- JPY is behaving like a classic risk-on-risk-off currency again

- A huge week laden with major events awaits, headlined by rate decisions from the Fed and BOJ along with earnings from Apple, Microsoft, Meta and Amazon

- Selling USD/JPY rallies preferred… unless it’s from 152

Yen reverts to safe haven

The Japanese yen is behaving like a classic risk-on-risk-off currency again, often moving in line with other riskier asset classes. With interest rate decisions from the Bank of Japan (BOJ) and Federal Reserve (Fed), along with earnings from tech giants Apple, Microsoft, Meta and Amazon to navigate, it promises to be another volatile week for USD/JPY.

USD/JPY moving with riskier asset classes

Before studying event risk, it’s worthwhile looking at what’s been influencing USD/JPY over the past two weeks. The chart below does just that, looking at the rolling 10-day correlation with US-Japan two-year yield bond spreads in blue, the S&P 500 volatility index (VIX) in grey, S&P 500 futures in black, Nasdaq 100 futures in yellow and copper futures in green.

Source: TradingView

The relationship with four of the five variables has been extremely positive over the past fortnight with scores of 0.76 or higher. The only exception has been with the VIX at -0.82, indicating USD/JPY has often moved in the opposite direction to implied US stock market volatility.

Looking at the underlying message, the evidence is overwhelming that the Japanese yen is once again behaving like a safe haven asset, strengthening when risk appetite declines and weakening when risk rallies. That’s a departure from early 2024 when it was heavily influenced by rate differentials with the United States.

Should the risk-on-risk-off moves of last week continue – and there’s nothing to suggest they won’t – it means we can isolate what events are likely to shift risk appetite to evaluate directional risks for USD/JPY.

To say next week is important is an understatement. It is laden with multiple major risk events that would dominate an entire week if they were to occur in isolation. The next section focuses on the key ones you need to be aware of as traders, along with those that carry the potential to alter risk appetite.

‘Magnificent Seven’ earnings

It feels unusual to start the section off with second quarter earnings results from the US tech giants, but after the rout of the past two weeks across the sector, it looms as a make-or-break moment for the AI-led rally. If traders aren’t impressed by the results, the backlash will extend far beyond the US equity universe.

Microsoft kicks things off on Tuesday, with Meta on Wednesday followed by Apple and Amazon on Thursday. The focus will be on what they say in relation to tailwinds for revenue growth from AI, weighed up against the amount of capital investment. As the first cab off the rank, Microsoft will likely set the tone for the remainder of the sector.

