The DAX was trading slightly lower, down for the third consecutive day, although it was only around 1.5% off from the recently achieved record high. Far from a turmoil, in other words. But equally, the loss of bullish momentum may be a sign that the markets could go in reverse soon. There were some disappointing company earnings from the likes of Starbucks, L’Oreal and Akzo Nobel all pointing to weaker performance in China. While none of these stocks are constituents of the DAX, most of the stocks in the German index are heavily reliant on China’s economic performance for their top and bottom lines. These softer earnings serve as a warning the DAX’s valuations might be overstretched and that a short-term correction could be on the way soon, particularly with the Eurozone also not doing so well either. And considering we are less than two weeks away from the US presidential election, global stock markets are showing very little signs of concern even though the race to White House is set to be a very close one this time. Are investors being too complacent? It is becoming increasing difficult to maintain a bullish DAX forecast even if we haven’t seen any major bearish technical shifts yet.

China’s Economic Struggles Impact Global Corporate Earnings

China’s weak economy is casting a shadow over global corporate earnings, influencing markets and indirectly shaping the DAX forecast as well. Companies with significant exposure to China are feeling the pain of slowing consumer demand and rising costs, which could affect broader economic sentiment and currency movements.

Among these companies are Starbucks, which pulled its guidance for 2025 after reporting a 7% drop in sales, marking its third consecutive quarter of declining performance. The weakness was not only evident in the US, where transactions fell by 10%, but also in China, where comparable sales plummeted by 14%.

L’Oreal and Akzo Nobel, which are listed in Europe, are also struggling in China’s sluggish economy. L’Oreal, a global beauty leader, saw its sales in North Asia dropped by 6.5% in the third quarter, marking the fifth consecutive quarter of falling sales in the region. In its report, L’Oreal highlighted that "In mainland China, the beauty market — already negative in the second quarter — continued to deteriorate, impacted by low consumer confidence.”

Akzo Nobel, Europe’s largest paint manufacturer, echoed similar concerns. The company warned that higher costs and weaker demand in China will continue to dampen profits for the rest of the year.

The ongoing struggles of major corporations in China, and those with heavy exposure to China, could play a role in shaping global market sentiment and, by extension, the DAX forecast as traders digest the impact of China’s slowing economy on global markets.

Calmer week for data shifts attention to the US presidential election

One factor that is continuing to help keep stocks elevated are signs that central banks will continue to ease policy well into 2025 amid ongoing weakness in data. This week, we saw a fresh rate cut by the People’s Bank of China, while comments from European Central Bank officials have been on the dovish side, causing the EUR/USD to break the 1.0800 handle. Also keeping the downside pressure on the euro and helping to maintain stability in European stocks this week was weaker German wholesale inflation data coming in at -1.4% y/y, suggesting that consumer inflation could fall further, thus allowing more rate cuts by the ECB. However, ongoing weakness in the Eurozone economy, coupled with political uncertainty in the US – with the presidential election now less than two weeks away – and not to mention the fact China’s markets don’t seem to be finding a sustainable recovery despite ongoing government stimulus efforts, all point to a potential dop in the coming weeks.

Key data releases this week include Thursday's PMI figures for both the manufacturing and services sectors. Central bank easing has been gaining traction as the global economy shows signs of weakness and inflationary pressures decline. The eurozone, particularly the manufacturing sector, has been a soft spot, with its PMI stuck in contraction for two years. These figures will bring the euro and major indices into focus. Any further decline in the PMIs could trigger recession concerns and negatively impact the DAX forecast.

In the US, the "Trump trade" is picking up steam following recent opinion polls and odds trackers, which suggest an increasing chance of Trump winning the presidential election. While the US dollar has shown some strength in response, the stock market hasn’t experienced significant shifts yet. Trump's protectionist policies could spell trouble for the Eurozone, especially in contrast to a potential Harris victory. If Trump’s chances continue to rise in the coming week, and other factors remain unchanged, we may see a weakening of the DAX as a result.

