EUR/USD in the hands of ECB, Powell Testimony, ISM services: The Week Ahead

EUR/USD is on track for its smallest weekly range since September 2021, although 1-week implied volatility levels that we could see more action next week. And that may well be the case, given we have Jerome Powell testifying on the same day as the ISM services PMI report is released, before an ECB and BOC later in the week. Also keep an eye on data from Japan in light of hawkish comments from a BOJ official, as bets may now be on of a hike in March of April.

The week that was:

- US PCE inflation data came in as expected across the board, leaving little in the way of a surprise – even if core PCE rose 0.4% m/m

- Wall Street indices turned higher and closed less than a day’s trade away from record highs by Thursday’s close, whist the Nikkei 225 and ASX 200 reached all-time highs during Friday’s session

- Fed member Collins and Williams said that Fed cuts would be appropriate “later this year whilst Bostic has one pencilled in “by summer”

- Japan’s core CPI reached the BOJ’ 2% target, although as the consensus was for it to soften to 1.8% it sent the yen higher

- BOJ member Tanaka said that the BOJ were on track to achieve their 2% inflation goal and that it could be time for the central bank to discuss how to move away from their ultra-loose policy, sending the Japanese yen broadly higher on Thursday

- Soft retail sales in Australia provided further reason to ignore the RBA’s hawkish bias in their latest statement

The week ahead (calendar):

The week ahead (key events and themes):

- US Primary elections

- ISM services PMI

- Nonfarm payroll

- ECB, BOC monetary policy meetings

- Japan’s data

- Tokyo CPI

- UK Spring budget

US Primaries (Super Tuesday)

The US primary elections will continue next week, where 16 States vote for their presidential candidates on a day known as “Super Tuesday”. It is almost a given that Biden and Trump will be the nominees for the Democratic and Republican parties, respectively. Something to watch is whether the Uncommitted campaign convinces enough people to halt support for Biden due to his stance on Gaza, and what proportion if the vote Nikki Haley can maintain in the “closed” primaries next week. Whilst these are not likely to be large market-moving events, it could provide a glimpse of what is to come as the Presidential campaigns kick off later this year.

