- US economic growth continues to outperform with inflation risks far more balanced than a couple of months ago

- That’s seen markets pare US Federal Reserve rate cut expectations from more than seven in 2024 to just over four

- That’s contributed to US two-year Treasury yields pushing back towards 4.5%, where buyers have previously stepped in over the past two months

- Higher yields may create renewed headwinds for cyclical assets and yield sensitive markets.

US two-year Treasury yields are at risk of breaking back into the higher range they traded in prior to the Federal Reserve’s policy pivot last year, creating opportunities in markets sensitive to shifts in US rate expectations such as Australia’s ASX 200, USD/JPY and gold.

US economic momentum remains strong

The resilience of the US economy has been on full display in 2024, maintaining the momentum it carried throughout much of 2023. Despite the fastest and largest episode of monetary policy tightening from the Federal Reserve in decades, the world’s largest economy continues to purr like a well-oiled machine, creating a warranted rethink from traders worldwide as to just how many times the Fed will need to cut interest rates this year as it attempts to engineer a soft economic landing.

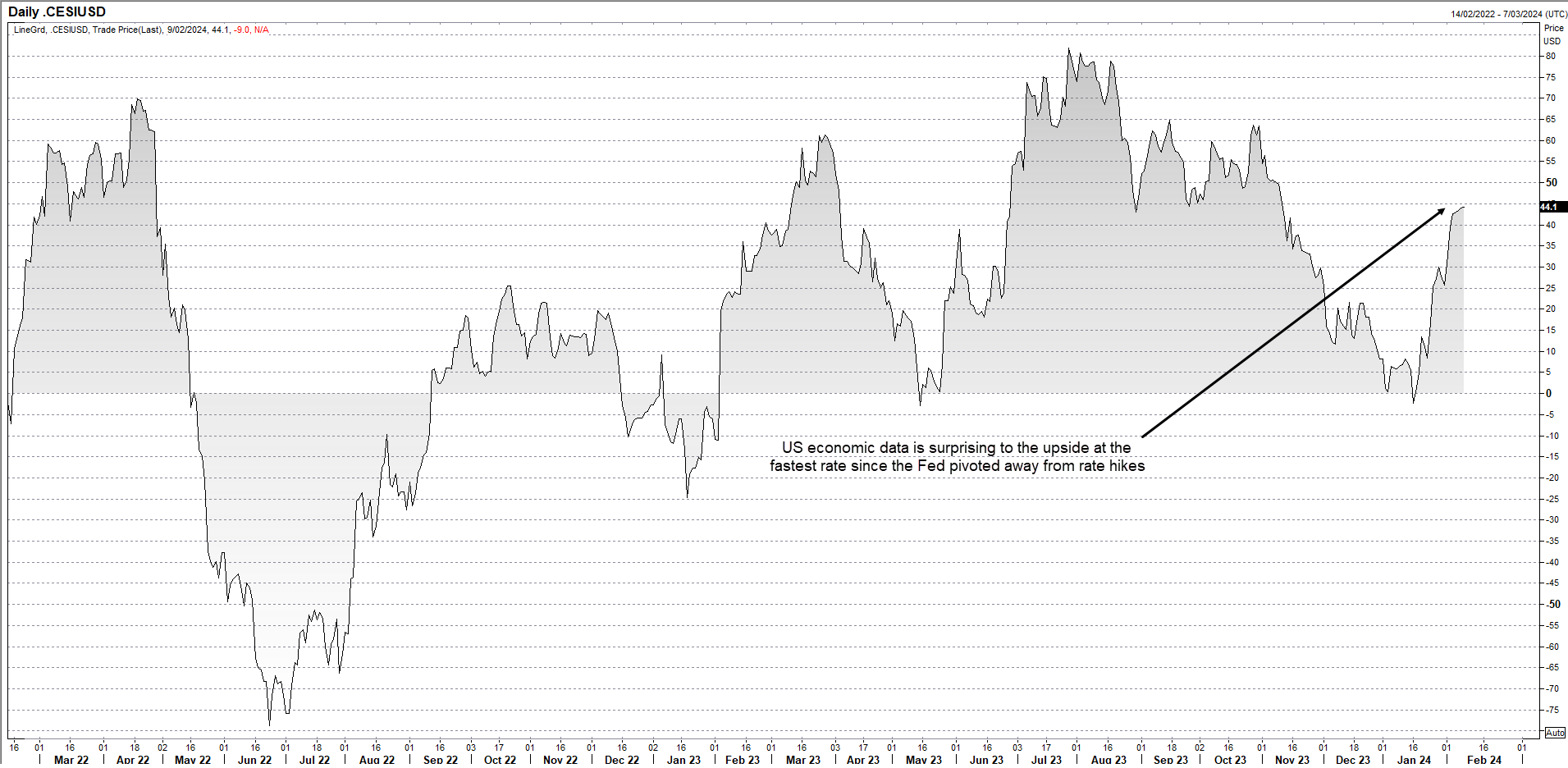

Just look at the rebound in Citigroup’s FX economic surprise index for the United States over the past month, signallling that on a net basis, information on the economy is now topping market expectations at the highest rate in over three months.

Source: Refinitiv

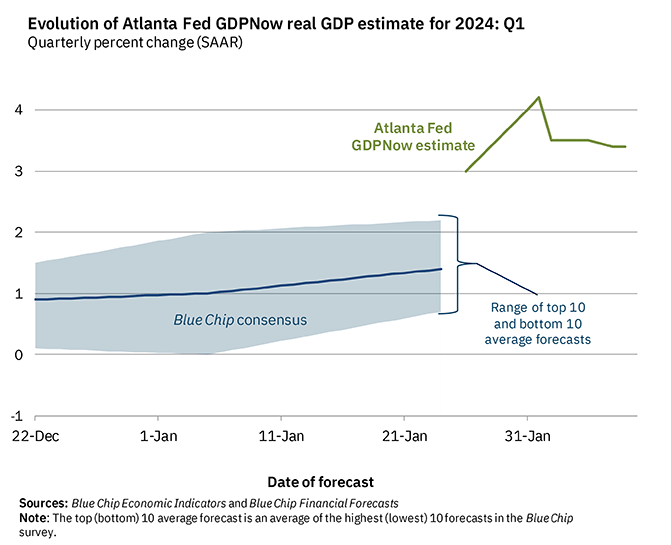

While we’re only halfway through the March quarter, the Atlanta Fed GDPNow model – which aims to predict US economic growth in real time – suggests the economy is expanding at an annual rate of around 3.4% based on recent indicators.

Source: Atlanta Fed

Not only does this maintain the pattern of GDP growth vastly outperforming expectations, but it also suggests the economy is operating above its long-run potential level, pointing to the risk of inflationary pressures reemerging should productivity begin to stagnate.

Fed policy settings may not be as restrictive as thought

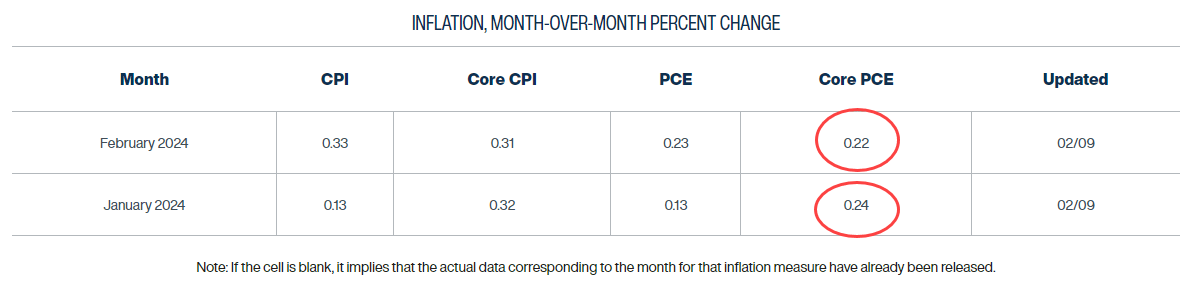

While core PCE inflation – the Fed’s preferred measure of underlying price pressures – has fallen back to its 2% annual target when measured in three and six-month annualised terms, the pace looks to be in the process of troughing.

