Asian Indices:

- Australia's ASX 200 index fell by -20.7 points (-0.28%) and currently trades at 7,337.10

- Japan's Nikkei 225 index has risen by 27.79 points (0.08%) and currently trades at 33,416.70

- Hong Kong's Hang Seng index has fallen by -384.03 points (-1.96%) and currently trades at 19,223.05

- China's A50 Index has fallen by -27.85 points (-0.22%) and currently trades at 12,746.48

UK and Europe:

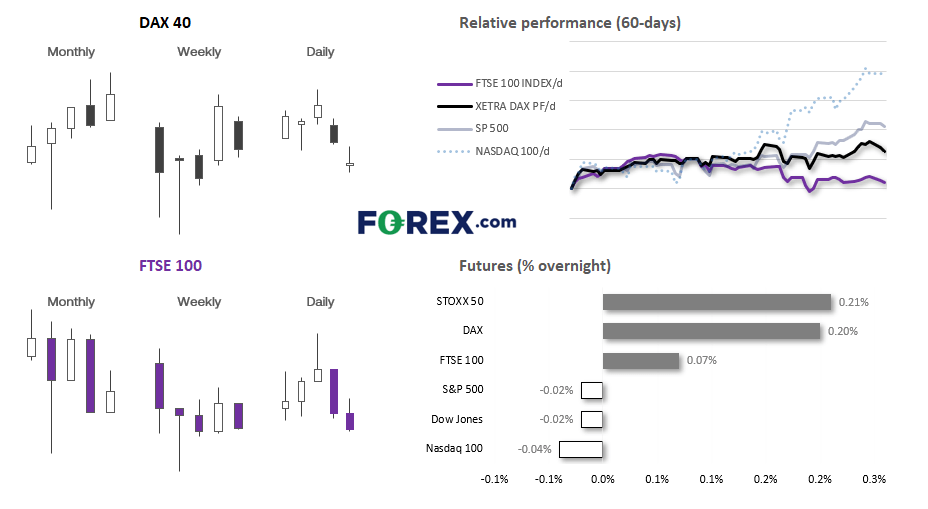

- UK's FTSE 100 futures are currently up 5 points (0.07%), the cash market is currently estimated to open at 7,574.31

- Euro STOXX 50 futures are currently up 9 points (0.21%), the cash market is currently estimated to open at 4,352.14

- Germany's DAX futures are currently up 32 points (0.2%), the cash market is currently estimated to open at 16,143.32

US Futures:

- DJI futures are currently down -8 points (-0.02%)

- S&P 500 futures are currently down -1 points (-0.02%)

- Nasdaq 100 futures are currently down -5.75 points (-0.04%)

- Volatility has been typically quiet ahead of a key Jerome Powell speech who is due to testify to the House today and Senate tomorrow

- There was no surprises within the BOJ minutes which showed members continued to favour ultra-loose policies (so any cancellation of YC remains very much on the backburner)

- This could allow USD/JPY to break top new cycle highs if Powell delivers hawkish comments

- President Biden has suggested that President Xi desires a resumption of relations with the US, although also labelled him a dictator

- US futures markets are holding steady in tight ranges after Wall Street retraced lower for a second day, presumably as investors lightened up their loads after a solid run, ahead of Powell’s speech

- And that mean equity traders on the side line may be looking out for any dovish clues (however small) to rejoin that trend, in hopes of a lower terminal rate (and not the 50bp of hikes the dot plot suggested

