The better-than-expected performance from US Q3 banks’ earnings often paves the way for some encouraging numbers from UK banks. While NatWest, Lloyds, and HSBC are expected to post a year-on-year rise in pretax profit, Barclays is forecast to post a decline.

When?

Barclays – Tuesday, October 24th

Lloyds – Wednesday, October 25th

NatWest- Friday, October 27th

HSBC – Monday, October 30th

Overview

High-interest rates have been a double-edged sword for the banks. On the one hand, higher rates have boosted Net Interest Margin NIM, the difference between interest received on loans and interest paid out on deposits. However, on the other hand, rising impairment provisions could outweigh those NIM improvements.

With the BoE potentially at the end of its rate hiking cycle, the outlook for NIM will be in focus, particularly considering that full-year NIM guidance was set at a higher rate of 5.5%, so a downward revision could be on the cards. Any comments on this topic will be scrutinized closely.

Loan demand will also be under the spotlight as higher borrowing costs stifle demand, as noted through recent weakness in mortgage approvals.

Customer deposits will be another area to watch as customers react to higher interest rates by paying down debt or moving to higher-yielding assets.

Barclays is set to underperform its sector peers, with investment banking in focus and a deeper downturn in FICC (fixed income, currency, and commodities) trading. Pretax profit is forecast to decline by 3.9%.

Meanwhile, HSBC is likely to outperform, underpinned by rising rates worldwide, with Q3 pre-tax profits expected to rise an impressive 168%.

Barclays

When: October 24th, before the opening bell

What to watch:

Barclays will report as the share price trades 9% lower year to date. The bank is set to underperform its sector peers with pretax profit expected to fall 3.9% year on year in Q3 to £1.89 billion. Total group revenue is expected to rise 7% to £6.3 billion.

The annual net interest margin was cut to 3.15% from 3.2% in Q2 and is at risk of being revised downward. Total deposits are set to fall 6% as customers react to higher interest rates by paying down debt or moving to higher-yielding assets. Total loans are expected to fall by 3% owing to high borrowing costs. Meanwhile, bad loan provisions were £372 million in the previous quarter, taking impairment charges to H1 to £896 million; this is expected to rise further. Significantly higher bad loan provisions could hit the bottom line. Cost containment will be a key to off-setting sluggish revenue.

The performance of the investment banking division will be watched closely, especially in light of the mixed performance of investment banking divisions on Wall Street. Equity trading could be a strength, but a deeper downturn in FICC (fixed income, currency, and commodities) trading could also be on the cards.

Lloyds

When: October 25th, before the market opens

What to watch:

Lloyds will report Q3 results as the share price trades down at around a 9-month low on concerns over the outlook for the UK economy.

Expectations are for Lloyds to post a pretax profit of £1.76 billion, up 16.8% from the same period last year, on revenue of £4.7 billion, up 0.5% annually. NatWest is expected to see NIM hold steady at 3.15%, in line with full-year guidance. With the BoE at or near peak interest rates at 5.25%, any margin outlook comments will be scrutinized closely and could impact sentiment. The bank missed profit forecasts after setting aside £419 million to cover potential bad loans, investors will be watching to see what the bank sets aside. Loan demand will also be a key focus, given that Lloyds is a big mortgage lender. Loan demand fell in the previous quarter, as did customer deposits. Easing inflation is a positive for the bank’s cost base, and the £9.1 billion cost base target looks attainable.

NatWest

When: October 27th, before the market opens

What to watch:

NatWest trades down 16% year to date in a reaction to CEO Alison Rose’s resignation after she admitted to leaking information to the BBC about the bank’s relationship with Nigel Farage. The new CEO

NatWest outperformed in Q2 results as the lender is the biggest beneficiary of interest rate rises. NatWest is expected to see NIM remain in line with full-year guidance of 3.15%. However, with the BoE near or even at the end of its rate hiking cycle, investors will be keen to see the outlook for net interest income in the coming quarter and heading into 2024. The full-year figure could be downwardly revised further as it was based on the BoE hiking rates to 5.5%.

Pretax profit is expected to rise 25.6% to £1.36 billion, up from £1.08 billion in Q3 2022, and revenue is expected to rise £3.6 billion. Total deposits are set to fall 9.2% compared to the previous year, and loan demand could also fall for the first time this year, given weakness in the housing market and mortgage approvals. After setting aside £153 million in non-performing loans in Q2 and £70 million in Q1, the market will be watching to see if this trend continues. As with Lloyds, costs will be in focus as easing inflation provides relief. Total expenses of £7.7 billion this year look within reach.