Source: Cleveland Fed

Combined with economic growth well above levels that would normally keep inflation stable, it begs the question why the Fed needs to cut rates aggressively this year? Based on evidence at hand, policy settings don’t appear to be as a tight as markets initially anticipated, making the need for even less restrictive settings weak at best.

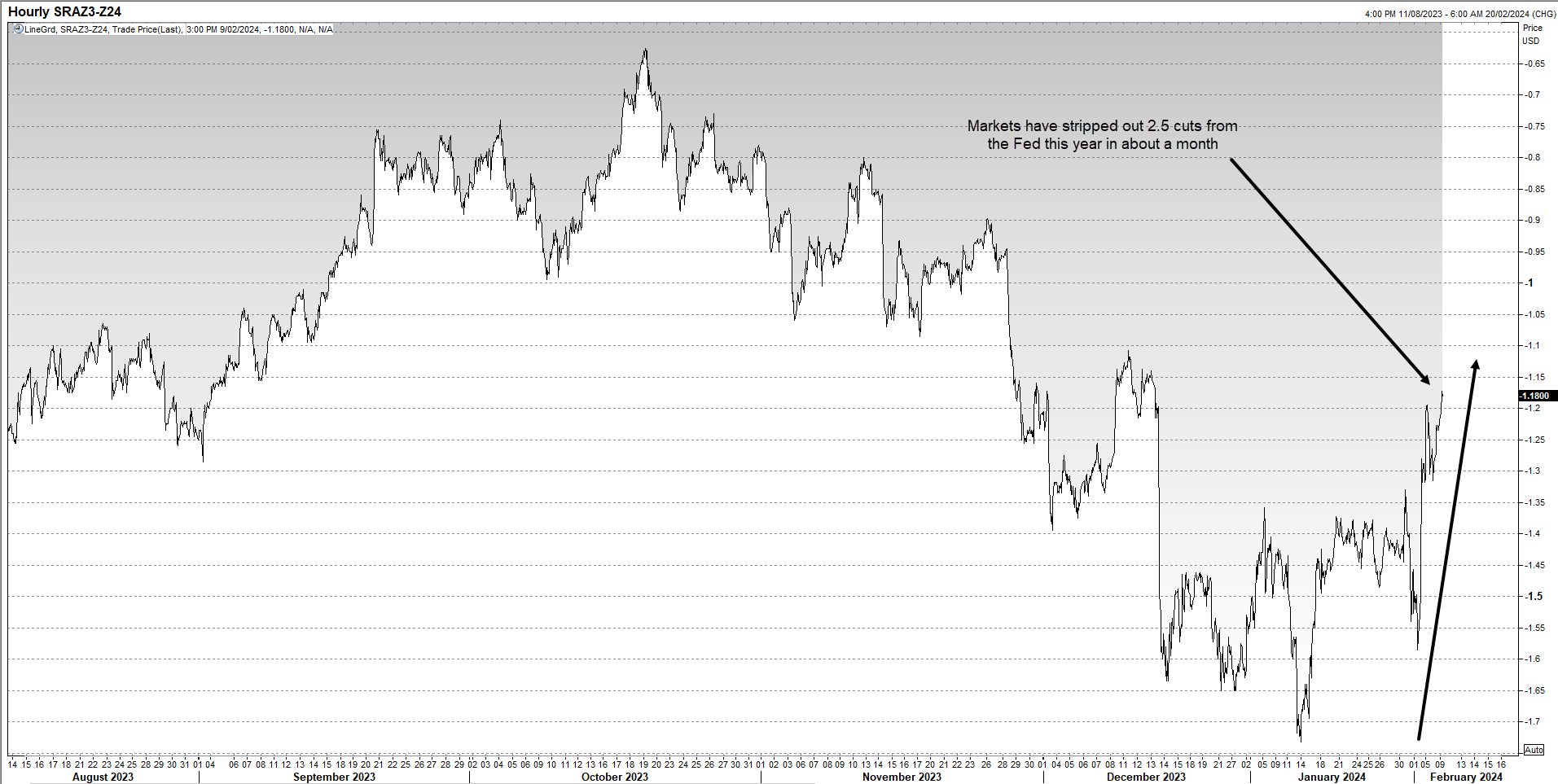

Which has seen markets pare rate cut expectations

Having priced in as many as seven 25-point cuts over 2024 earlier this year, markets have been scaling back their expectations ever since, trimming pricing to around 4.5 cuts at the time of writing. The SOFR [Secured Overnight Financing Rate] 2024 curve – which can be used as a proxy for Fed funds rate expectations this year – shows just how rapidly markets have stripped out 2.5 rate cuts as the debate over whether we’ll see a soft or hard landing shift to whether we’ll see a landing at all. The risks for inflation appear to be much more balanced than they were just a couple of months ago.

