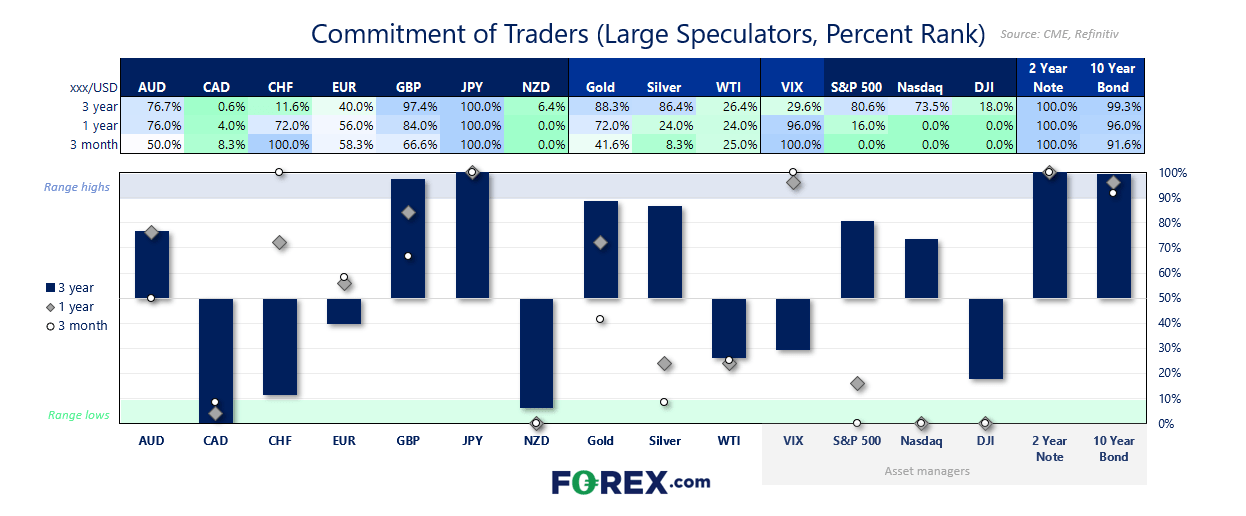

View the latest commitment of traders reports

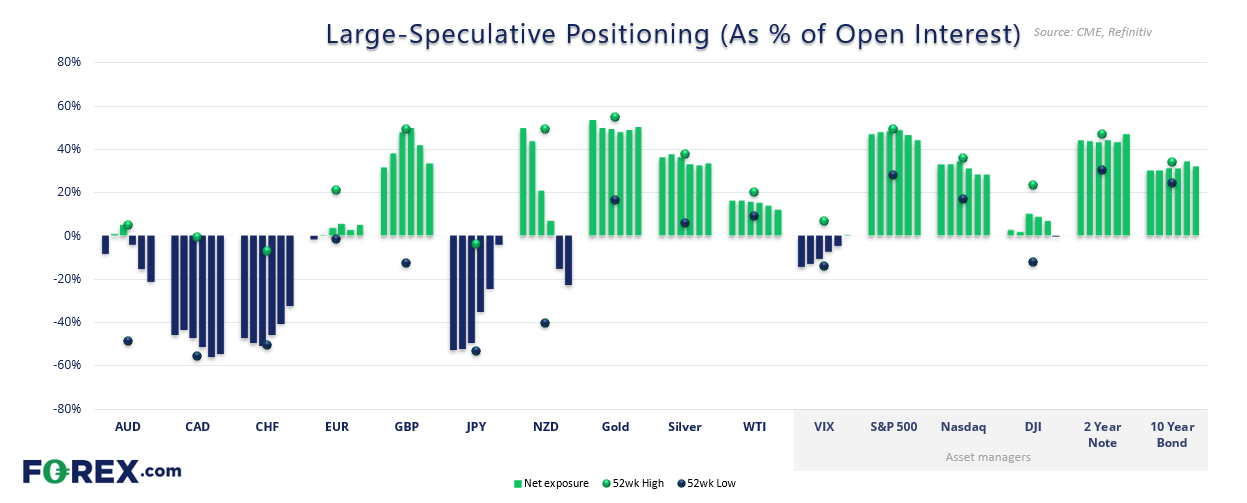

Market positioning from the COT report - as of Tuesday 6 August, 2024:

