- Gold analysis: Metal remains in holding pattern

- Dollar analysis: FOMC, BoE and NFP among next week’s highlights

- PCE inflation and consumer spending data keeping USD bears at bay

Welcome to another edition of Forex Friday, a weekly report in which we highlight selected currency themes. In this week's edition, we will discuss the US dollar and gold, and look forward to the week ahead.

Thanks to the positive risk tone across financial markets, the US dollar has struggled to hold onto its gains made in response to mostly positive data showing a resilient economy. Yet, it hasn’t sold off either, with many traders expecting the FOMC and its Chairman Jerome Powell to push back against early rate cut bets next week. For this exact reason, gold has been unable to find any lasting support, with traders happy to take quick profits in either direction, even if the long-term bullish trend remains intact. Today’s core PCE index was a touch weaker, but it was kind of expected after the GDP deflator came in softer the day before. However, consumer spending rose more than expected in December, and income was line. Adding to the fact we had a stronger GDP print the day before, plus several other positive macro releases lately, the dollar bears will find it difficult to justify pushing the greenback markedly lower from these levels until such a time we see significant data misses from, or big beats from outside of, the US. Let’s see if next week brings a real change.

Dollar analysis: PCE inflation and consumer spending data keeping USD bears at bay

Today’s key data release failed to offer any conclusive direction for the dollar. Following yesterday’s release of a weaker GDP deflator, it was always expected that the PCE data would also come in a bit weaker, and so it proved. However, if you exclude energy and housing from the PCE data, this measure of inflation was up 0.3% month-on-month, which is not something that would appease the doves in the FOMC camp. Correspondingly, the dollar rose a little off its earlier lows following the data release, helped along by the fact that we had stronger consumer spending data released at the same time.

