Lloyds flags uncertainty for outlook warning

A last-minute surge of PPI costs damped the quarter but that is the least of the bank’s worries

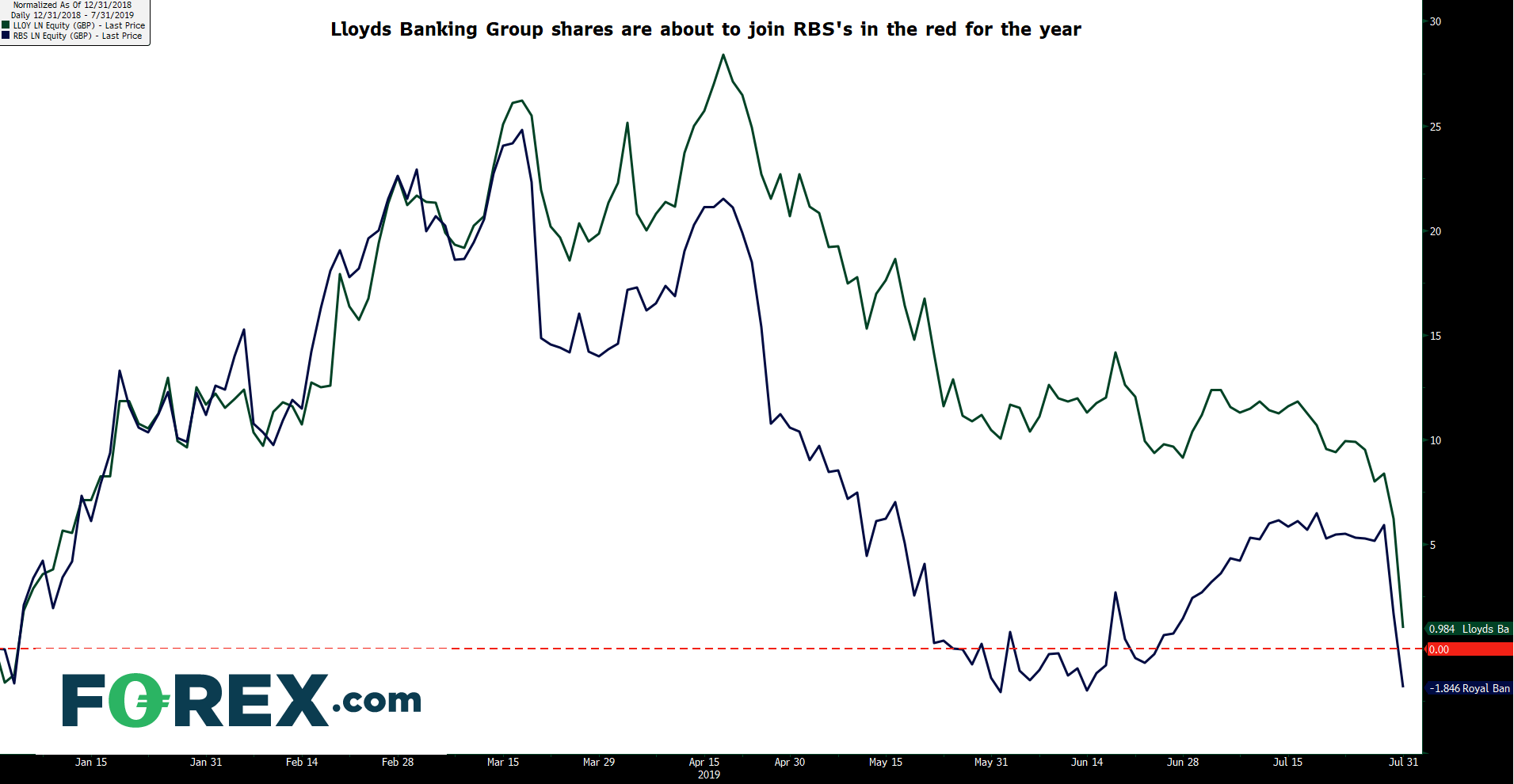

It’s difficult to see how Lloyds Banking Group could have performed more robustly given the specific challenges of the quarter. Looked at this way, perhaps the accelerated downturn of its shares on Wednesday is not entirely justified. The bigger picture helps explain why investor confidence continues to ebb. At last check, the shares had trimmed 4% more off a 2019 advance that stood almost 30% higher at mid-April. Now, they’re barely up 2% for the year and looking likely to turn negative.