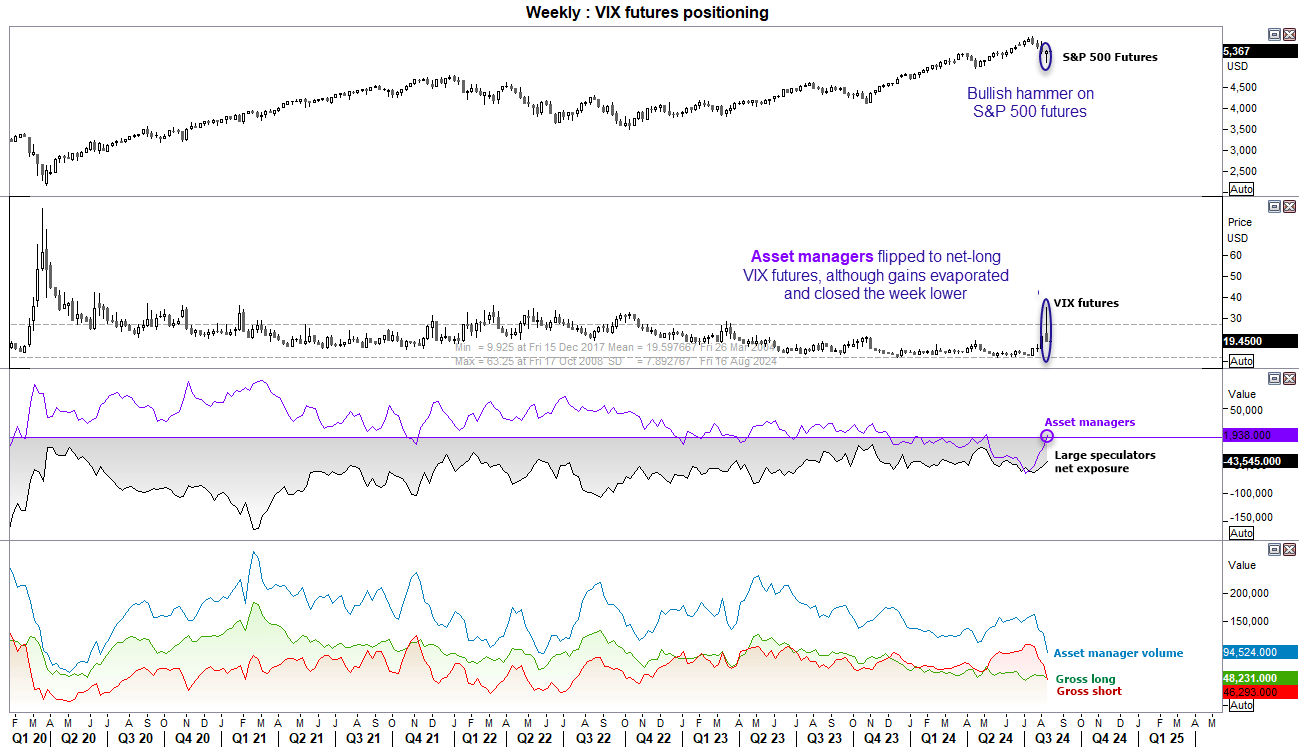

- Large speculators flipped to net-long VIX exposure for the first time since January 2019

