Week Ahead FOMC ECB and UK election

After a quiet start today, volatility should pick up from mid-week ahead of three major events. Interest rate decisions from the Fed and ECB on due on Wednesday and Thursday, respectively. Then, it is all about the snap election in the UK which is also happening on Thursday with the outcome likely to be announced late in the evening or in the early hours of Friday. Meanwhile, the US-China trade situation remains uncertain. Another round of US tariffs on $156 billion of Chinese goods is due next Sunday. That’s unless the two sides manage to strike a phase one deal in time, in which case the new and some of the existing tariffs may be cancelled. However, there was no sign of that happening at the start of this week.

FOMC likely to maintain status quo

The dollar will be in focus on Wednesday given the fact we will have the latest US CPI reading (see below) and FOMC’s last meeting for the year to look forward to. With Friday’s monthly employment report surprising even the most optimistic of forecasts, and other US macro pointers not being too bad, the Fed may well provide a more upbeat outlook on the economy than expected. If so, this could see the markets reduce expectations for a rate cut in 2020, which should help provide some support to the dollar. However, trade uncertainty will be discussed in detail - make no mistake about it. For as long as there is a risk that the trade talks collapse, the risks to the economic outlook would be skewed to the downside. Meanwhile, policymaker may also take note of the somewhat alarming slowdown in US manufacturing activity as we have seen over the past few months. Although this may be due to temporary factors, prolonged weakness in the sector could potentially lead to job losses and impact other sectors of the economy. The Fed may therefore monitor factory activity closely going forward. All told, we think the FOMC’s policy statement or press conference will contain few surprises.

Lagarde’s first ECB policy decision

The European Central Bank’s last policy decision and press conference for 2019 will be on Thursday. However, this will be Christine Lagarde’s first policy decision as the ECB head. Judging by her few speeches since she took over, it is unlikely the ECB will alter monetary policy. However, Lagarde may announce some changes in the way the central bank has been doing things under her Italian predecessor Mario Draghi – this will unlikely cause too much of a reaction in the euro. Meanwhile, economic data in the Eurozone has been poor for much of 2019, although we have seen some positive surprises here and there of late. The improvement has been nothing too significant, however. We therefore think the ECB will maintain is dovish view. The single currency could come under some pressure, before the focus shifts to the UK election and Brexit…

PM Boris Johnson’s Tories expected to win majority in UK election

The UK’s eagerly anticipated general election is on Thursday with the outcome set to be announced late on the day or in the early hours of Friday. The means that the pound – and by extension, the FTSE – will be among the most important markets to watch for volatility towards the end of the week. Here is what my colleague Fiona Cincotta wrote earlier today on the pound and election:

- Boris Johnson maintains a healthy lead in the polls in the last few days heading towards the elections. The latest data showing voters intentions puts Boris Johnson with a double-digit lead of 11.9 points ahead of Labour’s Jeremy Corbyn.

- Traders are looking for the Tories to win by an overall majority. This is being seen to pave the way for Boris Johnson’s Brexit bill to pass quickly through Parliament, enabling the UK to leave the EU early next year with a deal in place.

- Conservative market friendly policies are also playing a part in boosting sterling. These are favoured over Jeremy Corbyn’s left leaning policies and the uncertainty that he brings to Brexit.

Other important macro events this week

- A handful of European data on Tuesday (e.g. German ZEW and UK GDP, construction and manufacturing output) are likely to be just a distraction ahead of the more important events later in the week.

- US CPI will provide some volatility for the dollar before Wednesday’s more important Fed decision takes centre stage (see above). Economists are predicting consumer prices to have risen to 2.0% on year-over-year basis, up from 1.8% previously. On a month-over-month basis, CPI is seen rising 0.2%. Meanwhile, core CPI is expected to have remained unchanged at 2.3% y/y with the m/m reading seen at +0.2%.

- Swiss National Bank’s monetary policy decision is on Thursday – this is unlikely to cause too much of volatility given that the SNB has not altered its policy in years and are unlikely to do so again this time.

- US retail sales on Friday will provide some distraction to what we think would be a volatile day for the pound. Still, the dollar could move meaningfully against other currencies, should retail sales surprise to the upside. Both headline and core sales are expected to print +0.4% respectively.