Source: Refinitiv

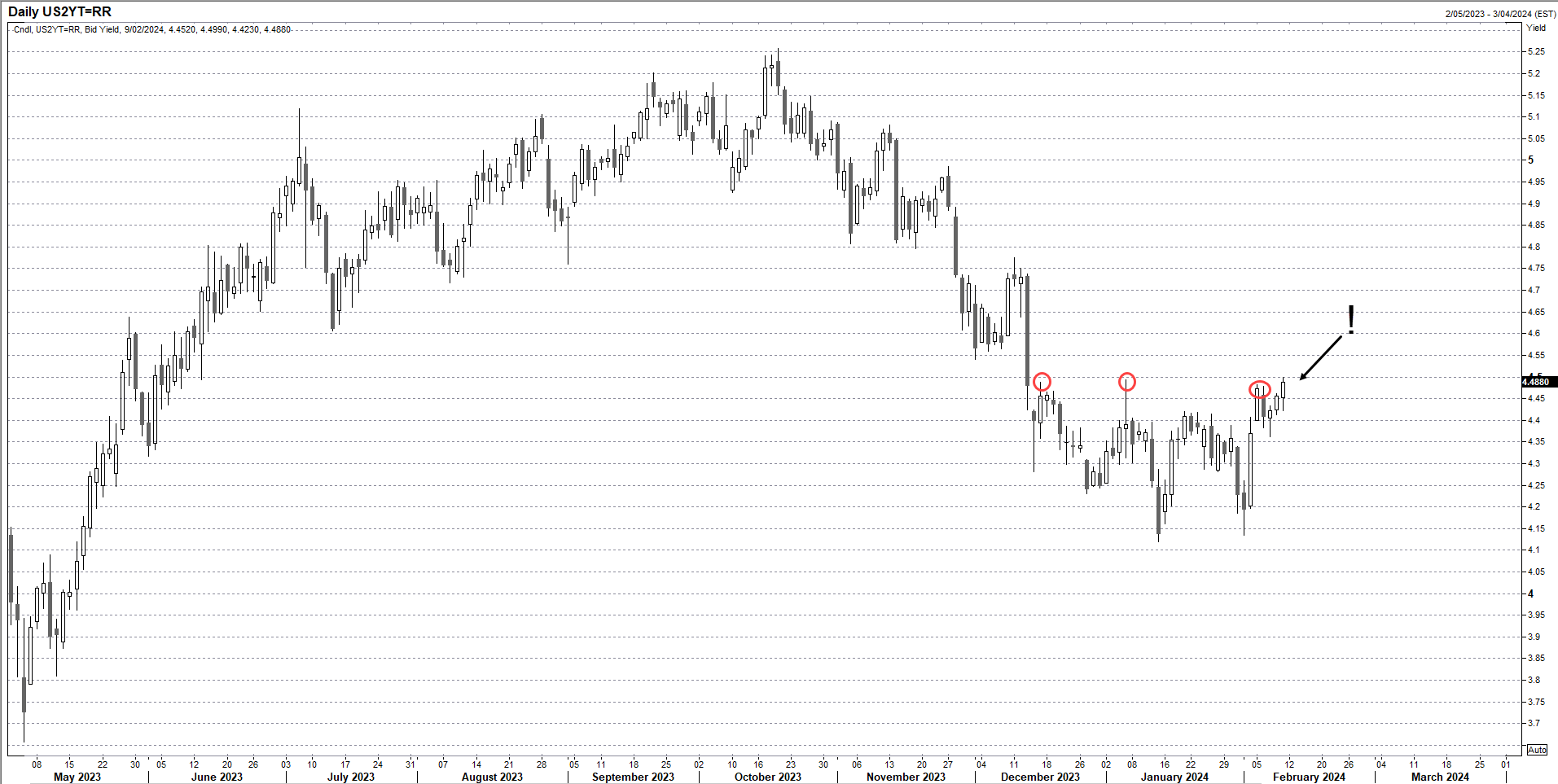

US two-year yields at top of recent range

Combined with significant new Treasury and corporate debt issuance, the unwind of rate cut bets has contributed to short-end bond yields pushing aggressively higher, seeing two-year yields threaten to break above 4.5%.

If you look on the daily chart below, that’s where buyers have moved in since December, helping to cap yields below this level. But will that remain the case when the momentum with the economy, interest rate expectations and inflation all moving in the same direction? It feels like a matter of when, not if, right now unless something serious in the economy breaks.

Source: Refinitiv

If yields do break higher, it will have implications for a variety of asset classes, especially those which rallied the hardest when rate cut and soft-landing bets were in full swing in the final months of 2023.

