VIX, Yen, Treasury Yields Talking Points:

- The VIX ‘fear index’ has spiked to an 18-month high following the Non-farm Payrolls report, going along with an aggressive sell-off in US equities to go along with the USD/JPY move.

- Weekend Gap Risk: Nikkei futures have continued to sell-off since Japanese markets closed for the week so it’s reasonable to imagine that there could be gaps on the Sunday open. Be careful with risk as we move towards the weekly close.

- If want to learn more about technical or fundamental analysis, along with trading strategy, The Trader’s Course can help: Click here to learn more.

It’s been a massive week for macro as expected, but the size of the moves and the areas that volatility has shown are notable. In effort of cleanliness, I’m going to try to parse through these one at a time, using charts as visual aides to illustrate the depth of this week’s reactions.

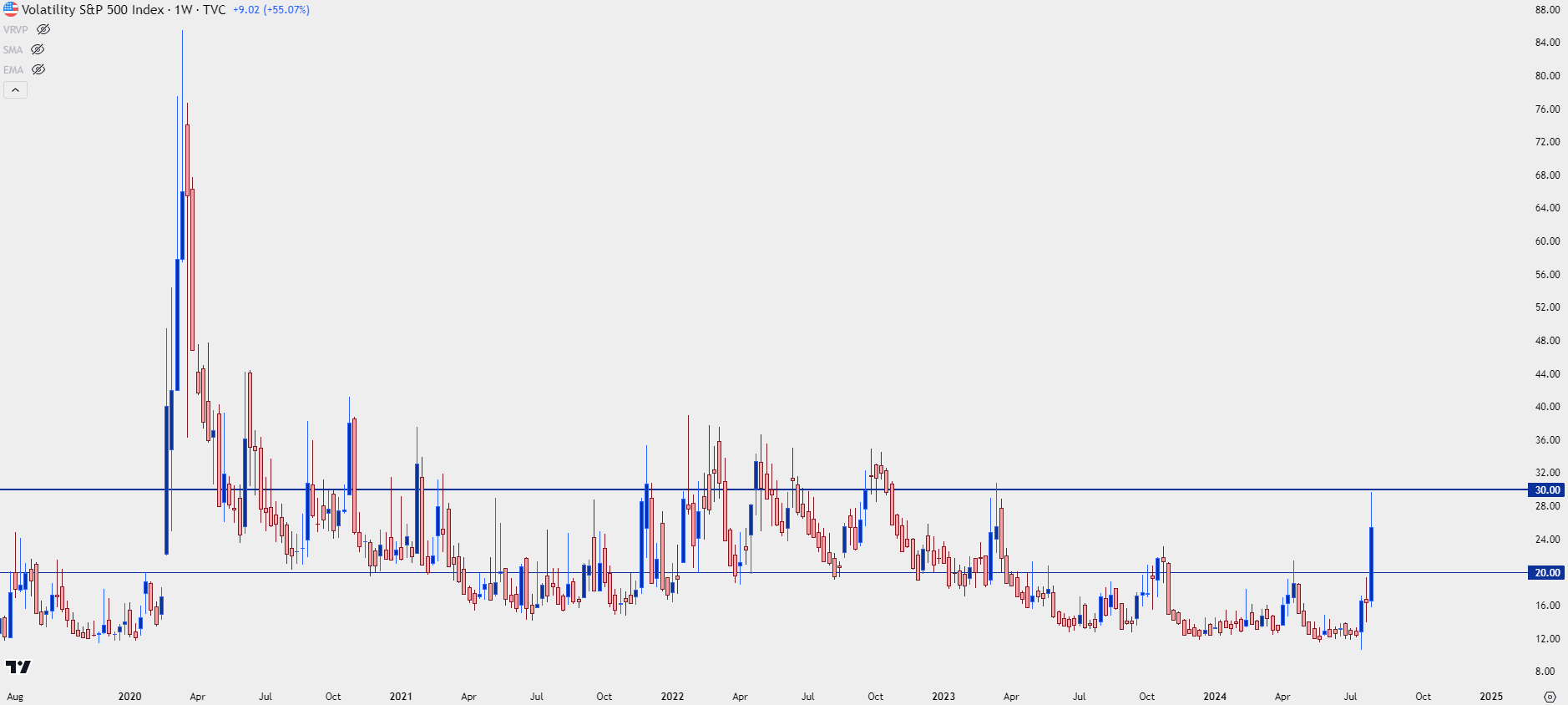

Firstly, the VIX ‘fear index’ has spiked to an 18-month high. This is derived from options activity on SPX so given the moves in US equities, it makes sense. But, putting this into perspective, the ‘20’ level is often looked at as a cut-off for the index and there was just one single day so far this year where VIX has traded above 20. That was right at the Q2 low for the S&P 500 and as bulls returned, VIX softened and moved back-below 12.