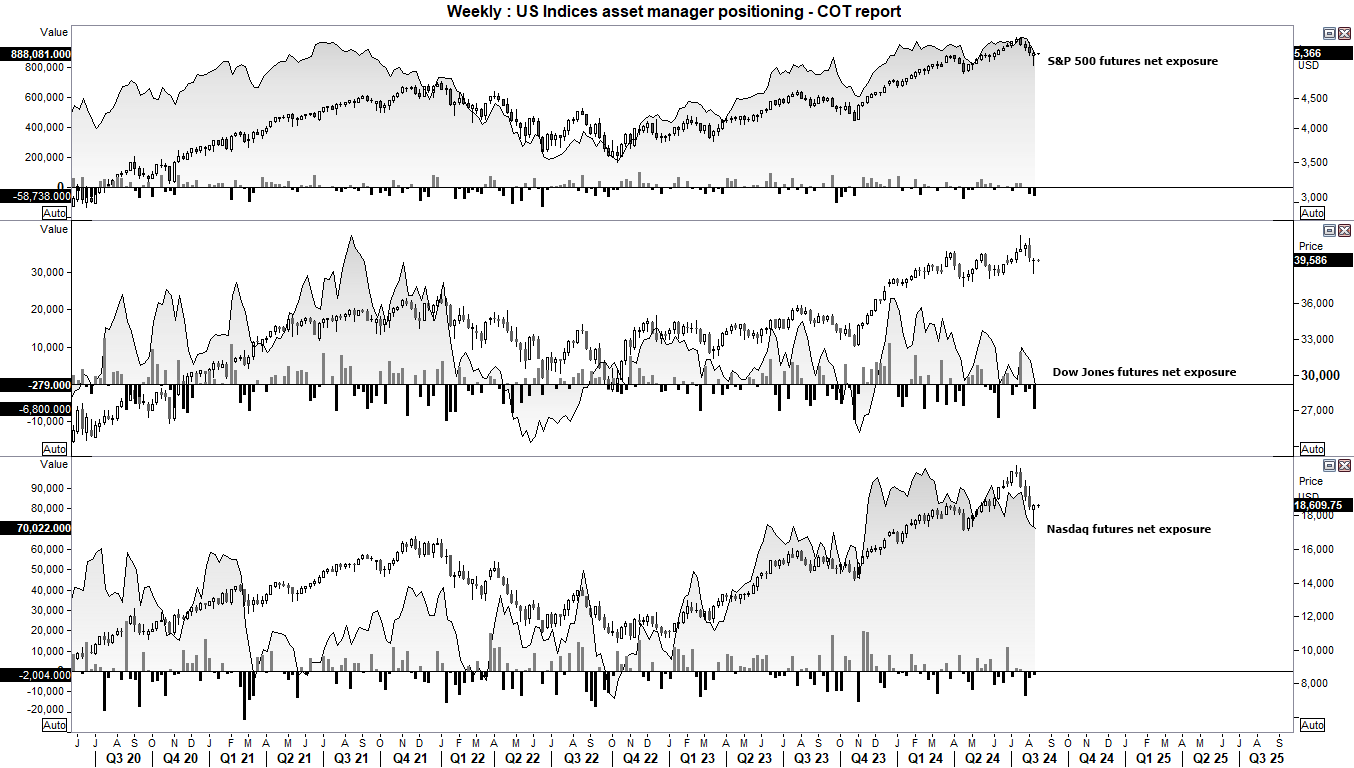

- They also flipped to net-short exposure to Dow Jones futures, increasing gross shorts by 22% (2.9k contracts) and reducing longs by -19.4% (-3.8k contracts)

- Traders clearly sought safe-haven currencies, increasing gross-long exposure to Swiss franc futures by 37% (2k contracts)

- Large specs were on the cusp of flipping to net-long yen exposure after gross-short exposure plunged by -44% (-61k contracts)

- Large speculators lightened their exposure to commodity currencies AUD, CAD and NZD – reducing both longs and shorts

- They also increased gross-short exposure to WTI crude oil futures by 19% (21k contracts)