Trader’s watchlist: S&P 500, Nasdaq 100, Dow Jones

ISM services PMI

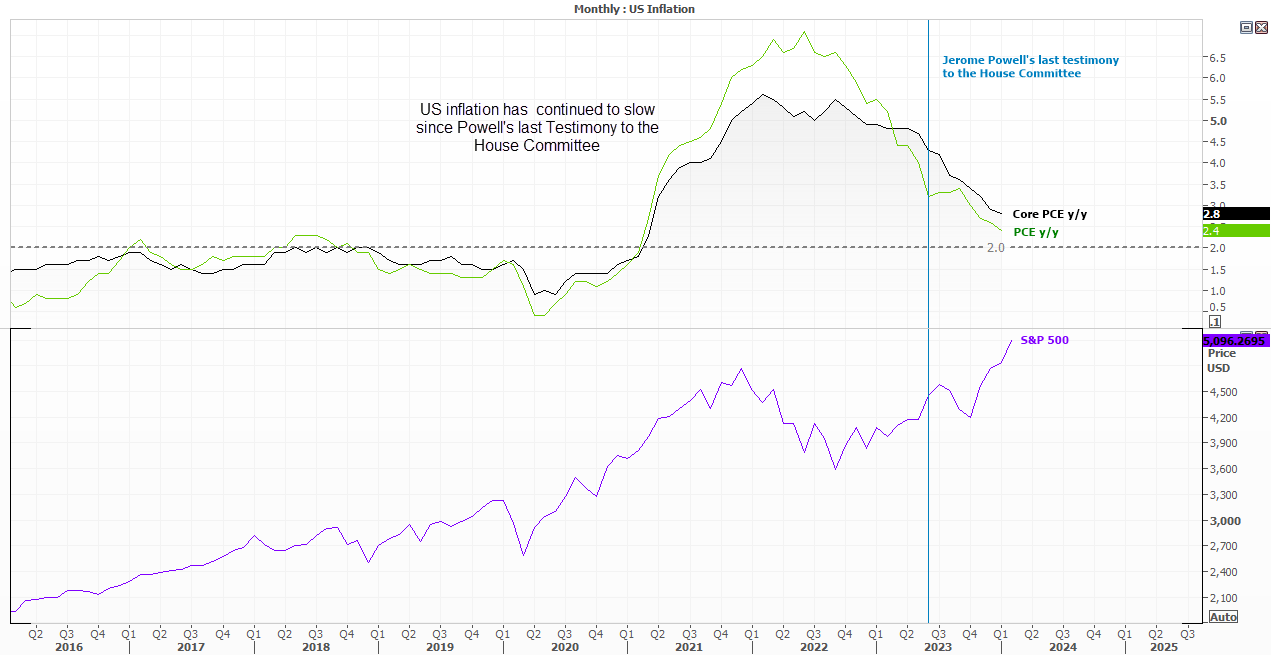

ISM services PMI will provide a gauge on growth prospects for the US, alongside inflationary pressures via the ‘prices paid’ sub index. Given Fed members continue to push back on imminent rate cuts, employment remains firm and inflation relatively elevated (even is softer), the data sets such as the ISM can fine-tune expectations of Fed policy. It is therefore worth noting that the headline index expanded at its fastest pace in five months, employment and new orders also expanded, and prices paid rose shot up to a 12-month high at its fastest monthly pace in nearly three years. If a similar pattern emerges, it points to higher inflationary and growth forces and likely lowers expectations of a June Fed cut.

Trader’s watchlist: S&P 500, Nasdaq 100, Dow Jones, gold, WTI, USD/JPY

Jerome Powell to testify before the House Committee

Next week the Fed Chair has his bi-annual testimony to the House Committee, which is an ideal opportunity for him to (re)shape policy expectations. What traders clearly want to hear is a dovish pivot, but I’m not convinced we’ll get it next week. But it likely means volatility will be hampered in the lead up to his appearance.

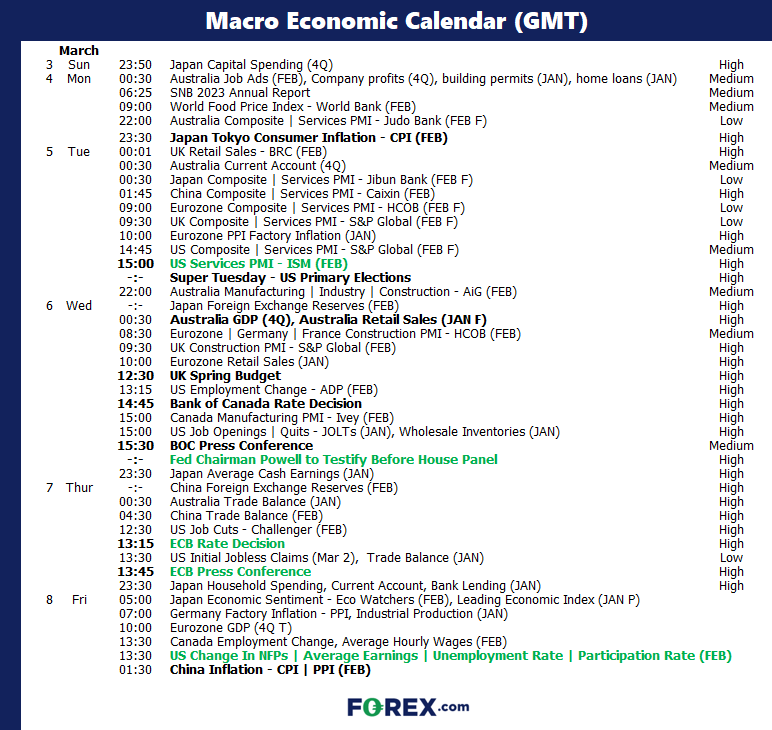

Powell told the committee last June that he was hawkish on inflation, and walked back any concerns of mass job losses. Since then, PCE inflation has slowed from 3.2% Y/Y to 2.4% and core PCE has slowed from 4.3% y/y to 2.8%, whilst employment reports continue to knock out some decent numbers, all thing considered. And it is really that latter point as to why I still do not expect to hear any sort of dovish pivot from Powell next week, but he should at least tip his hat on the progress to inflation.

My bet is he may further convince markets that a cut around June seems likely, which is what market pricing and economists generally agree on. And that could make his testimony one of the less interesting ones.

Of course, if he surprises with a dovish twist an implies an earlier hike, expect markets to jump onto the ‘short USD’ theme and send risk (and therefore Wall Street indices) to new highs.

Trader’s watchlist: S&P 500, Nasdaq 100, Dow Jones, gold, WTI, AUD/USD, AUD/JPY, EUR/USD, USD/JPY

BOC interest rate decision:

Softer inflation figures leave the potential for a dovish tile to the BOC’s statement next week, although a cut can effectively be ruled out given market expectations of a Fed cut as late as June. Their January statement tipped their hat to softer consumer spending and contracting business investment yet higher wages. And with growth expected to pick up in H2, a hold seems appropriate and for no dovish pivot to be revealed.

Trader’s watchlist: USD/CAD, CAD/JPY, NZD/CAD,

ECB interest rate decision and press conference:

Again, no change is expected from the ECB given the debate has really been about which side of summer their easing will take place. Ther was a lot of noise among ECB members at the start of the year which may have muddied the ECB’s core message which may need to be fixed at the press conference by Christine Lagarde. And whilst German inflation figures are softening faster than expected, that is not the case across Europe as a whole which means inflationary pressures persist, which is why I doubt the ECB will signal a dovish pivot over the next couple of meetings.