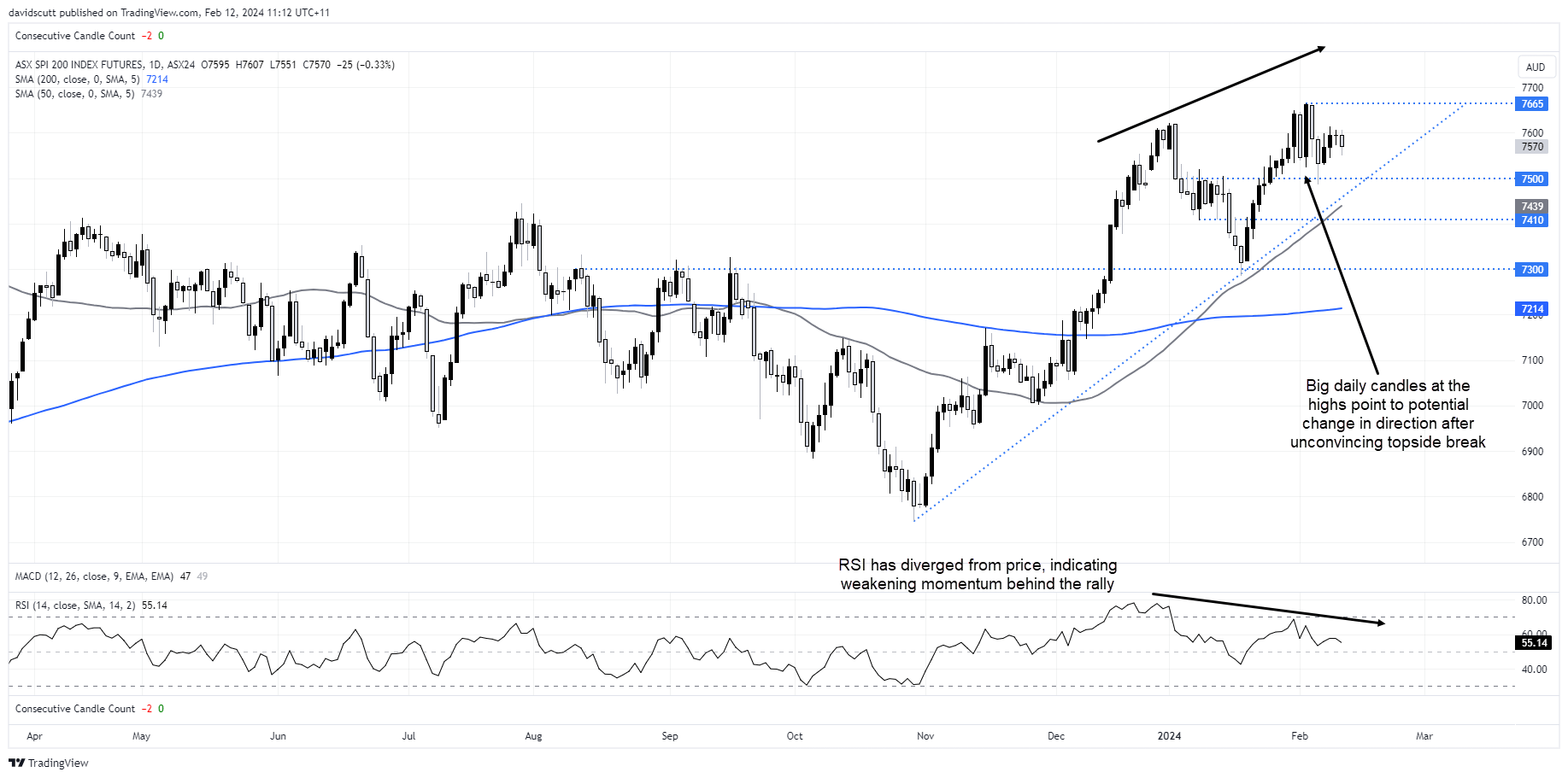

ASX 200 looks vulnerable to rate outlook recalibration

Australia’s ASX 200 stands out as one market that looks particularly vulnerable to a recalibration in the global interest rate outlook.

There are convincing topside breaks, such as those seen for the Nasdaq and Nikkei, and there are those that are not. Having surged to record highs after a near 14% rally from the lows hit in late October, the price action since has been anything but convincing with a series of lengthy daily candles in both directions giving sense to a potential shift in direction.

Divergence between RSI and price – with the former setting lower highs even as the price hit fresh records – provides another question mark on the longevity of the rally.

While futures remain in an uptrend for now, without multiple expansion driven by lower rates, traders need to ask themselves where the next leg of growth will come from, especially with China stimulus hopes entirely baked in while financials have already run so hard.

Probes above 7600 have been sold recently, giving those traders looking to play the market from the short side an attractive entry level. On the downside, support is found around 7500, 7410 and 7300, with the uptrend from October located in between. A stop above the high of 7665 would provide protection against reversal.

If the Australian equity market isn’t your thing, cyclical assets that rallied hard between November to late December would be other candidates to consider short setups should US short-term yields break higher.