That indicates a degree of complacency that’s built-in to markets as the Fed was laying the groundwork for rate cuts. But, as the shock of this morning’s NFP hit an already-vulnerable market, VIX has shot-higher while making a fast run at the 30-level.

The last time the index was this high was March of 2023, right around the time the regional banking crisis had come into the equation. This shows that fear is increasing, and that complacency has started to take a back seat.

VIX Weekly Price Chart: Highest Since the Regional Banking Crisis in March, 2023

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

A Yield-Driven Move

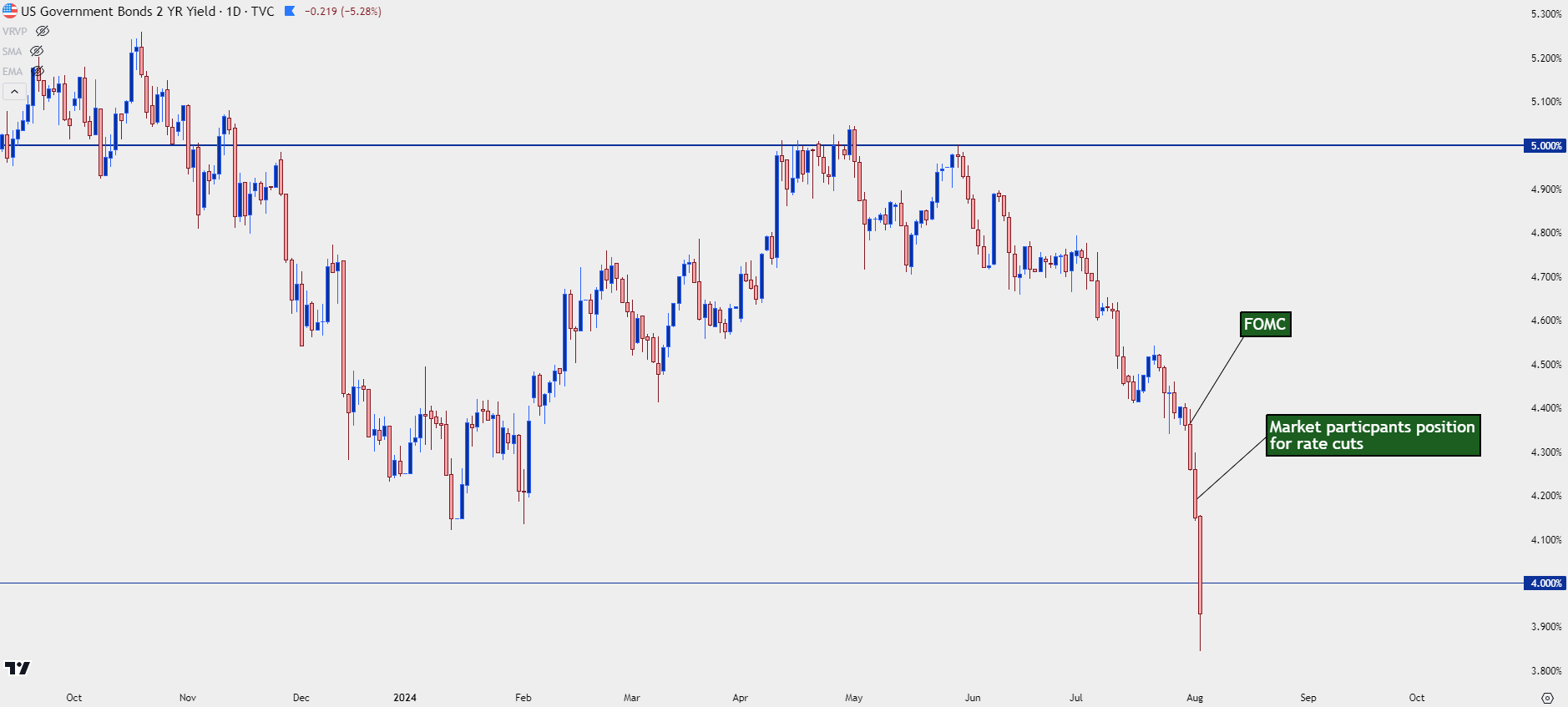

Markets have long been expecting rate cuts from the Fed, that’s not a secret. And on Wednesday, the wide expectation was that the FOMC would begin to lay the groundwork for cuts to begin at their next meeting in September. And when trading closed on Wednesday there was still the expectation that the bank would cut three times in their final three meetings of the year.

But market participants aren’t often willing to wait around, and what showed after that meeting was a continued bid in Treasuries as hedge funds and market participants tried to get in-front of those potential FOMC rate cuts. If short-term rates go down, there’s opportunity for principal pops in those bonds and that can become an attractive trade, particularly when the previous market darlings of the Mag 7 continue to see pullbacks from oversold conditions.

In the 2-year Treasury, yields are now below 4% for the first time since May of 2023; and just two months ago yields were at 5%. This is a massive market, and a move of that nature entails a lot of buying. That cash came from other pockets of the market, such as tech stocks, and this helps to explain the continued sell-off in equities which I’ll get to in a moment.

