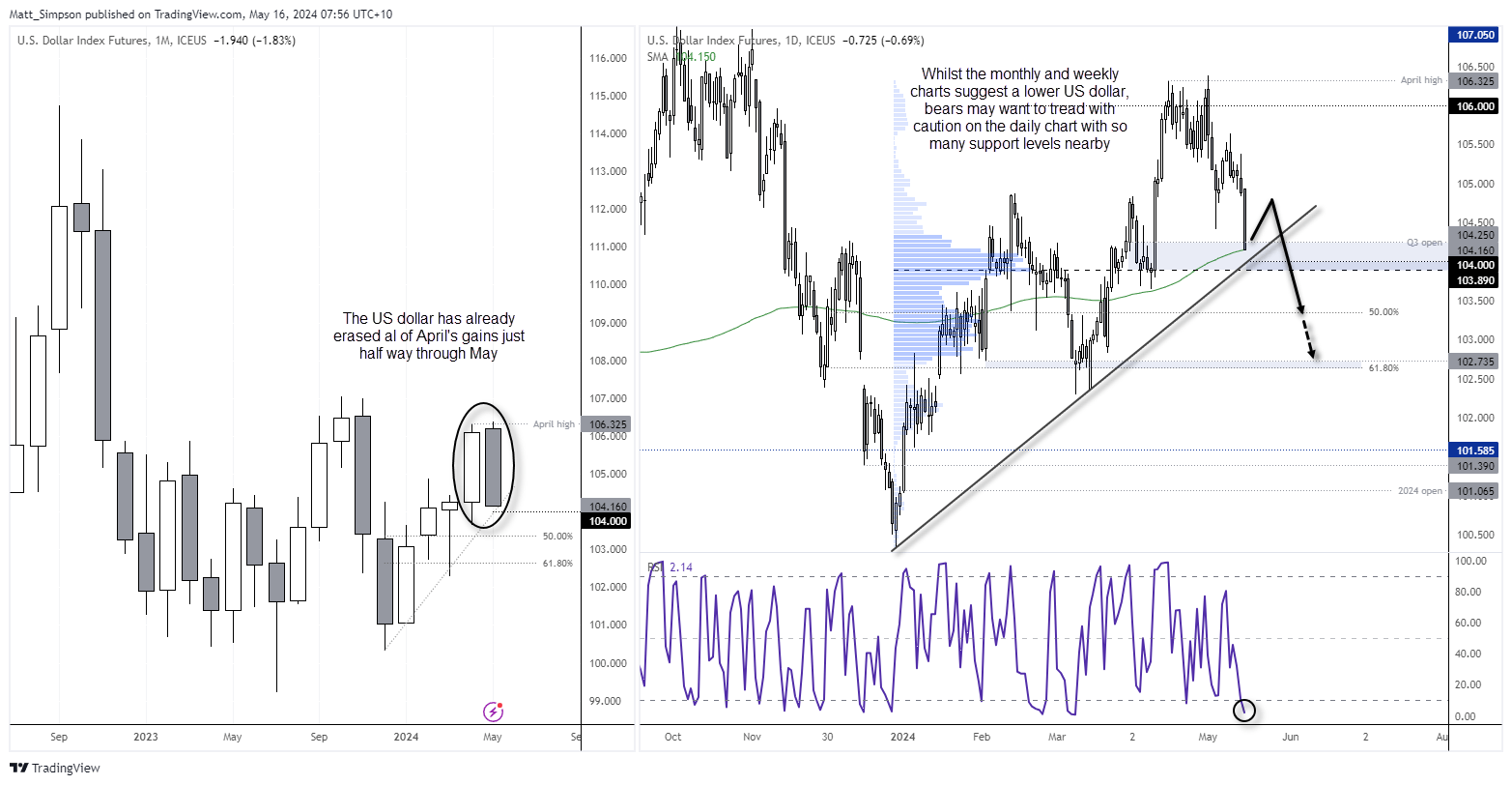

The US dollar index suffered its worst day of the year to safely claim ‘weakest FX major’ currency of the day. All of April’s gains have evaporated with May now on track for a bearish engulfing month at current levels. And if US data continues to soften, even modestly, bets are on for two 25bp Fed cuts this year.

However, the daily chart shows that support was found almost perfectly at the 200-day average, just beneath the Q3 open. Trend support is also nearby, in close proximity to the 104 handle and high-volume node. Furthermore, the daily RSI (2) is oversold. So whilst the monthly and weekly charts points to a lower US dollar, bears may want to trad with caution around current levels with so much support nearby.