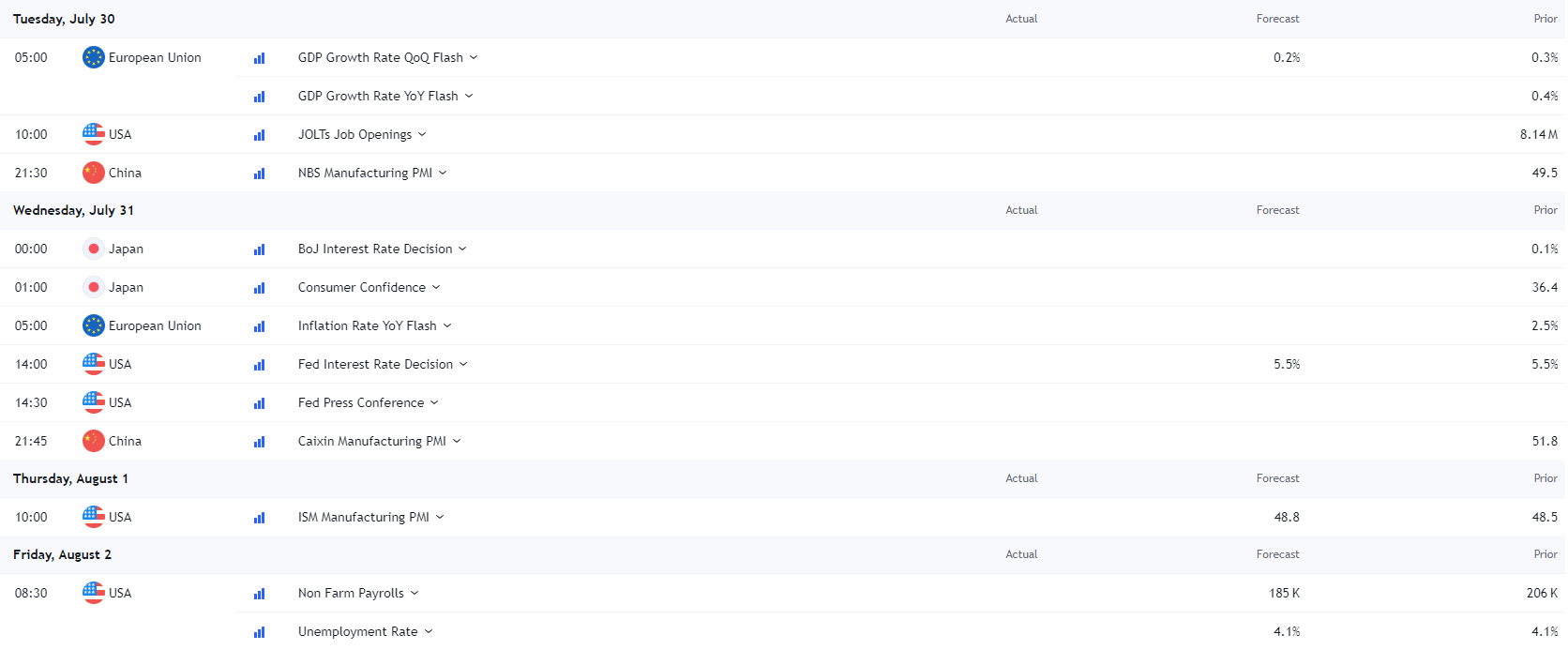

Fed, BOJ and major economic data

This calendar shows the key events traders need to know about. Along with those mentioned, the quarterly US Treasury refunding announcement on Monday and US Employment Cost Index (ECI) on Wednesday may generate volatility given the implications for US Treasury yields and policy outlook from the Fed. The Bank of England rate decision Thursday also warrants interest given the impact on FX markets.

US EDT times shown.

Source: TradingView

Looking at the data , the nonfarm payrolls report on Friday looms as the key risk event. The initial market reaction in USD/JPY will likely reflect the payrolls figure relative to forecast, although it’s worth reminding this is not the primary focus of the Fed. It’s more interested what’s happening with unemployment and average hourly earnings given the implications for inflation and economic growth. As such, be nimble if you’re trading off the payrolls figure solely, especially if we see another large downward revision that’s been seen frequently this year.