2-Year US Treasury Yields: Sub-4%

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

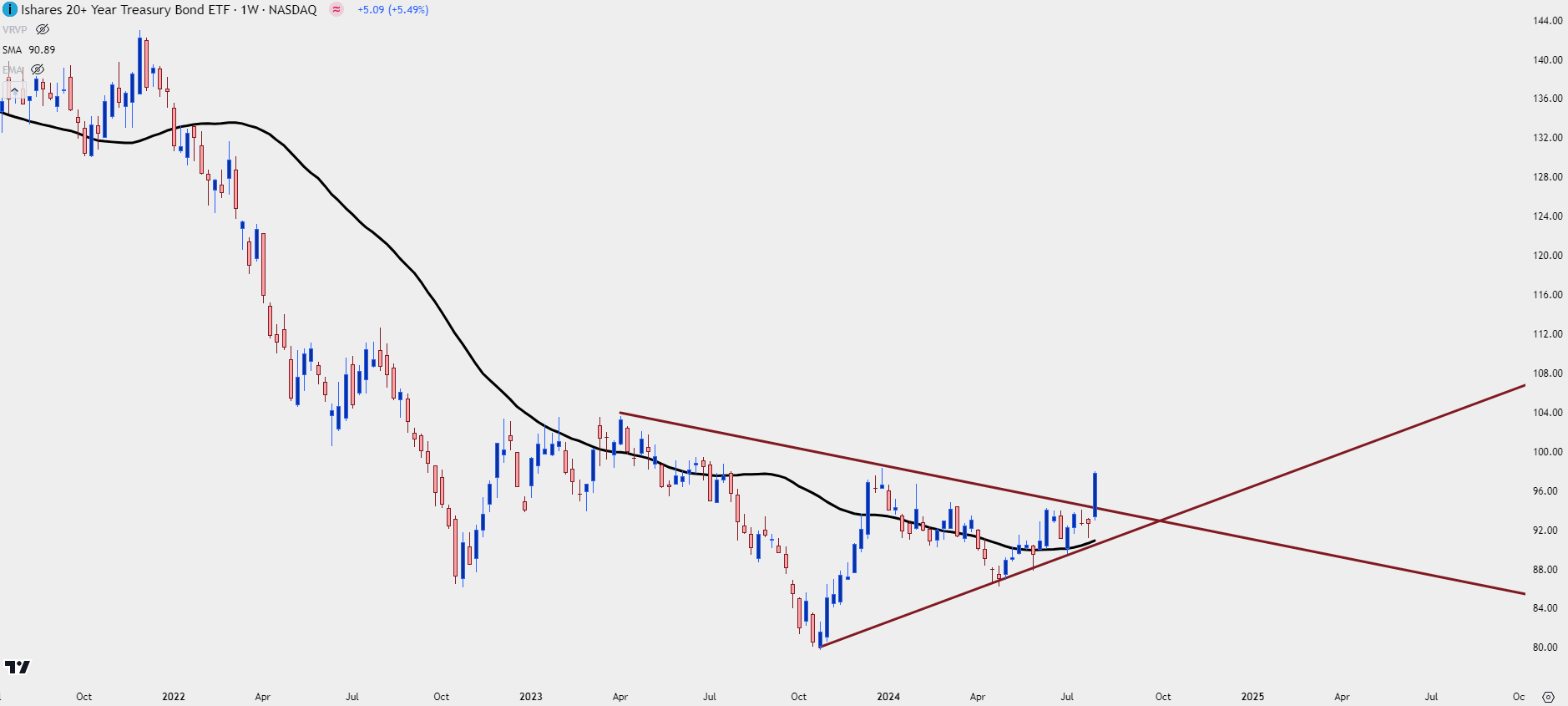

If the Fed cuts rates and the rest of the Treasury curve follows, there’s opportunity for principal gains in bonds, such as we can see in the ETF of ‘TLT,’ which is working on its strongest week since March of 2020, right around when the pandemic started to get priced-in. This represents Treasuries with 20+ years of maturity so as expectations build for cuts to come in, there’s opportunity for principal gain in this ETF as there is in US Treasuries, as well (prices up, yields down).