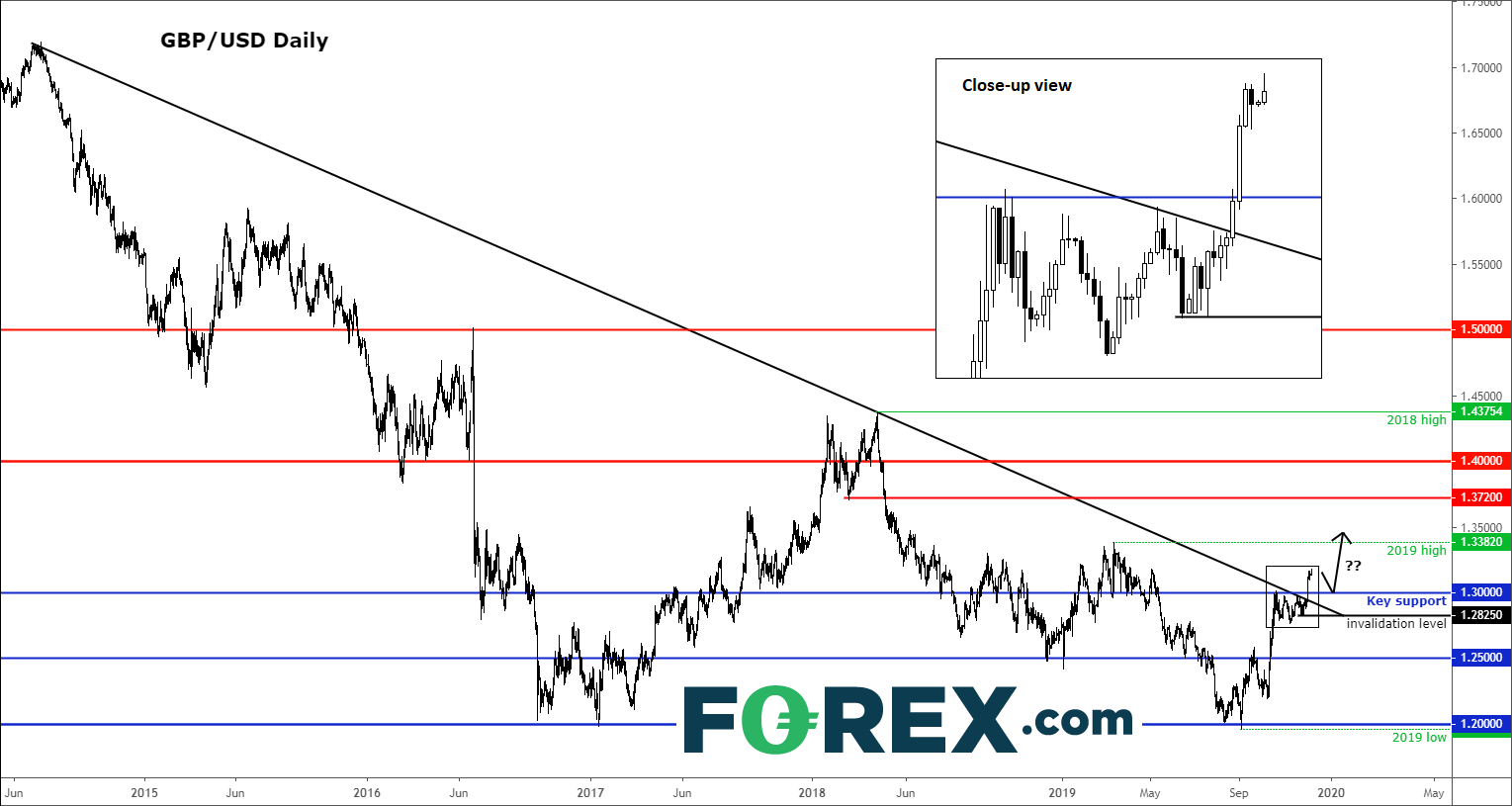

Featured chart: GBP/USD

{kind=link}

Source: Trading View and FOREX.com.

Given the importance of the UK election, which could shape the direction of Brexit, the pound is going to be the most important currency to focus on this week, we think. Like other pound crosses, the main GBP/USD pair has been making higher highs and higher lows in anticipation of a Conservatives majority win. If the polls were to tighten ahead of the elections, then the cable may pull back to the 1.30 handle before potentially resuming higher. As well as being a psychologically-important level, this was formerly resistance meaning it could turn into support upon a potential re-test. If the upward trend continues, as we think it might, then the liquidity above this year’s earlier high at 1.3380ish is the bulls’ main objective. The bears, meanwhile, will want to see a break down well below the 1.30 handle, and some bearish news too in so far as the election is concerned. A potential move below the most recent low circa 1.2825 would be the ideal outcome for them. However, at the time of writing, the bulls were in full control…

The information on this web site is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement. The information and opinions in this report are for general information use only and are not intended as an offer or solicitation with respect to the purchase or sale of any currency or CFD contract. All opinions and information contained in this report are subject to change without notice. This report has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. Any references to historical price movements or levels is informational based on our analysis and we do not represent or warranty that any such movements or levels are likely to reoccur in the future. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness, nor does author assume any liability for any direct, indirect or consequential loss that may result from the reliance by any person upon any such information or opinions.

Futures, Options on Futures, Foreign Exchange and other leveraged products involves significant risk of loss and is not suitable for all investors. Losses can exceed your deposits. Increasing leverage increases risk. Spot Gold and Silver contracts are not subject to regulation under the U.S. Commodity Exchange Act. Contracts for Difference (CFDs) are not available for US residents. Before deciding to trade forex, commodity futures, or digital assets, you should carefully consider your financial objectives, level of experience and risk appetite. Any opinions, news, research, analyses, prices or other information contained herein is intended as general information about the subject matter covered and is provided with the understanding that we do not provide any investment, legal, or tax advice. You should consult with appropriate counsel or other advisors on all investment, legal, or tax matters. References to FOREX.com or GAIN Capital refer to StoneX Group Inc. and its subsidiaries. Please read Characteristics and Risks of Standardized Options.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Contracts for Difference (CFDs) are not available to US residents.

FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited, 30 Independence Blvd, Suite 300 (3rd floor), Warren, NJ 07059, USA is a member of the Canadian Investment Regulatory Organization and Member of the Canadian Investor Protection Fund. GAIN Capital – FOREX.com Canada Limited is a wholly-owned subsidiary of Stonex Group Inc.

Complaints are taken very seriously at FOREX.com. You can view our complaints procedure here.

© FOREX.COM 2025