Japanese Yen, USD/JPY Talking Points:

- USD/JPY is pushing towards its first test of the 150 handle since the sell-off in early-August.

- Another 150 test was probably unthinkable just a month ago, when USD/JPY was testing below the 140.00 handle. But notably, there was a building case of divergence to go along with a falling wedge and so far in Q4 USD bulls have been able to push a strong move, allowing further recovery in the pair.

- I look into USD/JPY every Tuesday in the webinar. Click here for registration information.

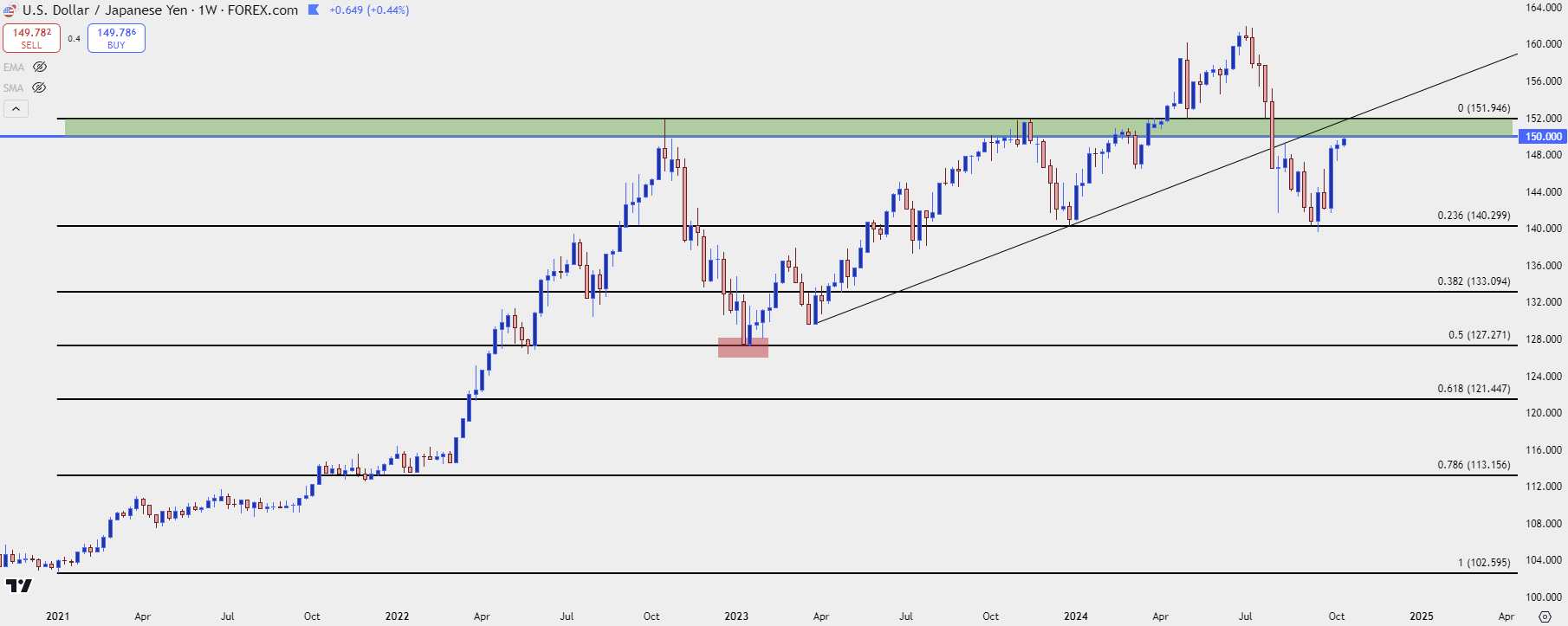

Shortly after the weekly open sellers came in to defend the 150.00 handle on USD/JPY. And, at this point, the two-month-high in the pair is just 1.8 pips inside of that level, which has some important history in USD/JPY price action.

That was the price that forced the MoF and in-turn the BoJ to spring to action in Q4 of 2022. At the time, the carry trade was in full bloom, and the Fed had just started to ramp down rate hikes from the 75 bp clips that had started in June. Inflation was still elevated, but there were early signs of moderation. Nonetheless the fear at the Ministry of Finance was that a bleeding JPY would soon invite inflation into their own economy, so on the morning October 21st they ordered the Bank of Japan to act, by buying Yen and selling USD.

