- S&P 500 outlook: What’s driving the markets?

- Could corporate earnings help lift sentiment?

- Key data to watch this week include US retail sales and Chinese GDP

- S&P 500 technical analysis: Lower lows still in place despite recent recovery

US index futures retreated along with European indices in the first half of Tuesday’s session. Once again, the bulls were unable to charge higher, after global indices rose on Monday. While there is a chance we could still see the markets climb higher once US investors come to the fray, even then, I am not so sure we will see a long-lasting rally. As far as I am concerned, there is nothing fundamental to help change investors’ risk appetite materially. So, I wouldn’t be surprised if markets resumed lower again. We have seen this sort of price action quite consistently ever since markets topped in July. And it makes total sense.

S&P 500 outlook: What’s driving the markets?

Understandably, not many people are in the mood to put their hard-earned cash at risk in these uncertain economic times. With interest rates being at their highest levels since before the financial crisis, and the full economic impact of those hikes not fully filtered through the economy yet, many investors are wondering what lies ahead in the months to come. Granted, there are signs that inflation and interest rates have peaked, and that looser monetary policy should follow. But we just don’t know how long inflation is going to remain elevated, which in turn raises question marks about the longevity of high interest rates. Judging by recent data in the US, oil prices and Fed commentary, it can be a long time before the Fed starts cutting rates again. That’s before we even put into equation the recent flare up in the Middle East crisis, a situation which could further fuel the oil rally and pressure risk assets.

Could corporate earnings help lift sentiment?

Following last week’s better-than-expected results from US banks, we saw shares of Bank of America advanced around 1% in premarket after its net interest income came in ahead of estimates. Goldman Sachs’ profit was hit by a write-down on its GreenSky fintech business and its investments in real estate, causing its shares to slip slightly in premarket. Morgan Stanley is set to report its earnings on Wednesday. Meanwhile, Johnson & Johnson shares rose after it raised its revenue outlook.

Here are the key results in case you missed it:

BAC

- Rev: $25.2B vs $25.1B est.

- EPS: $0.90 vs $0.83 est.

GS

- Rev: $11.82B vs $11.21B est.

- EPS: $5.47 vs $5.54 est.

JNJ

- Rev: $21.4B vs $21B est.

- EPS: $2.66 vs $2.51 est.

The focus will turn to technology earnings, with results from electric vehicle maker Tesla and streaming giant Netflix to kick things off this week on Wednesday, ahead of the other tech giants next week.

Key data to watch this week

This week, the economic calendar is a bit quieter, although we do have lots of FedSpeak to look forward to, including Fed Chair Powell who is due to speak on Thursday at the Economic Club of New York Luncheon. In terms of global data, the following are probably the most important macro pointers to watch this week:

US retail sales

Tuesday, October 17

Us retail sales have held up relatively well in recent months, despite borrowing costs continuing to rise and price pressures remaining elevated. Concerns over interest rates remaining high for longer in the US was intense in September, but not so much in October so far with equity markets staging a bit of a recovery. Can retail sales and industrial production data (that will be released on the same day) ignite those concerns again? However, it is likely that spending is likely to fall on non-essential items, potentially causing the economy to come to a standstill in the months ahead.

Chinese GDP

Wednesday, October 18

As well as GDP, we will have industrial production and retail sales data to look forward to from the world’s second largest economy on Wednesday. Concerns over China’s struggling economy has been a key theme for much of the year, which has held back the local stock markets and the yuan, as well as some commodity prices like copper. But will we start to see some signs of stabilization in data to arrest the underperformance of Chinese assets?

