- DAX index among Europe’s top fallers

- Italian banks leading the falls

- Moody’s cut ratings of 10 US banks

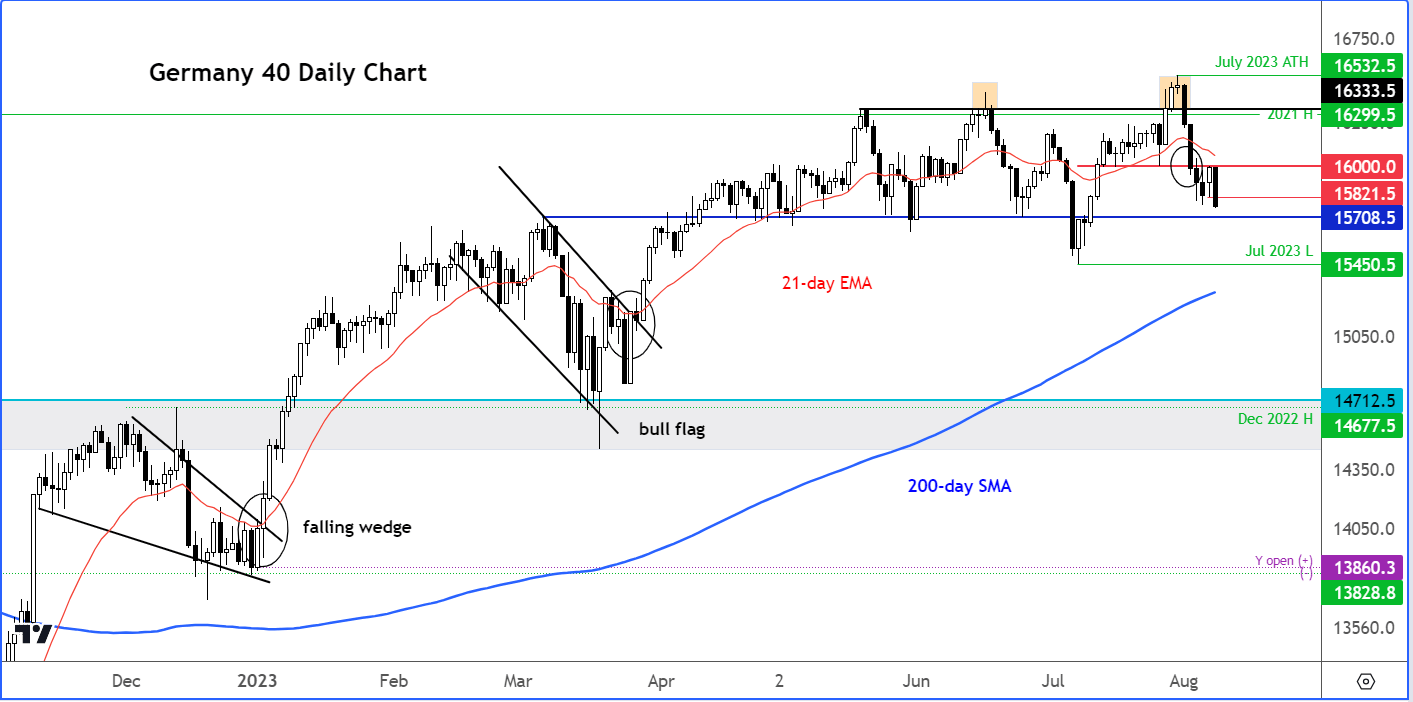

- DAX analysis: German index nearing key support level

After Monday’s positive close, the “risk off” trade returned Tuesday as European stocks and US futures slid. The Italian stock markets fell more than 2.5% to lead Europe lower. We saw noticeable falls for the Germany DAX and other leading indices in the region. The risk-off tone kept the dollar underpinned, which weighed down on the commodities like copper, gold and oil. In the FX space, the commodity dollars were typically leading the falls. But with a light economic calendar, will we see markets stage a bounce back in the second half of the day?

Why are markets falling?

There are various reasons behind the weakness we have observed in risk assets.