- Fed fund futures are now implying a 52.7% chance of a 25bp in September (or a 99.3% chance of a cut by September)

- Wall Street wasted no time sending indices higher with the S&P 500, Dow Jones and Nasdaq 100 all reaching new record highs

- The ASX 200 futures market (SPI 200) tracked Wall Street higher overnight and shows the potential to reach the 7866 target mentioned in yesterday’s report

- The US dollar was the weakest FX major, sending the USD index beneath the 104.30 target (but is not trying to fund support around its 200-day average)

- EUR/USD closed at a 2-month high and is less than 20-pips from testing the 1.09 handle

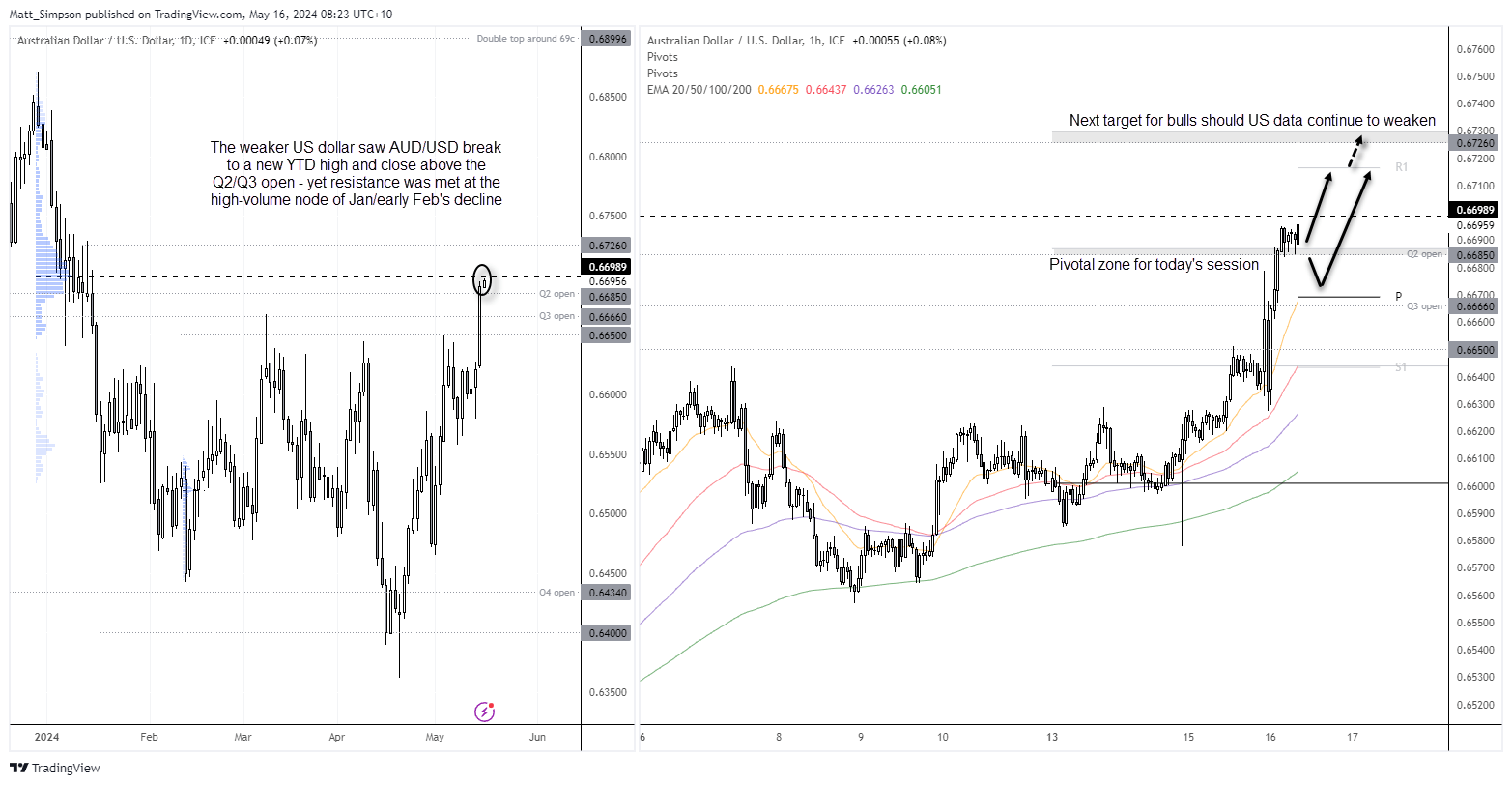

- AUD/USD broke above its key resistance zone around 0.6650 – 0.6660 to reach a new YTD high