The bank points to a fresh charge of £500m linked to payment protection insurance (PPI) as primarily responsible for missed second-quarter expectations.

The key misses

- Statutory pre-tax profit: £1.294bn vs. £1.76bn estimate

- 2Q net interest income: £3.06bn vs. £3.16bn consensus

- 2Q underlying profit: £2.03bn, below company-compiled £2.05bn consensus

- 2Q net interest margin: 2.89% vs. 2.94% estimate

Bloomberg consensus unless specified

But beyond the headline misses, the outlook weighs more. Hopes were pinned on the possibility that rising efficiency and lower regulatory and business capital needs, could enable swifter dividends rises and share buybacks. The interim dividend rose 5% to 1.12 pence; in line with expectations, which is exactly the point.

“Below the line charges”, including the last-minute wave of PPI costs have scuppered those hopes for now. Lloyds’ boast of sufficient capital for growth, regulatory requirements, uncertainty and a ‘management buffer’, have come a cropper as it now expects 2019 leeway to be at the lower end of a 170-200 basis point range. It implies that’s the reason why it’s holding back from a nearer term increase of capital returns. A fairly solid first-half despite misses adds a random variable.

- Total costs fell a more than forecast 5%, operating costs -3%

- Cost: income ratio on course for low 40% levels by end-2020, better than comparable rivals

- The wealth management push is bearing early fruit whilst insurance is stable

“Continued economic uncertainty could impact” the outlook as clarified on Wednesday, the bank says. Despite economic “resilience” it is nodding to Brexit risks for a decision to hang fire on pay-outs, perhaps for even longer than the first quarter of 2020.

More broadly, if the first half was sobering for Lloyds investors, it should be more worrying for RBS holders. They will find out how that bank fared in the first half on Friday. RBS faces a sharper delta from declining economic confidence and is the runner-up in Britain’s mortgage market. The stock was down 3% at time of writing and is slightly weaker for the year than Lloyds’. On the basis of results from its bigger rival, it’s set to continue leading the downside.

Normalised: Lloyds Banking Group, RBS – year-to-date [31/07/2019 13:14:42]

{kind=link}

Source: Bloomberg/FOREX.com

The information on this web site is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement. The information and opinions in this report are for general information use only and are not intended as an offer or solicitation with respect to the purchase or sale of any currency or CFD contract. All opinions and information contained in this report are subject to change without notice. This report has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. Any references to historical price movements or levels is informational based on our analysis and we do not represent or warranty that any such movements or levels are likely to reoccur in the future. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness, nor does author assume any liability for any direct, indirect or consequential loss that may result from the reliance by any person upon any such information or opinions.

Futures, Options on Futures, Foreign Exchange and other leveraged products involves significant risk of loss and is not suitable for all investors. Losses can exceed your deposits. Increasing leverage increases risk. Spot Gold and Silver contracts are not subject to regulation under the U.S. Commodity Exchange Act. Contracts for Difference (CFDs) are not available for US residents. Before deciding to trade forex, commodity futures, or digital assets, you should carefully consider your financial objectives, level of experience and risk appetite. Any opinions, news, research, analyses, prices or other information contained herein is intended as general information about the subject matter covered and is provided with the understanding that we do not provide any investment, legal, or tax advice. You should consult with appropriate counsel or other advisors on all investment, legal, or tax matters. References to FOREX.com or GAIN Capital refer to StoneX Group Inc. and its subsidiaries. Please read Characteristics and Risks of Standardized Options.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Contracts for Difference (CFDs) are not available to US residents.

FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited, 30 Independence Blvd, Suite 300 (3rd floor), Warren, NJ 07059, USA is a member of the Canadian Investment Regulatory Organization and Member of the Canadian Investor Protection Fund. GAIN Capital – FOREX.com Canada Limited is a wholly-owned subsidiary of Stonex Group Inc.

Complaints are taken very seriously at FOREX.com. You can view our complaints procedure here.

© FOREX.COM 2025