FOMC meeting

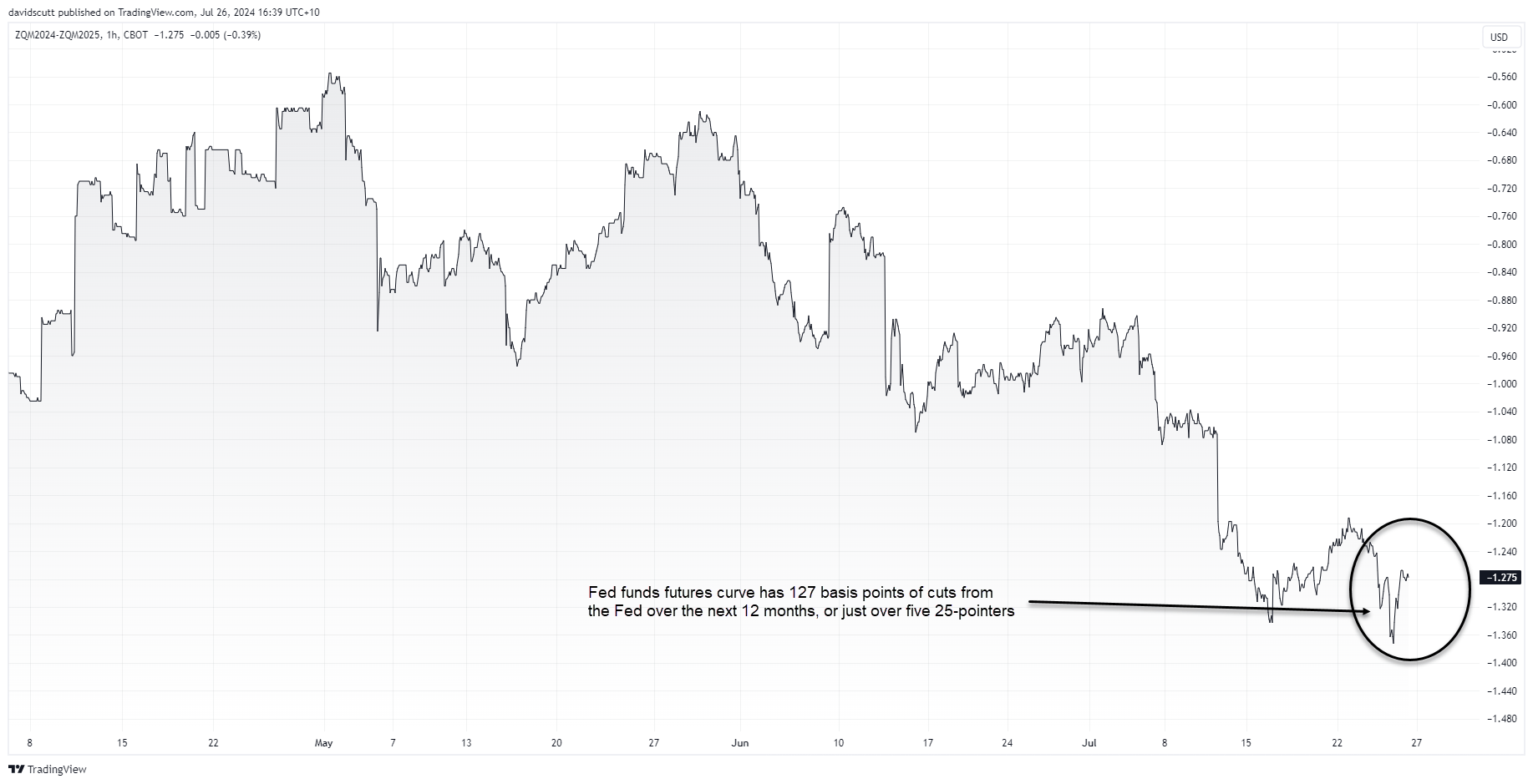

Unusually, the July FOMC meeting screens as one of the more predictable events next week with the Fed likely to signal explicitly that rate cuts are looming, most likely in September. Chair Jerome Powell will make the easing bias conditional on a continuation of progress in returning inflation to target, but the more important factor will be what clues he provides on the magnitude of cuts expected as we move into 2025.

Heading into the meeting, the Fed funds futures curve have just over five rate cuts priced over the next year.