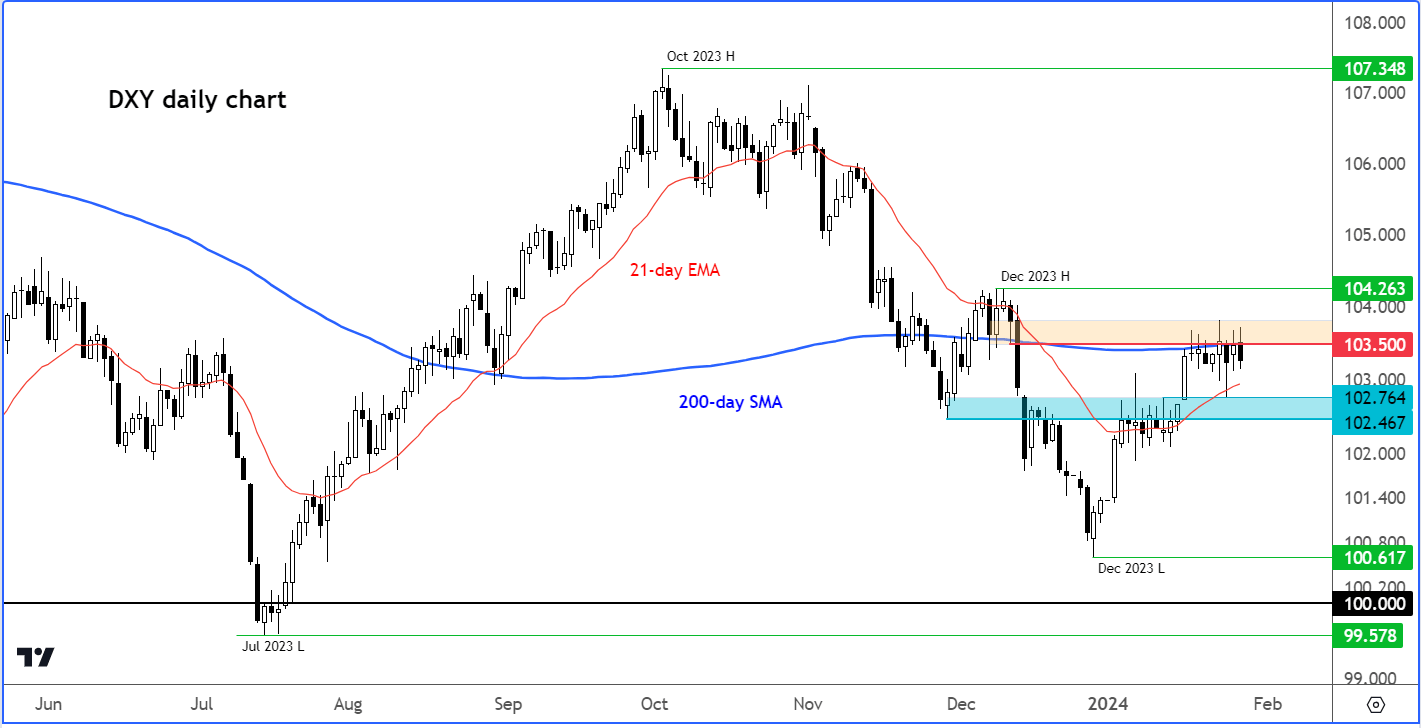

The Dollar Index (DXY) is therefore still stuck between a rock and a hard place, as per the highlighted support (blue shade) and resistance (orange shade) regions on the chart:

In case you missed it, the PCE core inflation data showed an annual rise of 2.9% in December compared to 3.0% expected and +3.2% in the prior month. The headline PCE Price Index was in line and unchanged from the previous month at +2.6% year-over-year. On a month-over-month basis, core PCE was in line at +0.2% compared to +0.1% last month.

There was more evidence of a strong consumer as spending rose more than expected in December. Personal spending was up 0.7% vs +0.4% expected, rising from the prior month’s upwardly revised +0.4% (from +0.2%). What’s more, real personal spending came in at +0.5% m/m vs 0.5% prior (revised from +0.3%). Consumer spending was in line at +0.3% as expected, following the previous month’s +0.4% print.

Gold analysis: Metal remains in holding pattern ahead of big events next week

With the US dollar unable to move freely in any particular direction this week, and bond yields largely holding onto their gains, gold has struggled to move away from its recent trading range. Investors are perhaps waiting for more clarity from the Fed itself next week, with nonfarm payrolls data also having the potential to move the markets sharply.

