Lloyds shares recoup after final PPI hit

Last-minute PPI sting won’t be fatal for pay-out plans

As it was for Lloyds Banking Group’s main rivals, the tail of the PPI saga had a sharper sting than expected. Charges related to remediation costs for the two-decade long insurance mis-selling issue amounted to £1.80bn in Q3, against £1.67bn expected by analysts. The harsher than forecast hit partly reflects a last-minute gush of compensation claims that brought Lloyds' buyback plans to an abrupt halt in September.

The group is arguably the best-defended and best-positioned bank focused on the UK for revenues. Yet it is just as hemmed in by economic challenges as peers. Consequently, substantially accelerated growth remains a distant goal. Shareholders have thereby been more focused on capital growth and prospective returns to assess their investment in recent years. So even the hint of a risk to expected higher dividends and share buybacks can be a big deal, particularly with PPI impact also consuming profit targets for the year. (The trading statement didn’t update the bank’s view on its Return on Tangible Equity goal for 2019).

Still, such concerns have been reflected in contained fashion by share price moves in Lloyds stock on Thursday. It retreated by somewhat less than 3% at worst and curbed the loss to about 2% by late morning. Despite Q3 upsets, the buffer of capital Lloyds is obliged to hold as a ratio of total assets improved by a satisfactory extent in Q3. Common Equity Tier 1 Capital stood at 13.5% by quarter end, “in line with the board’s target”. As such, management emits no change to dividend plans and “will give due consideration to the return of any surplus capital at the year end.” Meanwhile, “never say never”, the advice on PPI offered by Lloyds’ previous CEO, remains wise, though post-deadline, claim volumes will continue to decline.

Q3 2019 is yet another quarter Lloyds investors would prefer to forget and that’s reflected in a ten percentage-point share price drop over the last ten days. Still, a firm net interest margin emerged as one of the few high points of the quarter at 2.88% vs. 2.87% expected. Cost control also remained in hand. Lloyds is not compounding past mistakes with new missteps.