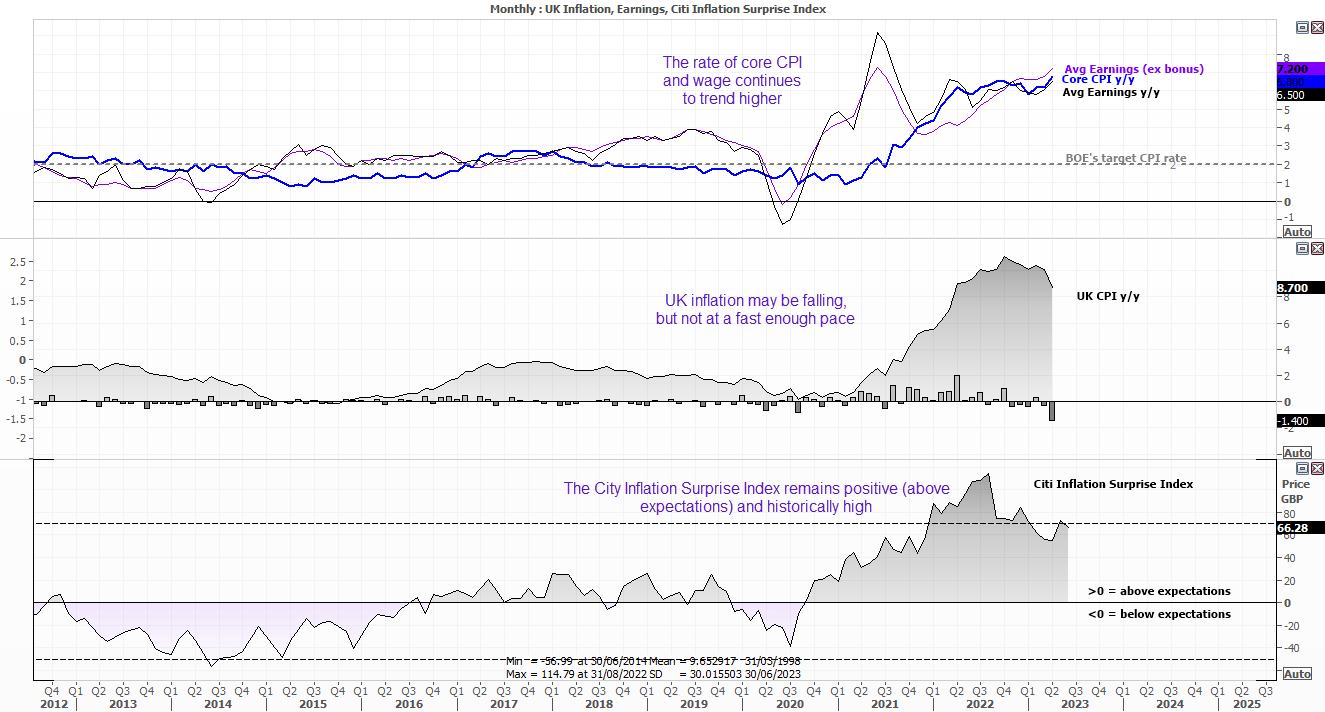

UK inflation in focus at 07:00 BST

The UK inflation report will be a key focus from 07:00 BST, as it could directly impact market pricing for the BOE (Bank of England) on the eve of their next monetary policy meeting. A 25bp hike tomorrow is effectively a given, so today’s inflation data is really about how many more hikes are to be expected, and for how long(er) they will remain high.

The BOE’s base rate currently sits at 4.5% whilst the 1-year OIS (overnight index swap) sits at 5.64%, which means money markets have fully priced in another 100bp of hikes with the potential for a fifth. With wages rising and employment tight as ever, the risks to inflation remain to the upside – even if input costs have been falling. And a hot inflation report today could simply increase expectations of higher-for-long rates, support GBP and weigh further on the FTSE 100.

Jerome Powell is set to testify to congress

The Fed have just paused interest rates, and now Fed Chair Jerome Powell will have to field questions from congress on that decision. Today he will speak to the House Financial Services Committee, then tomorrow the Senate Banking Committee. As the second performance is usually a repeat of this first, today’s show is the main event. His introductory remarks are usually released which means traders an algos and quickly scan the comments and potentially move markets, before he will then lock horns with congress. Inflation remains too high and we see that housing data is making a strong comeback – which is itself inflationary. And that means there is a chance we could have a hawkish tone overall and see the US dollar bid. Of course, if he surprises with dovish remarks, this could weigh on the US dollar and send GBP/USD notably higher should UK inflation surprise to the upside.