Source: TradingView

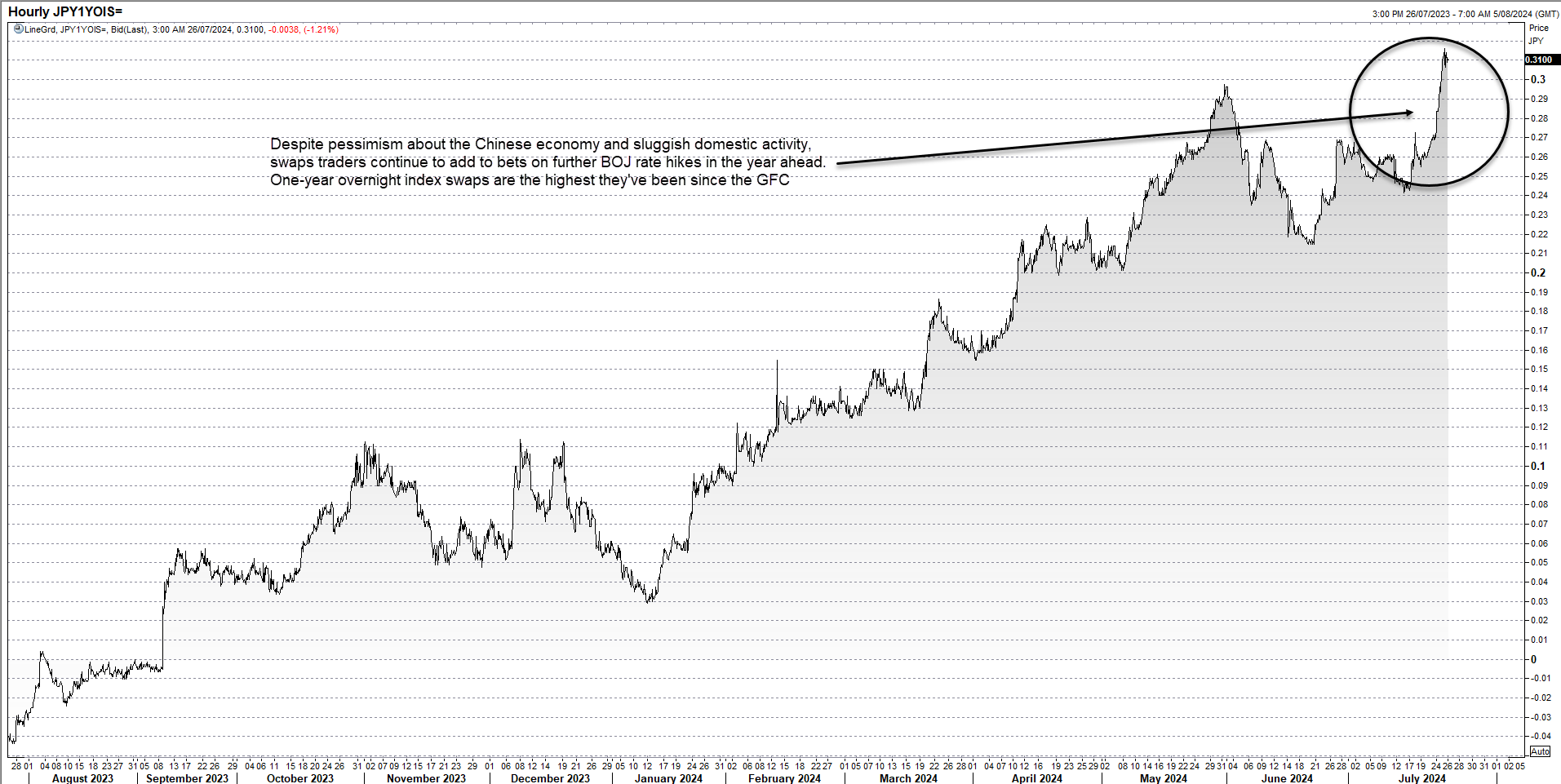

BOJ

In comparison to the Fed, the BOJ outcome is less certain with markets ascribing a 60% chance of the BOJ delivering another 10 basis point increase, adding to the one delivered in March. That would take the overnight rate to a range of 0.1-0.2%.

According to one-year overnight index swaps (OIS) which trade at 0.31%, it implies markets expect the BOJ to lift overnight interest rates to just over 0.5% over the next 12 months. OIS tracks the average overnight interest rate over the period specified.

Source: Refinitiv

It’s not just rates where this is a large degree of uncertainty with the outlook for the BOJ’s massive bond buying program also clouded. According to sources, the BOJ is likely to reduce bond purchases in several stages, most likely over the next 18 months to half the current pace. After muddling through the June meeting by failing to announce specifics, the BOJ will have to deliver something meaningful to prevent another ugly slide in the yen.