TLT Weekly Price Chart: Up 5.51% This Week

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

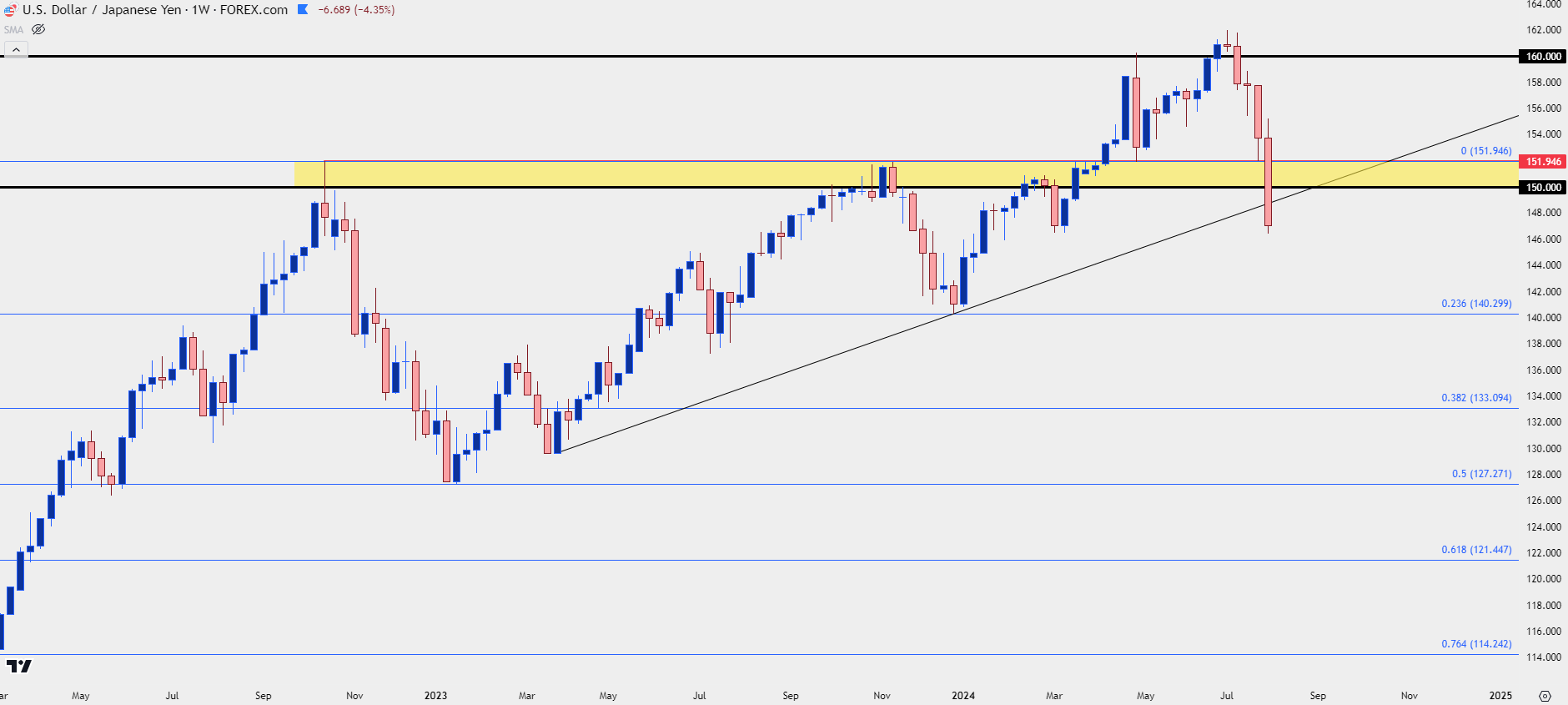

USD/JPY Carry Unwind as Yields Fall

As US Treasury Yields fall, so does the attractiveness of carry trades such as USD/JPY: And it’s not only the major market that’s seeing fast reversions as EUR/JPY, GBP/JPY and AUD/JPY have all been offered heavily over the past week. I warned of this yesterday and those markets have continued to sell-off since.

But this is something that can have some carry-over effect as we move into next week’s trade. As prices continue to fall further, longer-term positions see more incentive to close the position and realize whatever floating profits might be left as the yield trade shows more signs of being finished.

USD/JPY Weekly Price Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

Stocks

US equities have been hit hard but we need to put the move in scope of the broader backdrop. The Q2 sell-off showed intensity, at times which is why we had that previous VIX flare over 20. But that abated quickly. And with a Fed seemingly ready to begin cutting there could be a positive factor for equity markets to work with.

The bigger question at this point is one of opportunity cost: Is that trade in Treasuries going to be too attractive for capital flows to run back into equities? And is a larger retracement needed?

At this point there’s no clear evidence of a bottom being in but chasing equity prices lower after the VIX spike above could be a challenging way of adding on exposure. It would essentially be looking for panic to turn to pandemonium.

