Today, millions of UK citizens are heading to polling stations to vote in the general elections, while the US is out celebrating Independence Day. So, don’t expect any fireworks in the markets as we head deeper into today’s holiday-shortened session. As well as firmer FTSE, both GBP/USD and EUR/USD were higher in the first half of today’s session. The early hours of Friday when the election results come out, should be important for UK assets, before attention turns to the US economy and its jobs market with the release of non-farm payrolls data in the afternoon. Then it is all about the French legislative election on Sunday, which can arguably have a bigger influence on the FTSE 100 forecast than the UK vote today.

All eyes on UK elections – but don’t expect any fireworks in markets

The outcome of the UK elections looks to be a foregone conclusion with the Labour set to sweep to victory and the Conservatives getting annihilated, if recent polls are anything to go by.

Evaluating the Labour Party manifesto, we do not foresee substantial alterations to the UK’s fiscal position. Labour intends to boost spending by about £9 billion, financed by tax hikes. However, this is relatively modest given the scale of a £3 trillion economy.

If Labour emerges victorious, it must maintain investor confidence while tackling the UK's persistent economic issues, such as the public debt-to-GDP ratio being at a 63-year high. Significant economic improvement appears unlikely. To avoid spending cuts, Labour will need to either raise taxes or increase borrowing, presenting a lose-lose situation that the markets seem to have accepted.

Given that a Labour win is anticipated, the pound and FTSE could react sharply to an unexpected result, such as a hung parliament. Exit polls will begin around 10 pm, providing an early indication of party performance, with actual results expected in the early hours of Friday.

French legislative election poses greater risk to FTSE 100 forecast than UK vote

In Europe, attention is shifting to the second round of the French elections. A concerted effort by parties determined to keep Marine Le Pen’s far-right National Rally from gaining power has gained momentum ahead of Sunday's legislative election, with key political figures warning that voter decisions will have significant implications for France and the Eurozone. The recent rebound in the euro and stock markets suggests that investors are confident the National Rally will be kept out of power.

Indeed, the most probable outcome is a hung parliament, which could lead to difficulties for the new assembly in reaching a consensus on spending cuts, the primary concern for investors. Nonetheless, the possibility of Le Pen’s National Rally party governing France remains a significant risk. "If we're just a few members of parliament away from a majority, we'll try to go find them," Le Pen stated on Tuesday.

What other factors are driving the markets right now?

The primary reason why risk assets have rallied this week is perhaps because investors are growing confident that the US monetary policy will be loosened in September. A series of disappointing macroeconomic indicators from the world’s largest economy have increased expectations that the Fed will cut rates, but will Friday's release of US nonfarm jobs report throw a spanner in the works?

After showing surprising resilience throughout this year so far, we could begin to see more weakness in the US labour market moving forward. Indeed, economists expect the US jobs report to show only a modest 190,000 rise in non-farm payrolls compared to 272,000 the month before.

After last Friday’s core PCE price index, which was bang in line with expectations, we have seen rather weak data this week, in particular the services PMI as reported by the ISM on Wednesday, which caused the dollar to slump. If the jobs report also disappoints then this should further boost expectations over a rate cut in September, and thereby provide further support for US markets, which in turn could help to support other global indices like the FTSE.

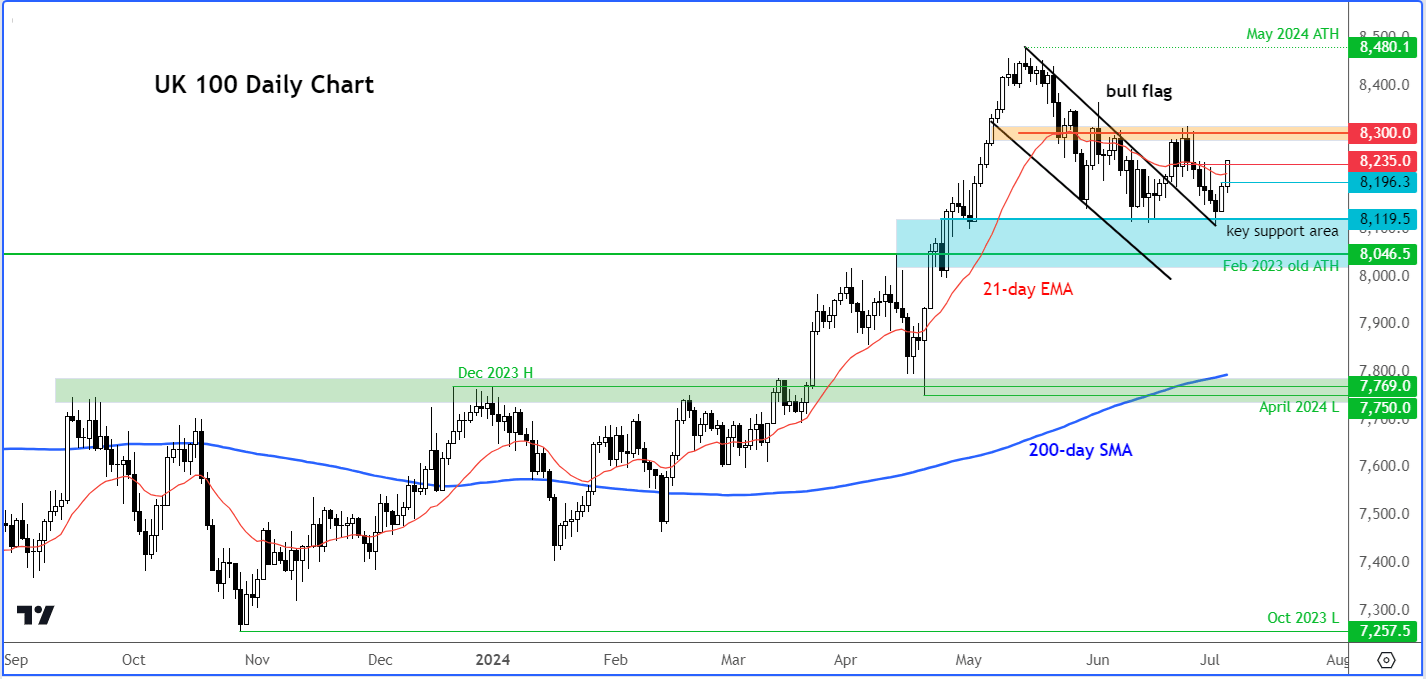

FTSE 100 forecast: technical analysis

Source: TradingView.com

The FTSE has held its own above key support and old all-time high in the range between 8046 (Feb 2023 high) and 8120 (horizontal support) after it recently broke out of its bull flag. While that bull flag breakout didn’t lead to any immediate follow-through gains, the fact that support has held is nonetheless a positive sign, keeping the technical FTSE 100 forecast bullish.

At the time of writing, the FTSE was trying to break the next resistance at around 8235/8245 area and sitting its sight on the bigger resistance circa 8300. Above 8300, the next objective is the all-time high that was formed in May at 8480.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 12:30 PM

Today 09:44 AM

Today 09:34 AM

Latest Election articles

Yesterday 04:20 PM

November 12, 2024 05:52 PM

November 6, 2024 09:52 PM

November 6, 2024 05:48 PM