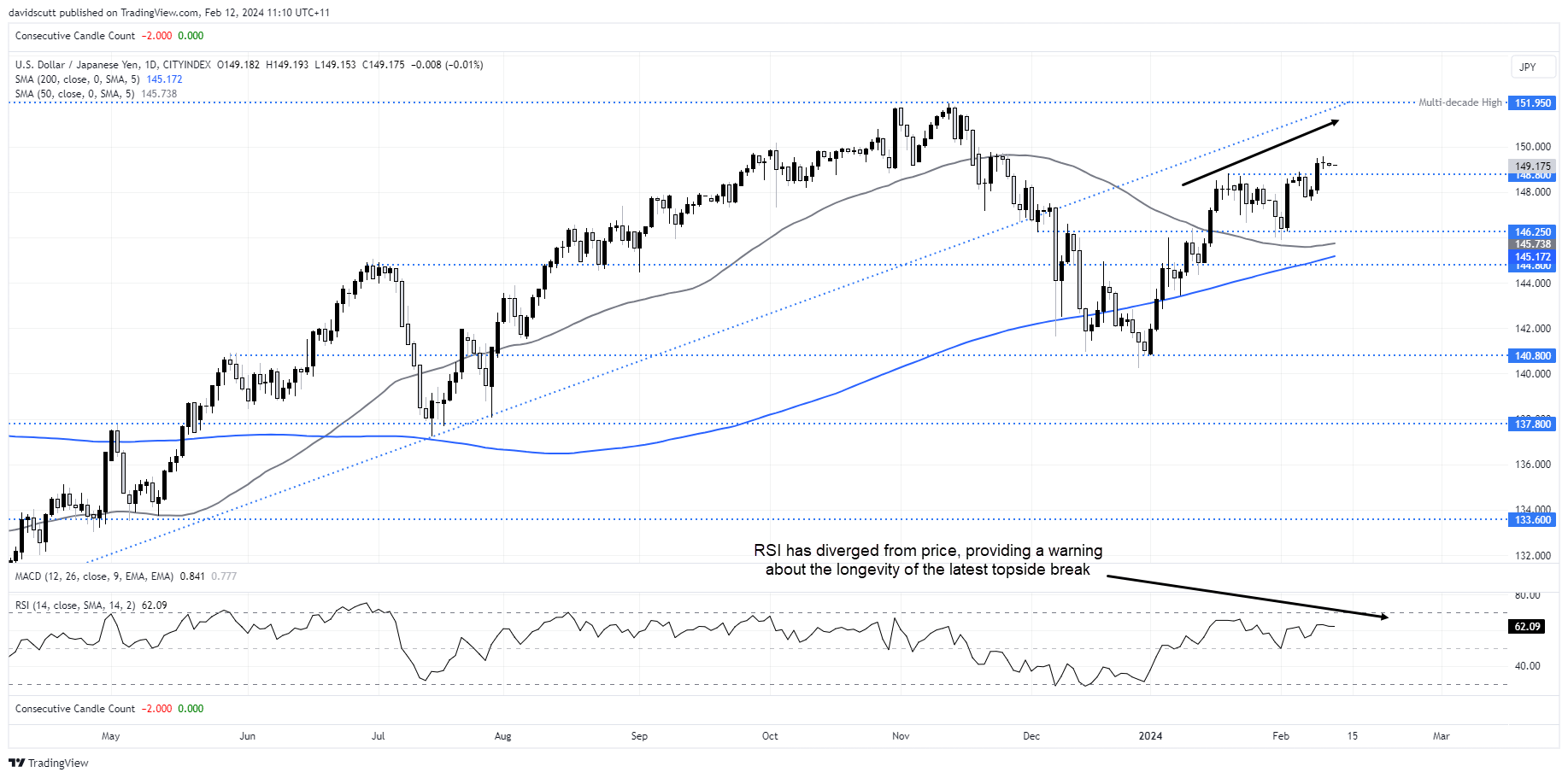

USD/JPY closing in on 150 as US yields lift

In the FX space, there are few better pairs to trade shifts in relative interact rate expectations than USD/JPY. It’s no surprise that with US two-year yields closing at the highest level since early December on Friday, USD/JPY also sits at multi-month highs. All else being equal, should US yields break higher, the path of least resistance for the pair is also likely to be higher.

Having broken resistance at 148.80 last week, traders will be eying a potential retest of the multi-decade highs just below 152.00. Should US yields reverse, downside levels to watch include 146.25 and 144.80. One cautionary indicator about the potential for continued upside is the divergence between price and RSI since late January.