That created a forceful move that, eventually, pushed down for a support test at the 145.00 handle. But it wasn’t until the below-expected US CPI print on November the 10th that sellers started to take over, eliciting a massive sell-off in the pair that, eventually saw 50% wiped out of the 2021-2022 major move. Perhaps more impressively is the fact that the carry trade trend took 21 months to build but only three months to erase half. But the scene of the sell-off started at that 150.00 juncture with the ultimate high on the morning of 10/21 printing at 151.95.

There’s a couple of lessons from that episodes that can remain important to keep in mind. The first is that intervention itself isn’t necessarily a trend reversal driver. It can help, but like we saw back in October of last year, it was merely enough to push bulls on their back foot. The other and perhaps more pertinent to current matters, is the fact that fundamentals are not a directly-perfect push-point for price. Sure, fundamentals can impact buyer and seller behavior or, said otherwise, supply and demand.

But if you have a crowded trade where almost anybody that wants or can be long already is, well, the unwind of that setup can be aggressive and forceful. And to be sure, rate divergence remained decisively-tilted to the long side of the pair for the entire three months of the sell-off. And this at least part of the reason why bulls soon returned at the 50% retracement of that prior trend to hold the lows, forcing the pair back up to that same 150 zone over the next nine months. The carry remained positive and after a brisk sell-off saw a host of longs close positions and take profits, there was cash on the sidelines while the bullish trend started to show signs of life again.

USD/JPY Weekly Price Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

USD/JPY Carry Trade

The carry trade can be an incredibly impactful driver in FX pairs. With near daily rollover payments or debits, traders buying the high-yielder and selling the low-yielder can earn a rollover payment just for being long the pair.

If rates increase even more in that higher-yielding currency, so can the rollover payment, thereby incentivizing even more traders and investors to get long. This can create a very symbiotic backdrop where a trader can earn rollover while riding a bullish trend and this is what helps to explain that initial spike up to the 150.00 level, after USD/JPY limped into 2021 trade below the 103.00 level.

But, as noted above, that important lesson, fundamentals aren’t always a directly perfect push point for price. And when you have an elongated trend of that nature, there’s a one-sided position that’s built in the marketplace, and this brings on the old analogy that if you’re in a crowded theater and you start to smell smoke, and the exit door is only so wide – are you really going to sit around and wait?

Well, when we have those crowded, one-sided trades, even when pushed by a logical fundamental backdrop, even a subtle hint or whiff of change can elicit counter-trend move.

The Bank of Japan intervention was enough to push bulls away from the 150.00 level they had defended – but it was the below-expected US CPI print on November 10th that started to scare bulls; and this is what led to the precipitous fall in the pair.

But when support started to show in January the Fed was nowhere near rate cuts, and the Bank of Japan wasn’t talking about hikes, either. So that fundamental bias allowed for the trend to continue, all the way until the 150 level came back into play in late-October of that year.

At the time, bulls were rightfully cautious of another round of Yen-tervention. And prices held just inside of the same 151.95 level that had marked the high the year before. And this is when more subtle whiffs of change showed in the form of US CPI, this time, on November the 14th when it came out below expectations.

And, again, a crowded, one-sided trade unwound as bulls rushed for the exits. But this time, the retracement only ran for 23.6% of that prior trend and the move only lasted for about six weeks, with support holding at 140.30 at the end of last year.