HSBC

When: October 30, before the market opens

What to watch:

After impressive H1 results, HSBC is set to report a pre-tax profit of £8.44 billion, up from £3.15 billion in 2022 but down sequentially from $8.8 billion. Revenue is expected to rise by 28% to £16.95 billion. The bank has benefited from a strong rise in revenue as it benefits from higher interest income across its global business, so much so that it announced a $2 billion share buyback in the previous quarter. HSBC saw a particularly strong performance in its commercial banking and wealth and personal banking segments. Investment banking revenue will be under the spotlight, with growth expected to slow, while wealth and personal banking revenue growth could increase.

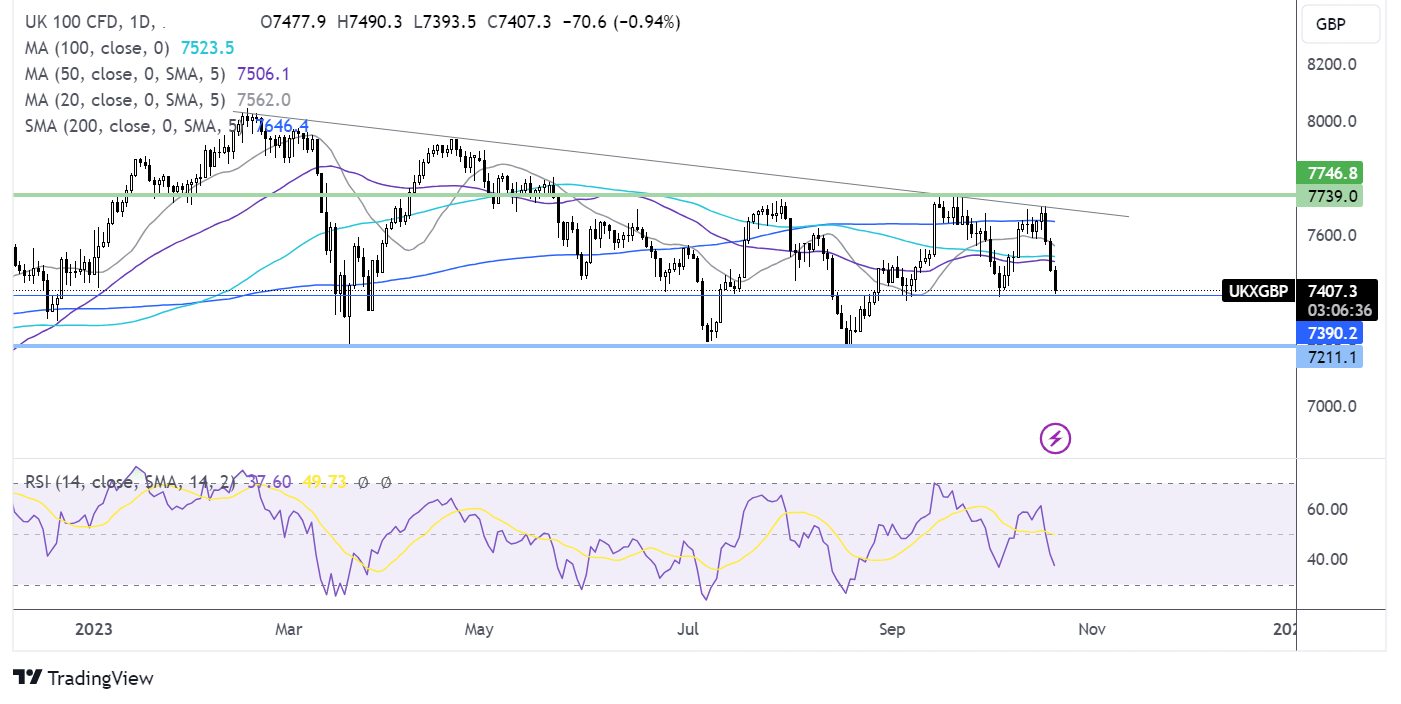

FTSE forecast – technical analysis

After running into resistance at the multi-month falling trendline, the price rebounded lower, falling below the 200, 100, 50 & 20 smas. This, combined with the RSI below 50 keeps sellers hopeful of further downside. Immediate support can be seen at 7380/7400 region, the October low. A break below here opens the door to 7200 the August low. Should the 7380/740 support hold, buyers could look to extend the recovery towards the 50 and 100.

Latest market news

Today 05:30 PM

Today 04:41 PM

Today 04:30 PM

Today 02:15 PM

Today 02:07 PM