The fact that banks were showing the steepest falls in Europe meant that the losses in this sector were driven by Italian government’s unexpected announcement of tax on windfall profits. Shares in top lenders like UniCredit and Intesa Sanpaolo were down sharply, in excess of 6% this morning. Sentiment in the sector was further damaged after ratings agency Moody’s cut the credit ratings for 10 small and midsize US lenders.

The fact that copper was falling hard had a lot to do with China. Here, fresh data showed the world’s second largest economy was continuing to struggle as exports plunged by the most since the height of the pandemic in early 2020. China’s imports also contracted in July.

There also worries about valuations after the big rally on Wall Street lifted the major indices near record levels on Wall Street, while the likes of the DAX and FTSE hit fresh record highs earlier this year, with the German benchmark achieving that feat in July and the UK index in February.

The key theme from US company earnings so far this reporting season has been slowing sales growth – which is why stocks like AAPL and TSLA have fallen sharply off late.

DAX analysis: German index nearing key support level

While the markets were in full risk-off mode, the retreatment is taking place inside a larger bullish trend. As such, many investors will still be looking to buy the dip, because they have missed out on the rally or took profit at higher levels and want to go back in. So, always expect to see a rebound – even if it ultimately doesn’t last long.

On the DAX, a technically-important support zone was fast approaching around the 15700-15720 area. This is where the German index rallied from in July. However, if the bulls don’t show up here by causing a reversal in the short-term trend, then traders should remain patient await another bullish signal at lower levels. In the event of a bullish no-show around here today, then the July low at 15450 would become the next downside target for the bears to attack.

However, with the market moving below the short-term 21-day exponential moving average, and breaking a few important support levels such as 16000 (which then turned into resistance), the near-term path of least resistance is now to the downside until proven otherwise.

Source: TradingView.com

What will the markets focus on next?

Investors will turn their attention towards consumer inflation data, due on Thursday. US CPI inflation has fallen sharply in recent times, printing below-forecast readings in each of the past 4 months. Annual CPI fell to just 3.0% in June from around 6.5% at the start of the year, increasing the likelihood that interest rates have now peaked.

But services inflation remains high as strong wage growth continues to push up input costs. This is something that was highlighted in the NFP report, which showed average hourly earnings rising 0.4% month-on-month or 4.4% year-on-year, which was more than expected. Annual earnings have now increased by 4.4% in April, May, June and July. This shows that wage inflation is still going strong, and it is a concern for the Fed. This is especially the case for the services sector – which was also highlighted by the rise in prices paid index of the ISM services PMI.

So, there is a risk that CPI could overshoot expectations on Thursday. But with the manufacturing sector clearly struggling, and now jobs market softening a little, the Fed will feel that its policy is restrictive enough to help cool price pressures further. So, a small beat wouldn’t matter too much.

Economic data highlights for the rest of this week

The economic calendar is not that busy this week, which points to consolidation in the FX space. But we will still have at least two important data releases to look forward to from the US, which should impact all the dollar pairs, including the GBP/USD. From the UK, the main data releases will take place on the last day of the week.

US CPI

Thursday, August 10

13:30 BST

US inflation has fallen sharply in recent times, printing below-forecast readings in each of the past 4 months. Annual CPI fell to just 3.0% in June from around 6.5% at the start of the year, increasing the likelihood that interest rates have now peaked. The Fed’s policy decision in September will be entirely data dependent. Until then, we will have one more inflation report after this. Any further weakening of CPI could cement expectations of a policy hold.

US Consumer Sentiment (UoM)

Friday, August 11

15:00 BST

A goldilocks outlook in the US is what stock market investors on Wall Street have been enjoying this year – until the recent weakness. They will be looking for signs that the health and sentiment of the consumer remains positive, enough not increase the risks of a further Fed rate increase, and yet not too depressing to raise recession alarm bells. Somewhere in between could support stocks. FX investors will have already had the July jobs and inflation reports to consider along with the UoM consumer sentiment and inflation expectations surveys. If most of these indicators point to strength in the US economy, then this should keep the dollar supported on the dips.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Today 07:15 PM

Today 04:10 PM

Today 12:30 PM

Today 09:44 AM

Latest GER40 articles

Today 12:30 PM

November 13, 2024 01:00 PM

November 4, 2024 01:30 PM

October 30, 2024 12:49 PM