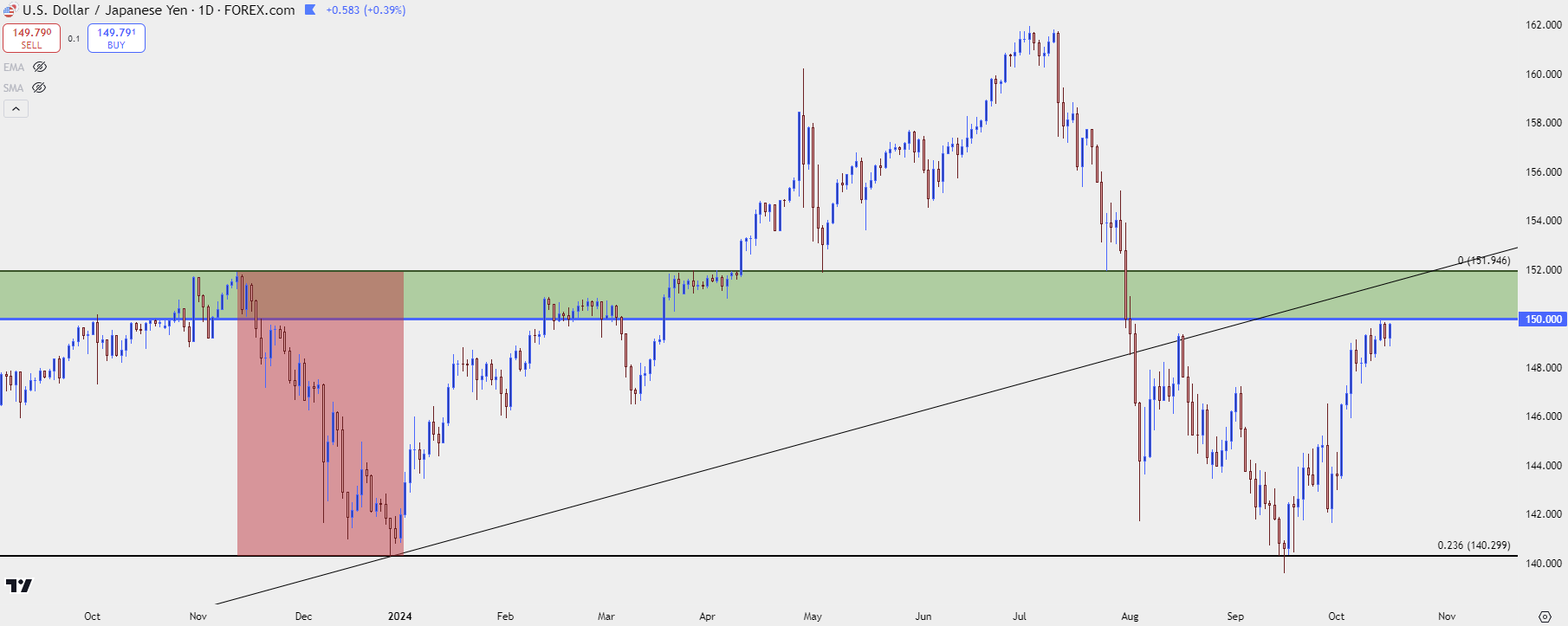

USD/JPY Daily Price Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

2024

The first half of 2024 was an interesting macro backdrop. US economic strength stayed relatively strong, particularly labor and core inflation. For the inflation data points, there were signs of entrenchment, which the Fed had previously said was a concern of slowing and the stopping rate hikes last year.

When there was an above expected US CPI print on April 10th, USD/JPY bulls finally found resolve to test the Bank of Japan again. And given the prior two episodes of clean resistance at the level, there were likely a host of stops. Stops on short positions are buy-to-cover logic, usually set up to execute ‘at best.’ This means that if that price gets hit a fresh influx of demand can come into the market, thereby propelling the breakout. It didn’t take long for USD/JPY to then jump up to the 160.00 handle after which the BoJ was ordered to step-in again.

But, just as we saw in 2022, intervention is not a panacea, and this could only elicit about a week’s worth of weakness until, eventually, the same 151.95 level came into play. This time, as support.

In May the question remained as to whether data would allow the Fed to cut; and rollover on the pair remained decisively tilted to the long side of USD/JPY. And, once again, bulls simply fired the trend back up to fresh highs, with a fresh multi-decade high printing through the Q3 open. And this around the time that matters began to shift…