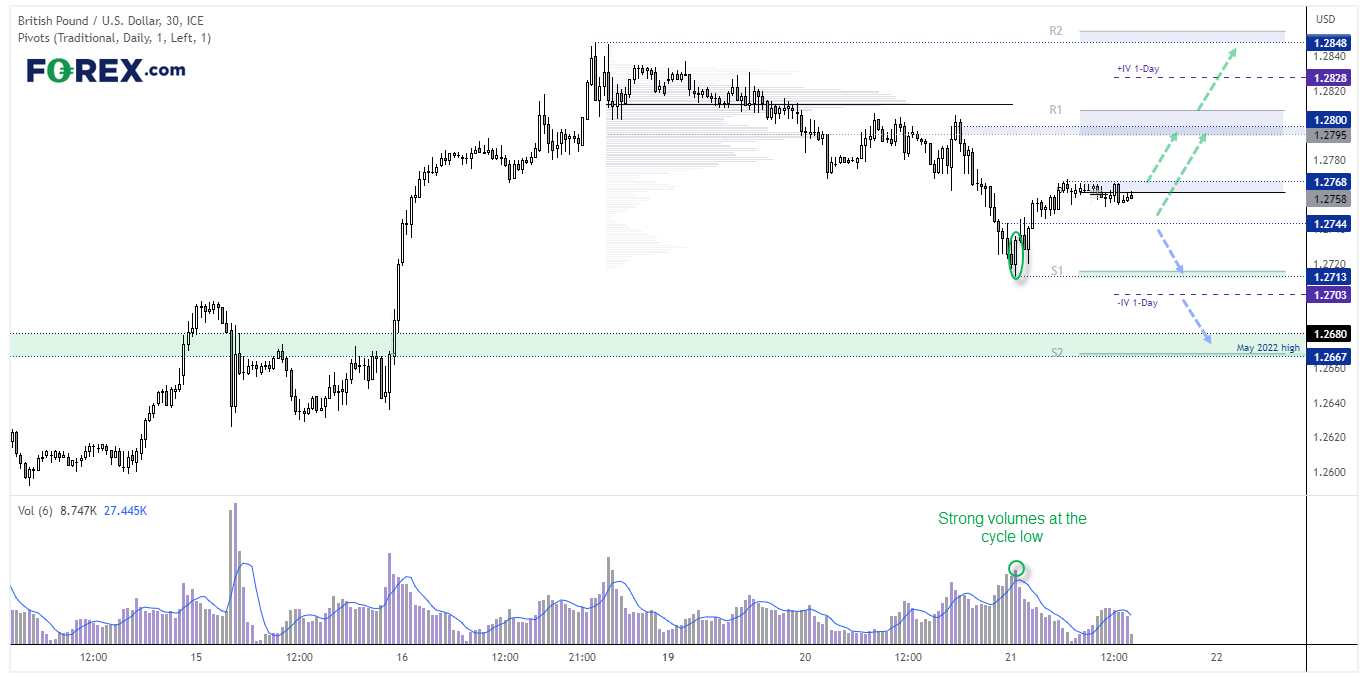

GBP/USD spot

We saw strong buying volumes at the 1.2713 low yesterday, before prices recouped around half of the day’s losses heading into the NY close. Intraday support sits around 1.274 and 1.2756, and momentum is trying to turn higher after a tight consolidation around 1.2760 early Asia. Overnight Implied volatility suggests a move of around 66pips, which could see GBP/USD reclaim the 1.2800 and break above Friday’s high ahead of Jerome Powell’s meeting, assuming we’re not presented with a surprisingly soft inflation report.

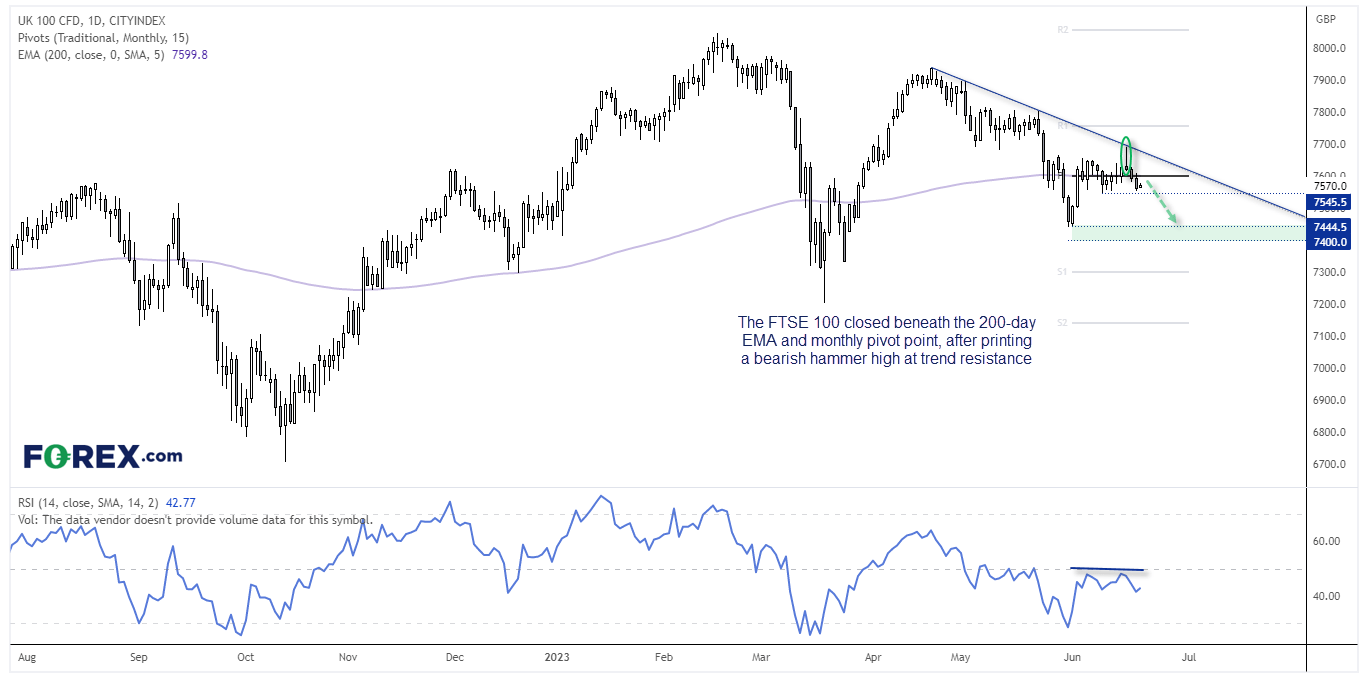

FTSE 100 daily chart:

The FTSE 100 closed at a 5-day low yesterday, which was its second close beneath its 200-day EMA and monthly pivot point. The index also printed a prominent bearish hammer on Friday, which met resistance at the bearish trendline to suggest the swing high is in place. The RSI (14) remains below 50 and is now moving lower with prices. We’re now looking for a break of the 7454.5 low, and move towards the 7400 – 7445 zone.

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

Latest market news

Yesterday 07:55 PM

Yesterday 05:50 PM

Yesterday 05:30 PM

Yesterday 05:06 PM

Latest Trade Ideas articles

Yesterday 07:55 PM

Yesterday 05:50 PM

Yesterday 05:30 PM

Yesterday 05:06 PM