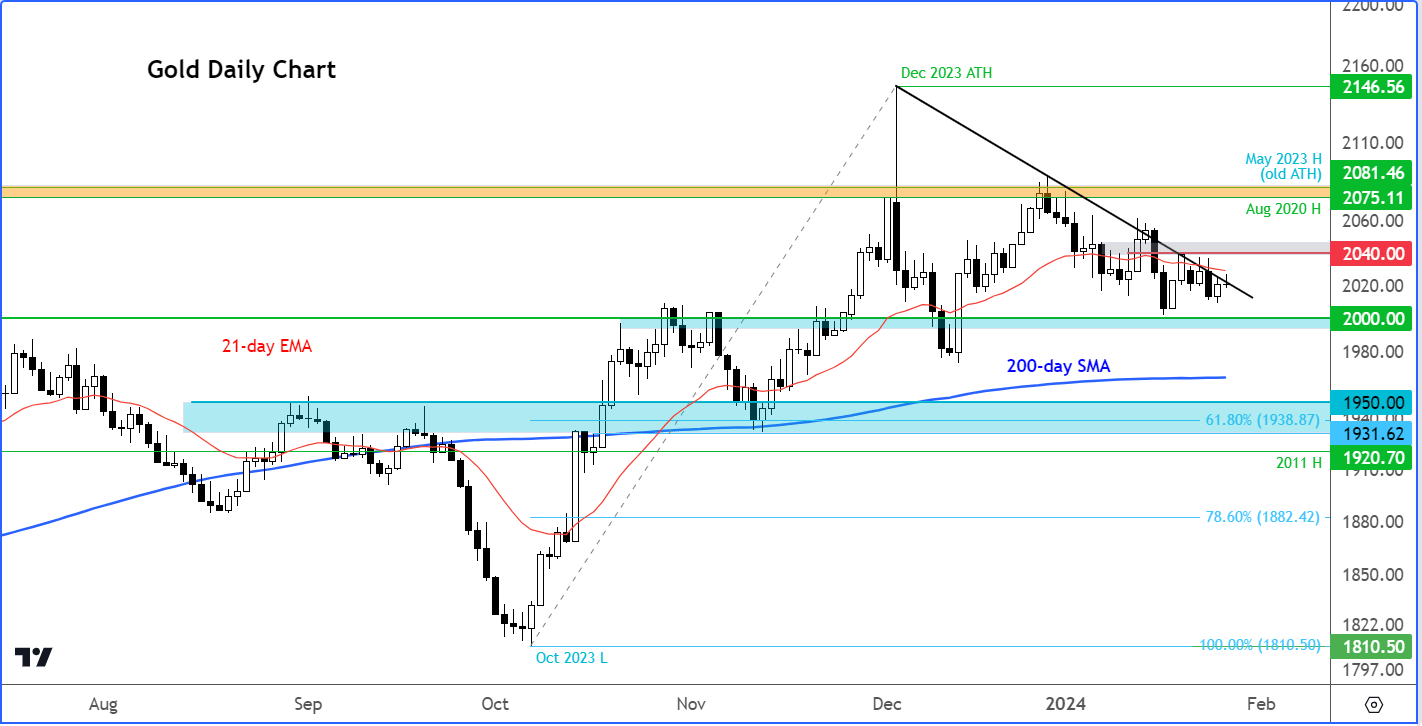

We will discuss those events, and more, in greater details, below. But from a technical point of view, gold remains inside a holding pattern for now, which means range-bound trading is likely to dominate rather than a sharp move in either direction. Support is seen in the area between $2000 to $2010. Resistance comes in around $2025, followed by $2040/5 area. A clean move above $2040 area is needed to re-establish the short-term bullish directional bias. The longer-term bullish view remains unchanged.

Dollar analysis: FOMC, BoE and NFP among next week’s highlights

The US dollar will remain in focus with some significant important macro events on tap for the week ahead.

FOMC rate decision

Wednesday, January 31

A slew of stronger US data in recent weeks has pushed the odds of a Mach rate cut to below 50% from above 90% at the end of December. This week saw consumer spending and GDP for the fourth quarter come in much better. GDP printed +3.3% on an annualised format, compared to 2.0% expected and 4.9% in Q3. Previously we had seen stronger-than-expected CPI, jobs and retail sales reports, keeping the dollar supported and gold undermined. There has been renewed concerns over the Fed’s inclination to maintain higher interest rates longer, after Fed governor Christopher Waller suggested a measured approach, cautioning against any haste in considering near-term rate cuts. Will Fed Chair Jerome Powell also push back against rate cuts bets more forcefully come Wednesday?

BoE rate decision

Thursday, February 1

Ahead of the Bank of England’s rate decision, we saw UK PMI data come in stronger than expected this week. But significant pressure on consumers remained with average earnings coming in weaker and CPI was hotter at 4% annual rate. The result of the squeeze on household incomes was evidenced by a 3.2% slump in monthly retail sales data. The BoE will not want to push too hard against rate cut bets as it could damage confidence and weigh further on the economy. Yet, with inflation remaining sticky, it won’t be able to cut rates as soon as the markets want. So, there’s a risk the BoE could keep rates high for longer, causing more damage to an already-struggling economy

US non-farm payrolls report

Friday, February 2

The dollar bulls would like to see continued strength in US data after the recent surprises that helped to push back rate cut expectations markedly. If we see further evidence of a resilient labour market, then this could keep the dollar supported against some of her weaker rivals. But if we start to see weakness creep into the jobs data then the market may once again start to believe in its earlier conviction that rate cuts may come sooner, after all. That said, it will take more than one jobs report to turn the tide again.

Source for all charts used in this article: TradingView.com

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 09:59 AM

Today 12:31 AM

Yesterday 10:31 PM

Latest Forex articles

Yesterday 07:31 PM

Yesterday 12:36 AM