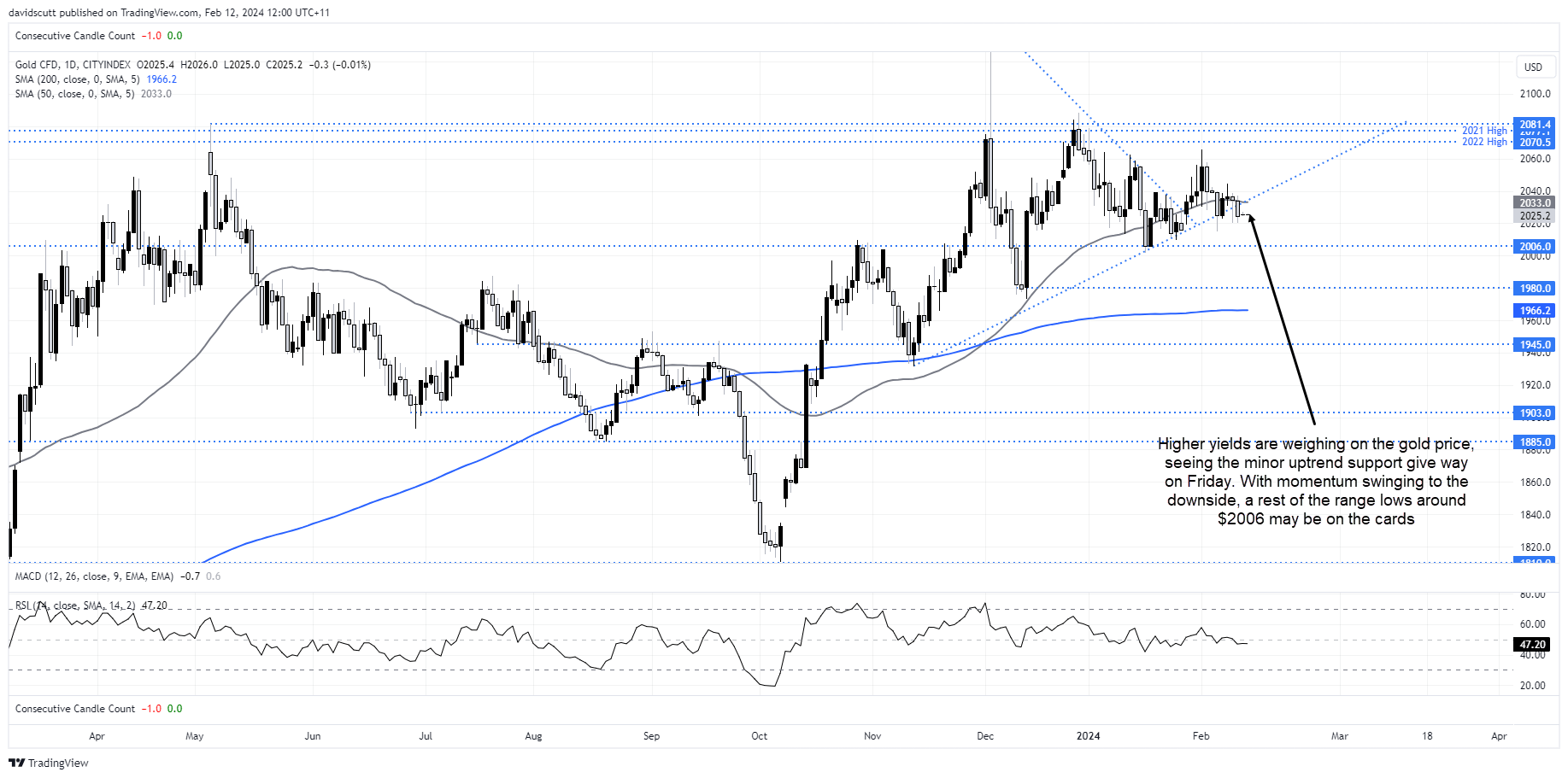

Gold easing lower towards test of channel support

Gold is another market that will be watching US yields closely, sitting comfortably in sideways channel above $2000 an ounce. With higher yields helping to fuel a stronger US dollar, gold broke uptrend support on late last week, putting a retest of the bottom of the channel at $2006 into play. A break there opens the door for a push towards $1980 and 200-day moving average located at $1966.

Right now, in the absence of a significant escalation in geopolitical tensions, resistance layered from $2070 does not look to be under threat.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Yesterday 07:31 PM

Latest articles

December 19, 2024 05:22 PM

December 10, 2024 07:00 PM

December 9, 2024 05:26 PM

November 26, 2024 06:30 PM