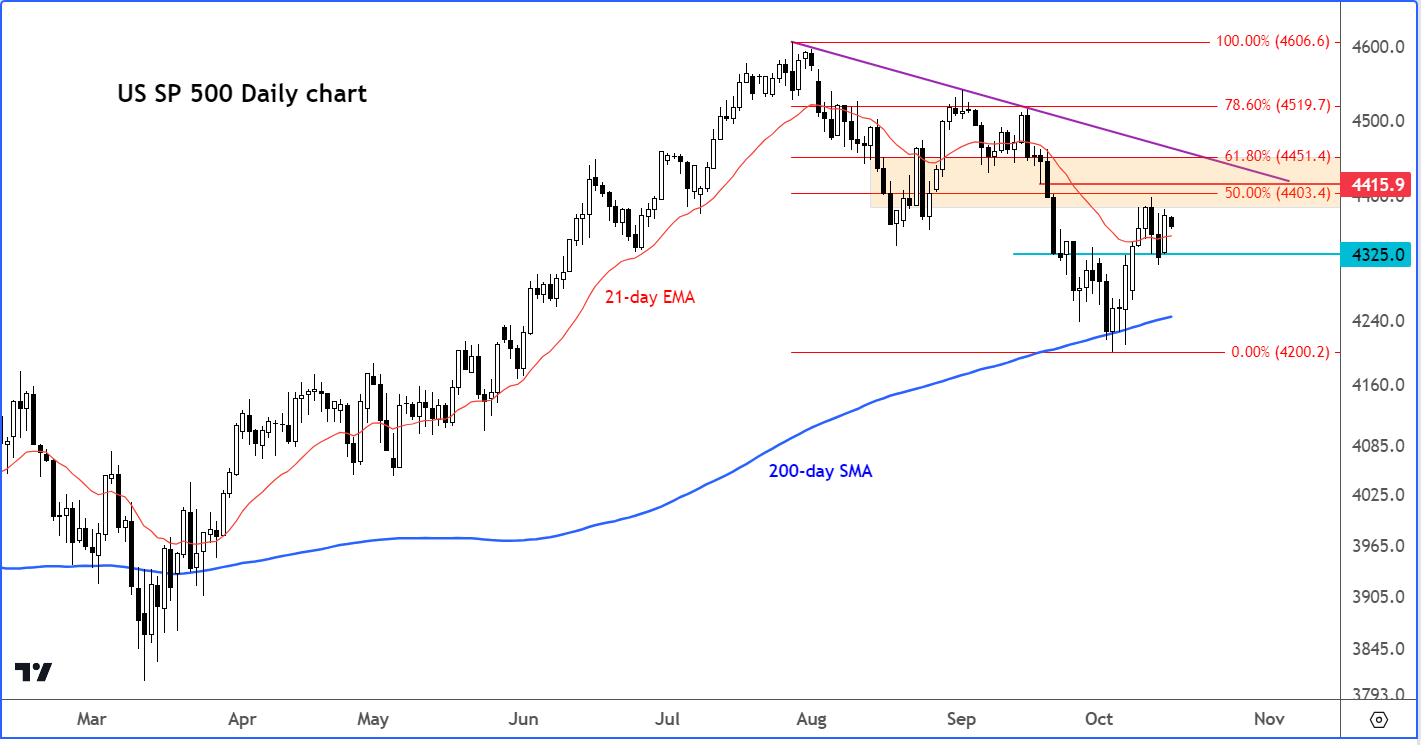

S&P 500 technical analysis

Overall, the bearish trend is still intact on the S&P 500 and many other global indices.

Source: TradingView.com

The US benchmark index has been making lower highs ever since peaking on July 27 at 4606. It has also made a couple of lower lows in the process. But the recent recovery from around the 200-day average and key long-term support at 4200 has complicated the technical picture. What’s more, the index has now formed an interim higher low around at 4310.

But while those lower lows are in place, and given the ongoing macro worries, raised geopolitical risks and still-high valuations (among many other risks), I would be on the look out for fresh bearish signals to emerge in the coming days.

Given that Monday’s low was formed around 4325, which is also were the index had bounced from on both directions in recent past, a closing break below this level could be that bearish trigger. Otherwise, the bears may wish to wait for an even larger recovery and an appropriate bearish signal, before looking for downside.

On the upside, there lots of technical levels that must be reclaimed before its bearish structure is removed. It is also worth keeping an eye on the bearish trend line that has been in pace since July. For me, that trend line is the line in the sand. While we are still below it, any short-term bullish signs should be taken with a pinch of salt.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Yesterday 11:57 PM

Yesterday 08:25 PM

Yesterday 07:48 PM

Yesterday 06:25 PM

Yesterday 05:30 PM

Latest articles

November 4, 2024 04:30 PM

November 3, 2024 08:00 AM

October 29, 2024 04:50 PM

October 27, 2024 08:00 AM