Technical DAX forecast and trade ideas

Source: TradingView.com

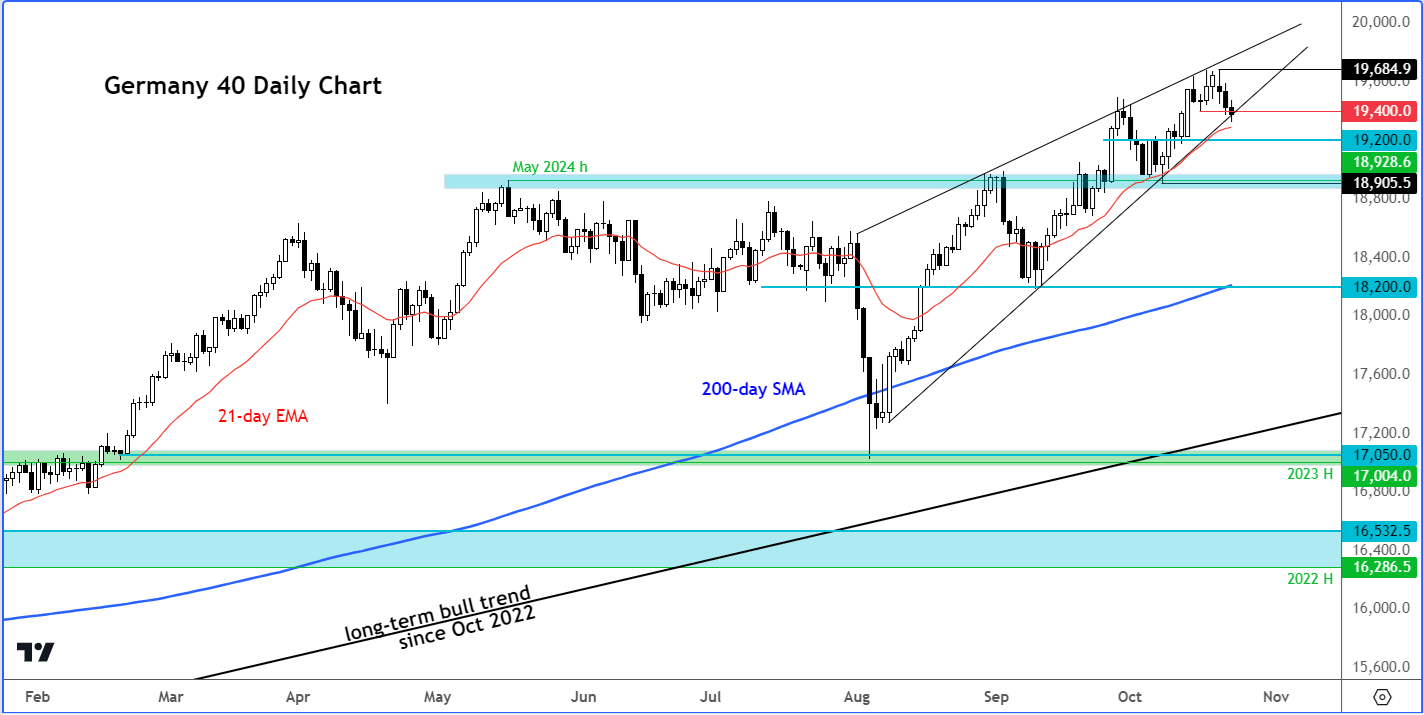

The German DAX remains in a solid bullish trend, having reached a new record high last week. Although it has since retreated from those highs, erasing Friday's gains, the bears will need to make a stronger push to shift momentum in their favor.

At the very least, a break of the bullish trend line, established since the market bottomed in August, would be required. This trend line sits near the 19,400 level, which also aligns with a key support zone. A decisive break below this area would signal a bearish shift in the short-term outlook, which could then pave the way for a deeper pullback towards the next support areas seen around 19,200 and 18910-30 (shaded in blude). The line in the sand is at 18905, marking the most recent low. Should that level break then we will have out first lower low in place and thus a clear bearish signal.

Meanwhile, if the bullish trend resumes, then the next key level to watch is the all-time high of 19685. Thereafter, the top of the rising wedge will be in focus depending how fast we will get there – if we do at all.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Latest Indices articles

Today 12:31 AM

Yesterday 12:30 PM

December 19, 2024 10:26 PM