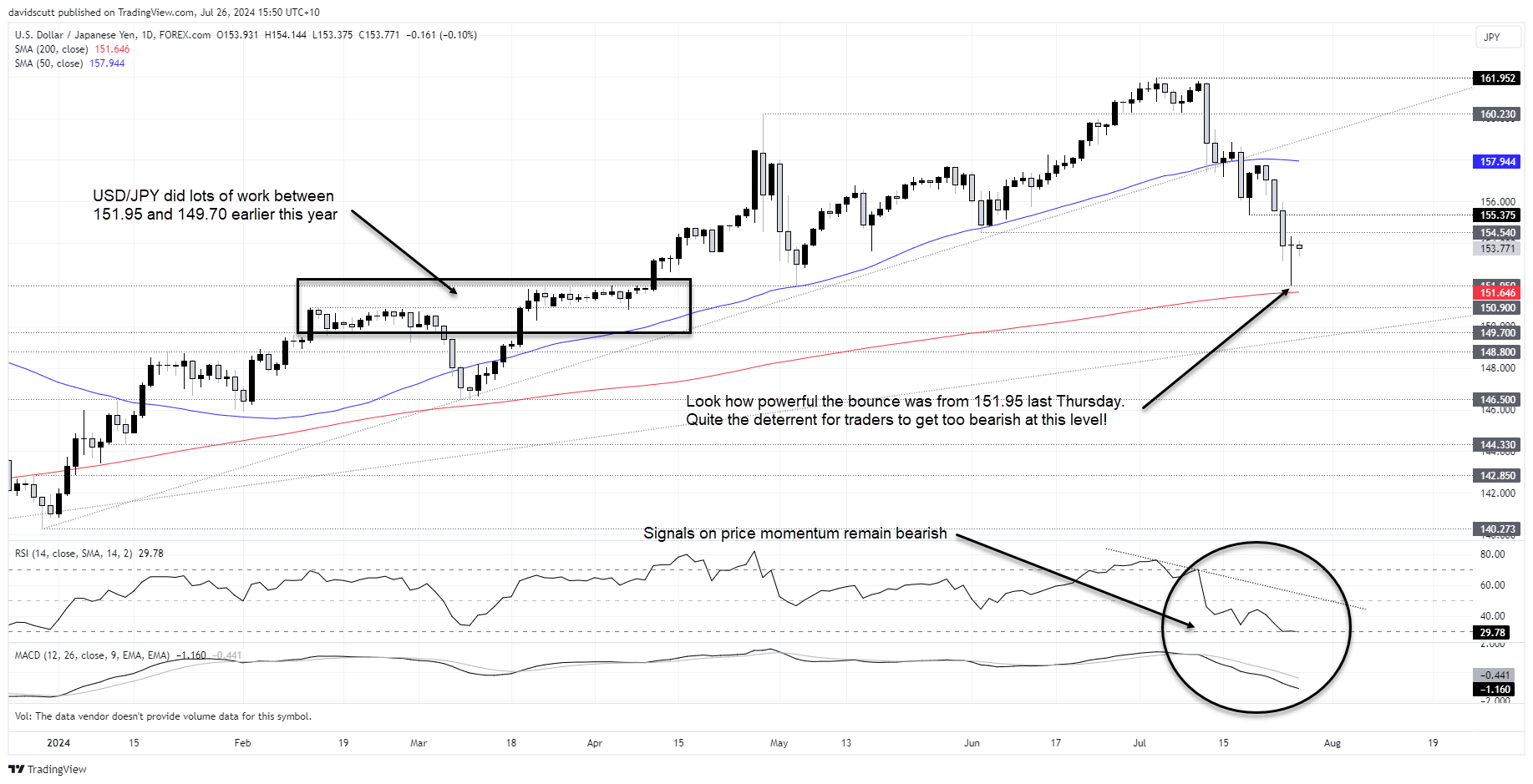

USD/JPY technical picture

The massive dragonfly doji candle off key support on Thursday has set the tone for the week ahead, reminding traders that while USD/JPY has broken down over the past couple of weeks, dip-buyers are not prepared to move aside just yet.

With RSI and MACD providing bearish signals on price momentum, selling rallies is preferred to buying dips… unless it’s from 152. That level could prove tough for bears to crack without a major risk off episode.

Source: TradingView

From its current level midway through the Asian session on Friday, minor resistance is found at 154.54 and 155.375 with far greater tests waiting at the 50-day moving average and former uptrend support above 157.94. On the downside, 151.95 is a hugely important level. With the 200-day moving average and major horizontal support located at 150.90 and 149.70, this zone looks ominous for bears near-term.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Yesterday 10:25 PM

Yesterday 09:46 PM

Yesterday 09:05 PM

Yesterday 08:20 PM

Yesterday 07:32 PM

Latest USD/JPY articles

Yesterday 08:20 PM

December 3, 2024 10:21 PM

December 3, 2024 06:28 PM

December 2, 2024 07:26 PM