Chart points

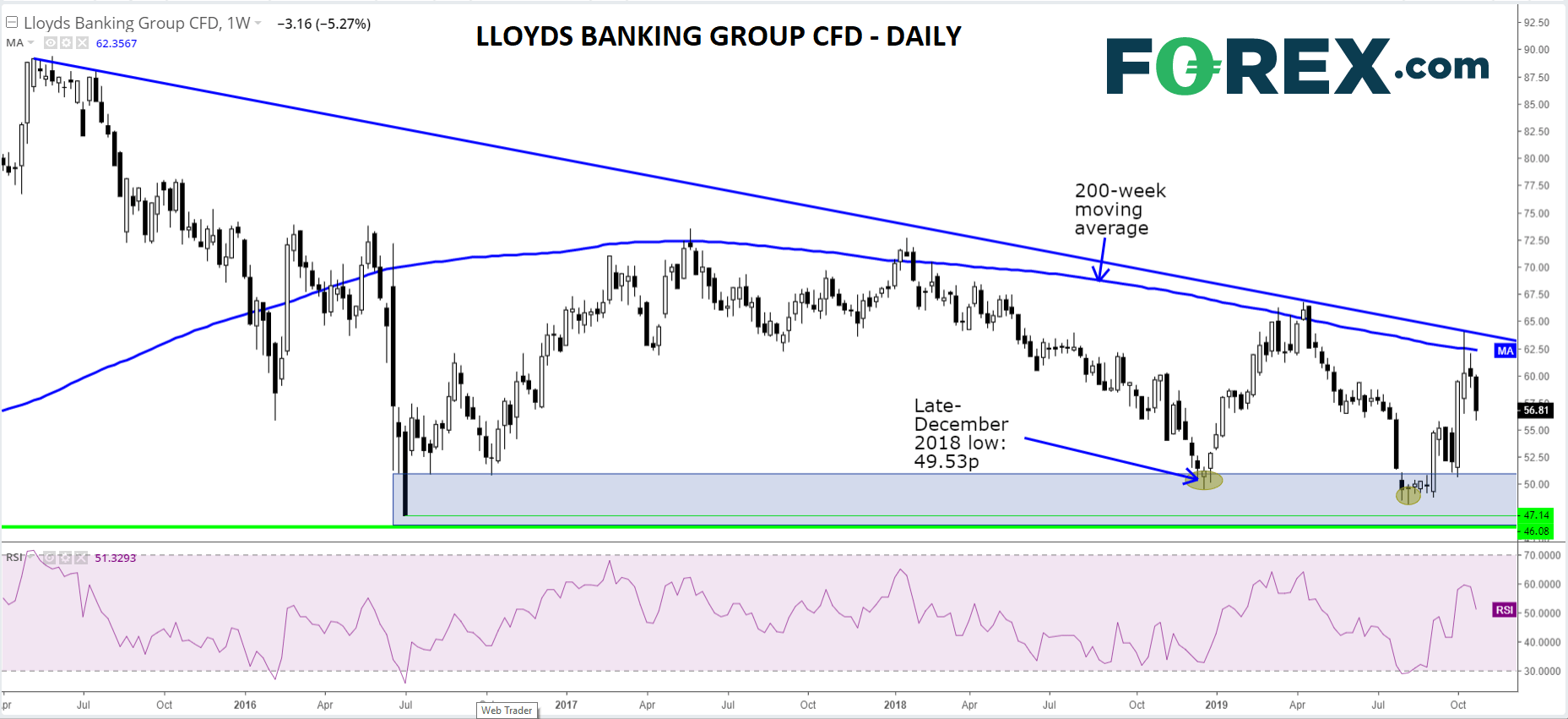

Over-arching pressure on the shares that could erode more of LLOY’s remaining 9% rise this year should continue, according to technical analysis. The decline since May 2015 is now well established: see the well-corroborated falling trend line since then that was last tagged in mid-October. The 200-week moving average reinforces trend line resistance given that mid-October also featured another failed attempt to get above the 200-WMA, the latest of many rejections in recent years. So long as overhead structures remain intact, objectives will continue to point towards December 2018’s base at 49.53p, and 2019’s 48.2p low from August. These floors are in within reasonable range of June 2016’s post-referendum lows as deep as 46p.

Lloyds Banking Group Plc. CFD – Weekly

{kind=link}

Source: FOREX.com

The information on this web site is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement. The information and opinions in this report are for general information use only and are not intended as an offer or solicitation with respect to the purchase or sale of any currency or CFD contract. All opinions and information contained in this report are subject to change without notice. This report has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. Any references to historical price movements or levels is informational based on our analysis and we do not represent or warranty that any such movements or levels are likely to reoccur in the future. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness, nor does author assume any liability for any direct, indirect or consequential loss that may result from the reliance by any person upon any such information or opinions.

Futures, Options on Futures, Foreign Exchange and other leveraged products involves significant risk of loss and is not suitable for all investors. Losses can exceed your deposits. Increasing leverage increases risk. Spot Gold and Silver contracts are not subject to regulation under the U.S. Commodity Exchange Act. Contracts for Difference (CFDs) are not available for US residents. Before deciding to trade forex, commodity futures, or digital assets, you should carefully consider your financial objectives, level of experience and risk appetite. Any opinions, news, research, analyses, prices or other information contained herein is intended as general information about the subject matter covered and is provided with the understanding that we do not provide any investment, legal, or tax advice. You should consult with appropriate counsel or other advisors on all investment, legal, or tax matters. References to FOREX.com or GAIN Capital refer to StoneX Group Inc. and its subsidiaries. Please read Characteristics and Risks of Standardized Options.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Contracts for Difference (CFDs) are not available to US residents.

FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited, 30 Independence Blvd, Suite 300 (3rd floor), Warren, NJ 07059, USA is a member of the Canadian Investment Regulatory Organization and Member of the Canadian Investor Protection Fund. GAIN Capital – FOREX.com Canada Limited is a wholly-owned subsidiary of Stonex Group Inc.

Complaints are taken very seriously at FOREX.com. You can view our complaints procedure here.

© FOREX.COM 2025