Trader’s watchlist: EUR/USD, EUR/JPY, EUR/GBP, DAX

Nonfarm payroll

Of course, NFP mush at least have a mention. But there's little to add that I haven't said previously; job growth remains strong, unemployment remains low by historical standards and this combination is a key reason as to why the Fed are in no rush whatsoever to announce cuts. As usual, keep an eye on prior employment reports next week such as Challenger job cuts, initial claims and ADP as it can change sentiment towards Friday's NFP report. But given the US added over 350k jobs last month, it could take an abnormally large miss for NFP to justify a cut at this stage.

EUR/USD weekly chart:

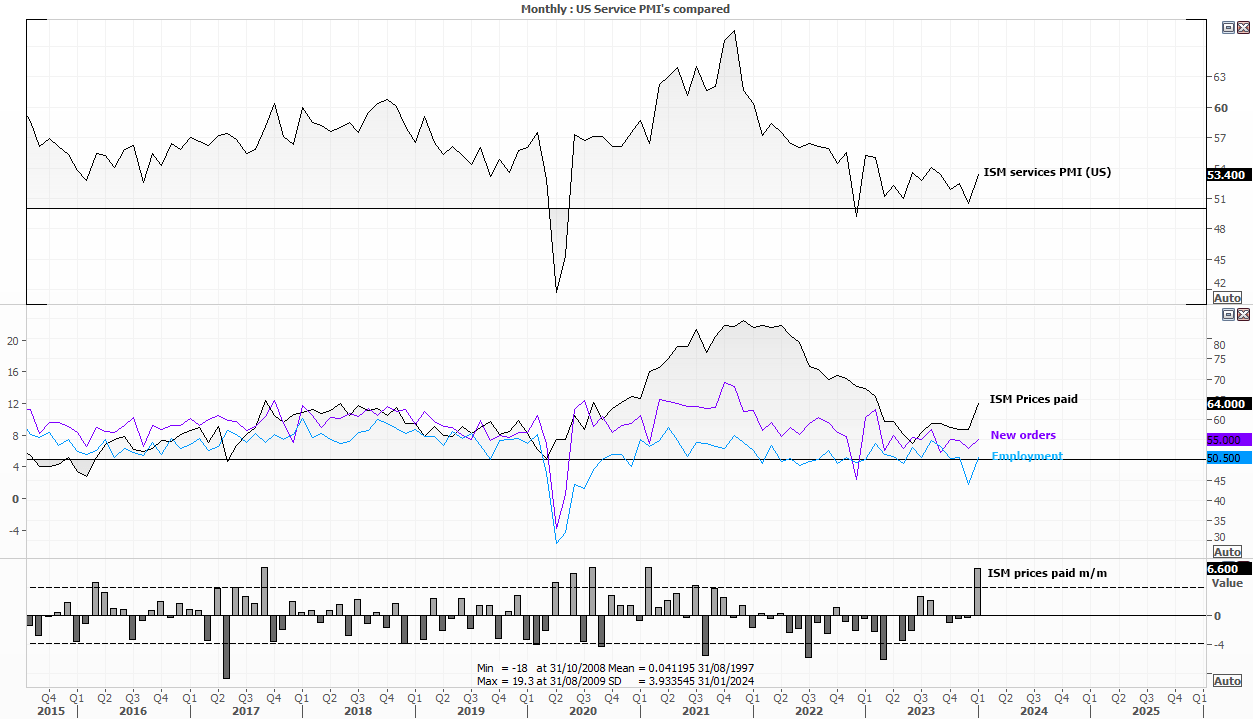

The two weekly bullish pinbars – the second if which saw a false break of the December low – did indeed mark the inflection point for EUR/USD. Yet the subsequent bullish week gave over half of its gains back by the end the week, and EUR/USD is currently on track to form a small indecision week and close between the 20 and 50-week EMAs. So not only has volatility dropped this week, but its direction has also been sorely lacking.

Therefore, we need to rely on an exciting Jerome Powell testimony or ECB meeting to break the deadlock. The 1-week implied volatility band suggests volatility is to increase next week, with a 68% chance of its range landing between the December low of 1.09 handle. And as we need to wait until Tuesday (US) for ISM services report and Powell’s testimony, I suspect it will be quiet trade heading into these events. But whilst EUR/USD remains above the 50-day EMA, then perhaps dips towards it could benefit bulls – assuming prices remain above it.

Trader’s watchlist: EUR/USD, EUR/GBP, DAX 40, CAC 40, STOXX 50

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

Latest market news

Today 04:10 PM

Today 12:30 PM

Today 09:44 AM

Today 09:34 AM

Latest Week ahead articles

December 15, 2024 01:00 PM

December 8, 2024 11:51 PM

December 1, 2024 01:00 PM

November 24, 2024 01:00 PM