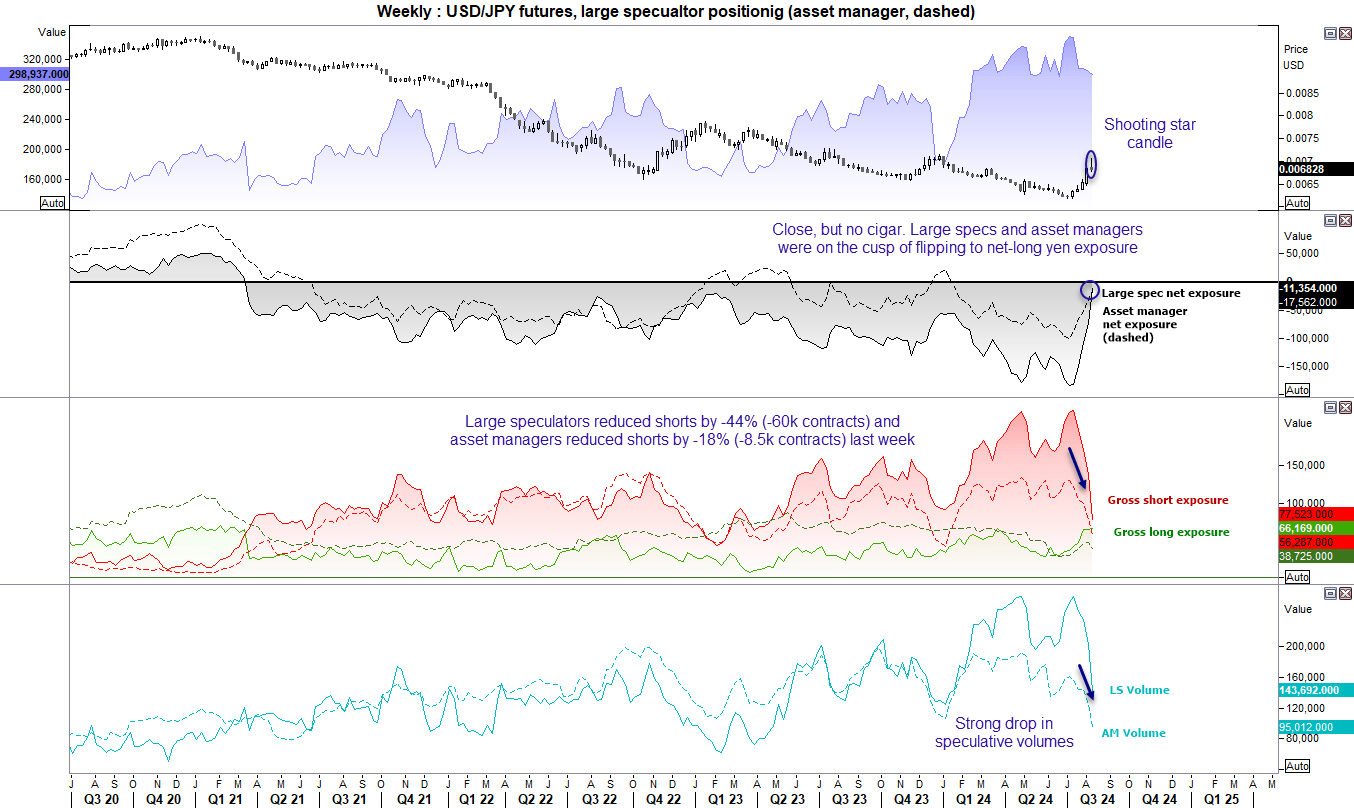

JPY/USD (Japanese yen futures) positioning – COT report:

I was expecting to see that traders had flipped to net-long exposure to yen futures in this COT report. While that did not happen, it was close. Large speculators reduced net-short exposure by -62k contracts, their most aggressive bear-culling week since March 2011. Gross shorts plunged by -44% (-61k contracts) which was the most aggressive short squeeze in 18 years.

Large speculators are now net short by a mere -11k contracts and asset managers by -17.6k contracts. But with the BOJ changing tact last week and deciding they don’t actually want a weak currency at all, I suspect the yen could have another spell of weakness. And that means traders may remain net short for a while longer until hawkish comments from the BOJ return.