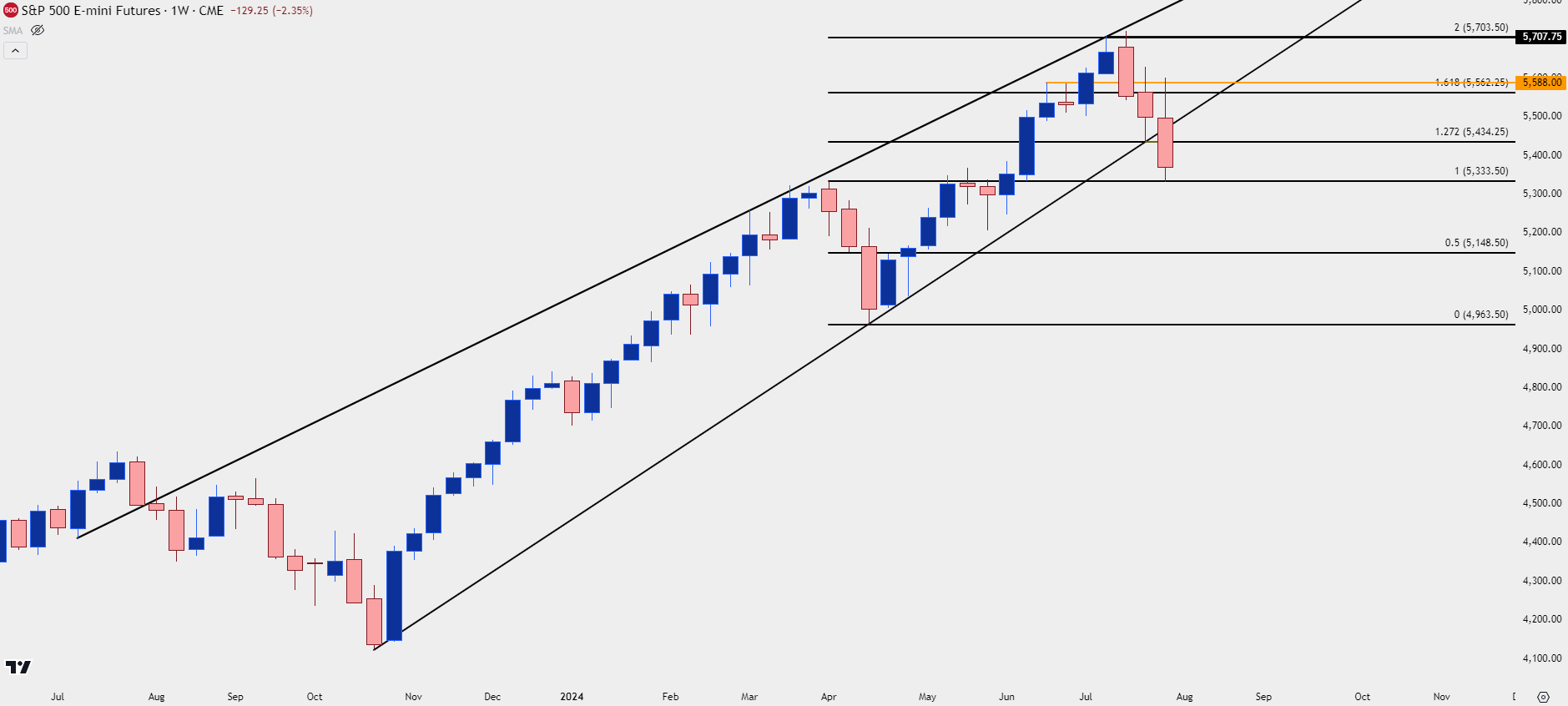

In S&P 500 Futures, I have price testing a key spot at 5334, which was a prior high at the Q2 open. I had highlighted this structure on Thursday before the breakdown and that remains in-play. But, notably, the index broke through support in a rising wedge this week which is a formation often followed with bearish reversal aim. Key resistance now shows at prior support, 100 points above that support at 5434.

S&P 500 Daily Price Chart

Chart prepared by James Stanley; data derived from Tradingview

Chart prepared by James Stanley; data derived from Tradingview

Recession Fears

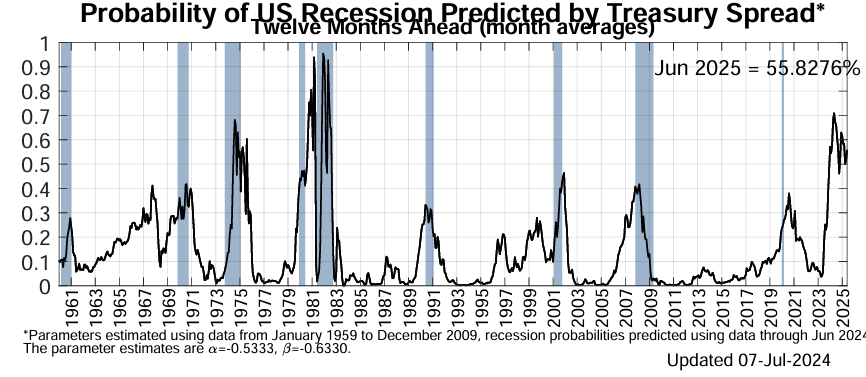

I saved this for last as I don’t consider it a directly actionable market setup, but the big percolating fear behind much of this volatility is the growing idea that we may be headed for recession. This morning’s NFP data confirms a trigger of the Sahm rule, which is a recession indicator that many economists follow.

And this isn’t the first time that we’ve heard of something similar as the Fed has continued to harbor a greater than 50% probability of a recession in the next 12 months, as highlighted by their work on the 10-year/3-month Treasury spread. At last release in early-July, this showed at 55.8% and this week’s movement in Treasuries has only forced deeper inversion of that indicator.

The Fed has a plethora of research behind that data point at this page: Federal Reserve Bank of New York: The Yield Curve as a Leading Indicator.

The yield curve has been inverted for a long time and, again, complacency set in to the point where many began to question whether this was legitimately a forewarning of recession. But, now that the Sahm rule has been triggered that fear has started to take-over and the big question now is whether the Fed is behind the curve as continued weakness seeps into US labor markets.

US 10-Year/3-Month Treasury Spread: Probability of US Recession

Chart prepared by James Stanley; data derived from FRBNY, ‘Probability of U.S. Recession Charts

--- written by James Stanley, Senior Strategist

Latest market news

Today 12:30 PM

Today 09:44 AM

Today 09:34 AM

Yesterday 07:55 PM

Latest articles

Today 12:30 PM

Today 09:44 AM

Yesterday 07:55 PM

Yesterday 05:50 PM