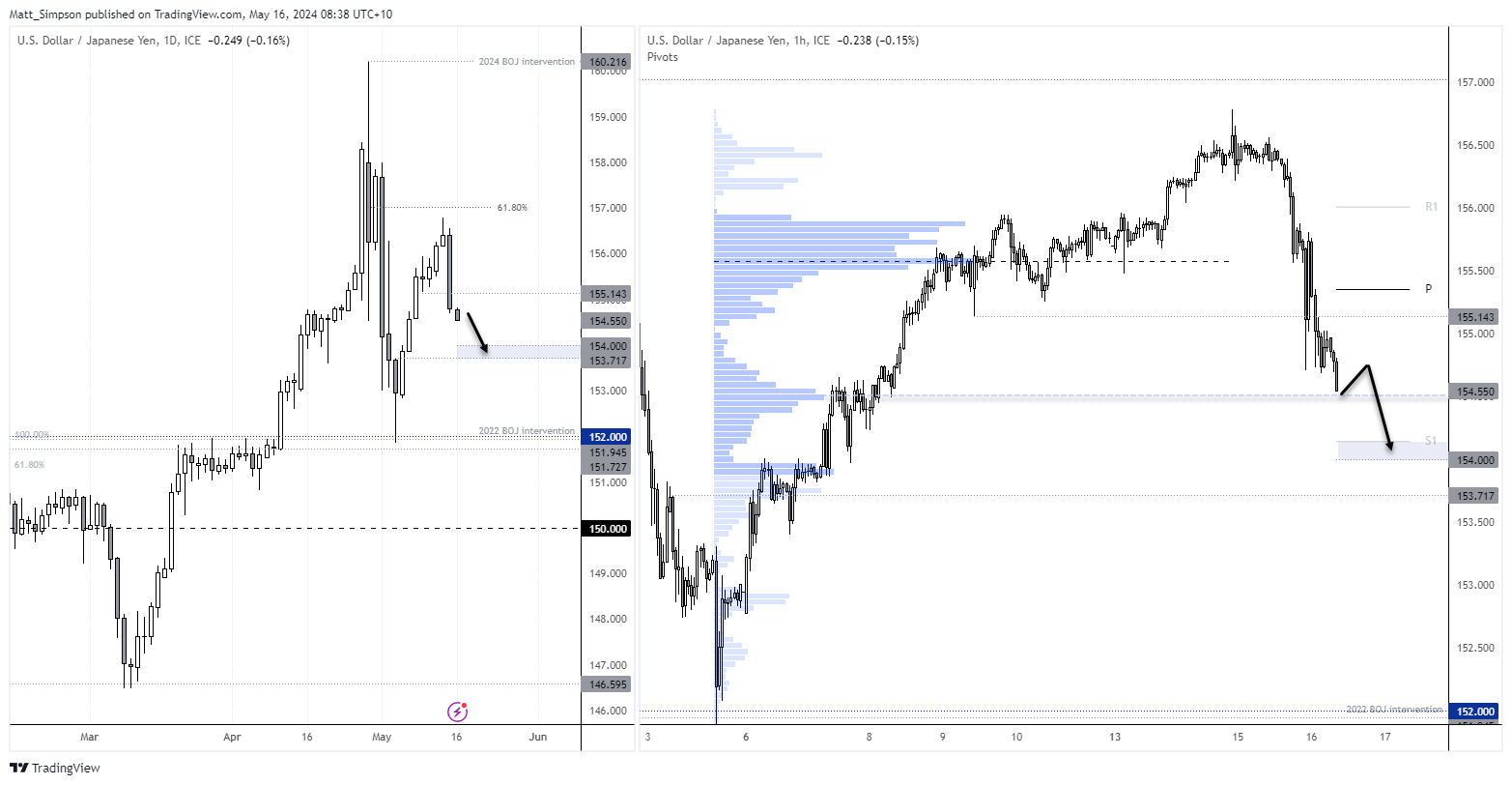

- USD/JPY fell just over 1% to mark its worst day since BOJ interventions, and further losses and move back to at least 152 seem likely with the US dollar bull-case quickly unravelling

- Bitcoin finally enjoyed the bullish range expansion we’ve been waiting for, rising above 66k for the first time in three weeks

Economic events (times in AEST)

- 09:50 – Japan GDP, foreigner stock/bond purchases

- 11:30 – Australia labour market report

- 14:30 – Japan capacity utilisation

- 20:00 – EU Economic Forecasts

- 22:30 – US building permits, housing starts, jobless claims, import/export prices, Philly Fed manufacturing

- 23:15 – US capacity utilisation, industrial production, manufacturing production

AUD/USD technical analysis:

The breakout of the Q3 and Q2 open prices were clean and done with conviction on AUD/USD. Prices stalled just beneath the 0.6700 handle and high-volume node from the January decline, so I suspect we may see some fickle price action around these levels early in today’s session. Note that support was found at the Q2 open on the 1-hour chart, which is also near the weekly R2 pivot – making 0.6685 a potential pivotal level for intraday traders.

But with traders on guard for even the slightest whiff of softer US data, AUD/USD could find itself extending its rally and heading for the daily R1 pivot or 0.6726 high should US data lean the ‘dovish’ way later today.

USD/JPY technical analysis:

After two (or maybe three) BOJ interventions, it seems market forces are now taking USD/JY the direction the central bank wants; lower. Wednesday’s bearish day saw prices cut through two handles and close below 155, and it now appears set to test 154 sooner than later. However, take note of a high-volume node around current levels which may provide interim support ahead of its next anticipated leg lower. The daily S1 pivot sits just above the 154 handle to make it a zone for bears to keep an eye on, a break beneath which brings 152 into focus.

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

Latest market news

Yesterday 10:18 PM

Yesterday 10:16 PM

Yesterday 09:00 PM

Yesterday 08:00 PM

Yesterday 07:39 PM

Yesterday 07:00 PM

Latest Asian Open articles

Yesterday 10:18 PM

December 9, 2024 09:50 PM

December 4, 2024 09:46 PM

December 3, 2024 10:21 PM