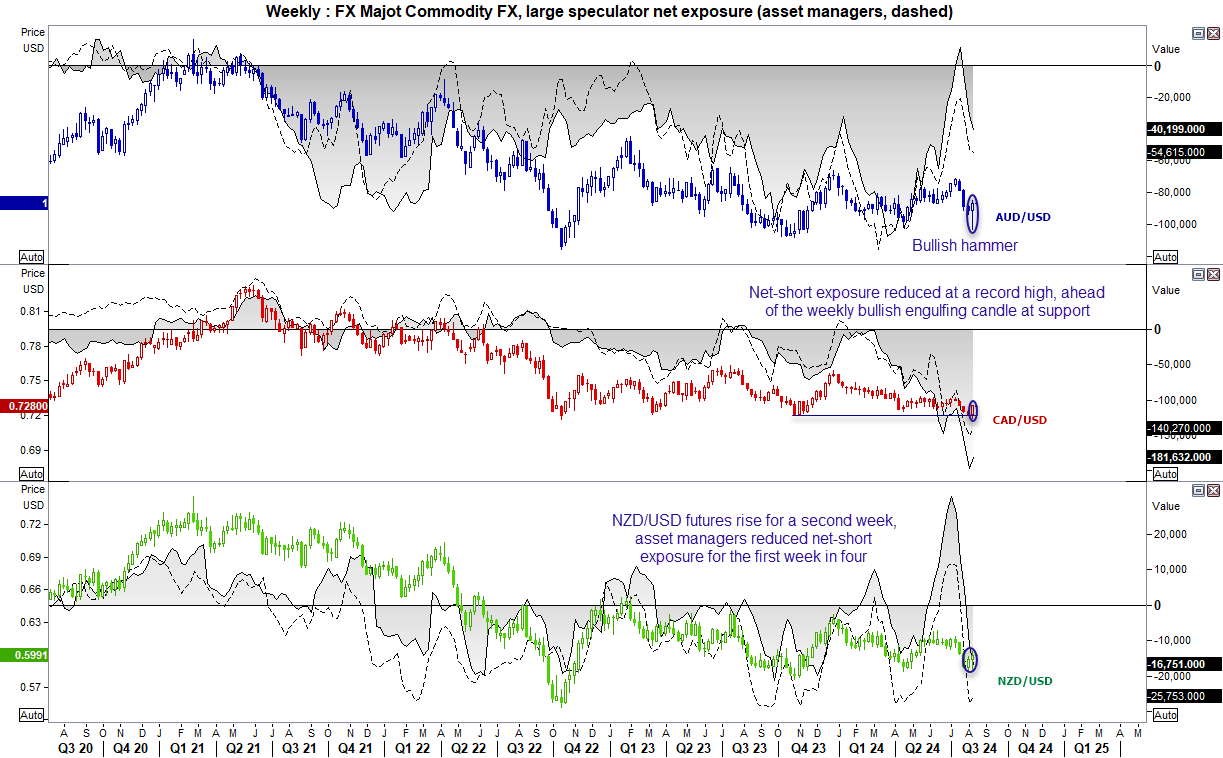

Commodity FX (AUD, CAD, NZD) – COT report:

There are a few clues across commodity currencies that the worst of the selling pressure could be behind us. While net-short exposure to AUD/USD futures increased for a third week among large specs and asset managers, it was the smallest increase of the three weeks. The latest COT data does not capture gains between Wednesday and Friday – and ignores the bullish weekly pinbar.

Net-short exposure for CAD futures also fell from a record high among both sets of traders. And given CAD futures formed a bullish engulfing week following a false break of key support and NZD/SUD futures rose for a second week, the downside move appears stretched for the commodity pairs.

Also take note that the RBNZ are expected to cut interest rates by 25bp this week. And if that is not backed up with a dovish bias (to hint at further cuts) then we could see some further upside potential for the New Zealand dollar.

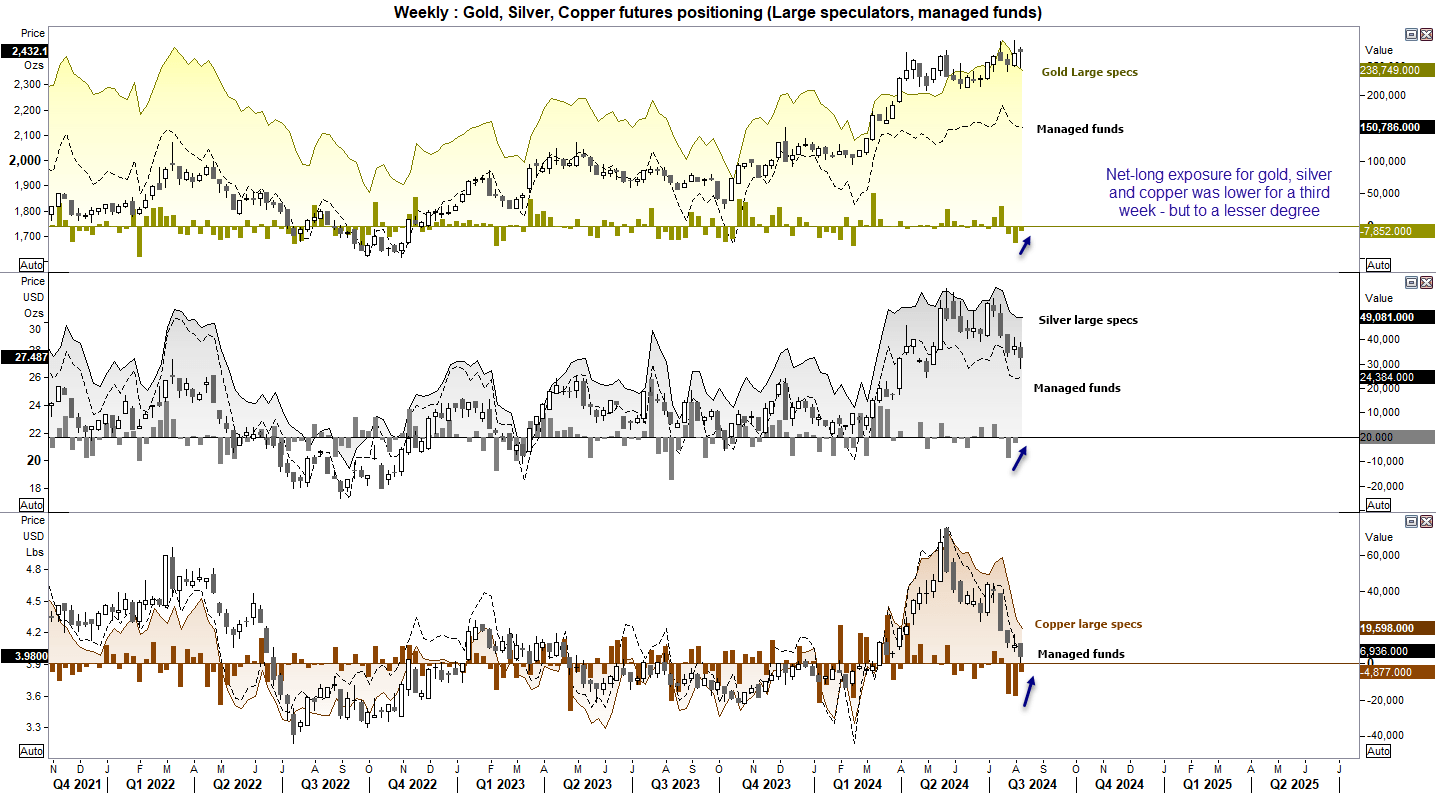

Metals positioning (gold, silver, copper) – COT report

Another clue that the commodity selloff could be in for a pause, if not a bounce, can be seen on metals. Net-long exposure for gold, silver and copper rose for a third week, but like AUD/USD the rise was the lowest in three.

With the exception of managed funds flipping to net-short exposure to copper, traders remained net-long to all three metals. Gold remains the most supported and recouped most of the week’s earlier losses by Friday. Reports that China is supporting copper helped hold coper futures above $4 for a period, although it now trades beneath it. But I suspect swing lows are close to forming on silver and copper looking at price action.

S&P 500, Dow Jones, Nasdaq 100 futures positioning – COT report:

Asset managers flipped to net-short exposure to Dow Jones futures for the first time this year, in a another sign that the Trump trade is dead. Net-long exposure to Nasdaq futures fell for a third week, and was lower for a second week on S&P 500 futures. Yet asset managers remain defiantly long on these markets in the grand scheme of things, which for now at least points towards recent losses being a retracement over the beginning of a bear market.

VIX (Volatility Index) positioning – COT report:

On Monday we saw VIX futures rise to the highest level since the pandemic, during its most bullish single-day rally on record. This saw asset managers flip to net-long exposure for the first time since May. But the subsequent price reversal and shooting star candle saw the VIX close lower for the week, which likely means asset managers are net-short once more. Ultimately, this backs up the view that Wall Street is in a correction given the bullish weekly hammer on the S&P 500 futures chart, assuming incoming data and Fed narrative continue to support the ‘soft landing’ narrative.

Take note that US CPI and retail figures are key reports which can sway sentiment either way this week.

Latest market news

Yesterday 07:55 PM

Yesterday 05:50 PM

Yesterday 05:30 PM

Yesterday 05:06 PM

Latest articles

December 16, 2024 05:06 AM

December 9, 2024 06:04 AM

December 2, 2024 05:42 AM