USD/JPY Daily Price Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

The Sell-Off

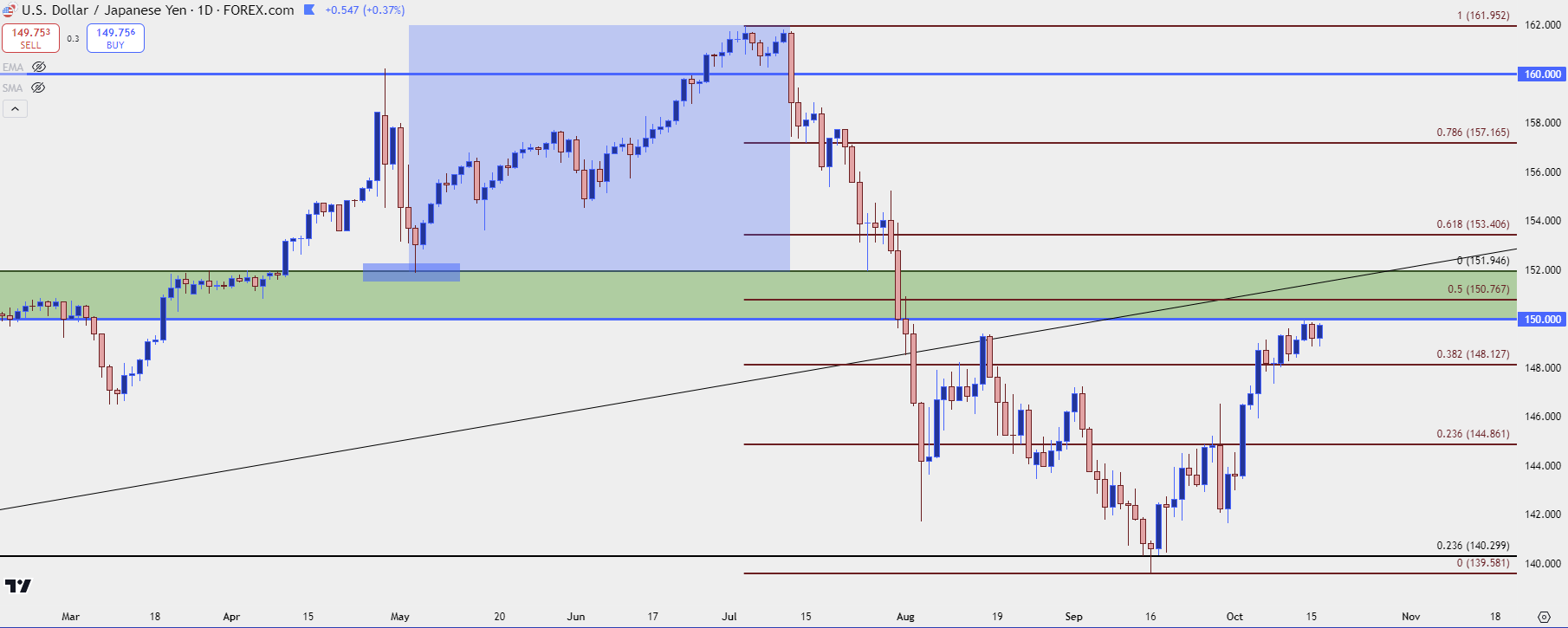

It was the morning of July 11th when it all went down and, really, there were a culmination of factors. To be sure the move was probably one-sided, like episodes in Q4 of each of the past two years. But that was also the morning of a US CPI print and finally, US inflation had seemed to cooperate with the Fed’s aims as the data printed below expectations. But combined with that was the fact that the Bank of Japan was standing by to try to take further advantage of the situation with yet another intervention.

And this time, it was different, as longs had reason to start smelling reacting to the smell of smoke that had built in the crowded trade. It started to seem as though the Fed would soon be cutting, thereby removing incentive from the long side of the carry trade, and as bulls rushed for the exits, bears piled-on, trying to get in-front of what felt like inevitable rate cuts from the FOMC. This drove a forceful push over the next few weeks, eventually entangling macro markets across-the-globe.

It didn’t take long for the media to start pointing fingers at the Bank of Japan as cause for the sell-off in US equities, claiming it was the unwind of the carry trade that had evaporated leverage from risk markets around the world.

While probably some of that was true, it seems unlikely that it was the sole cause of the sell-off. But nonetheless the damage in USD/JPY was undeniable as the pair dropped by more than 2,000 pips in less than two months.

And that’s when matters started to get really interesting.

USD/JPY Daily Price Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

The Stall

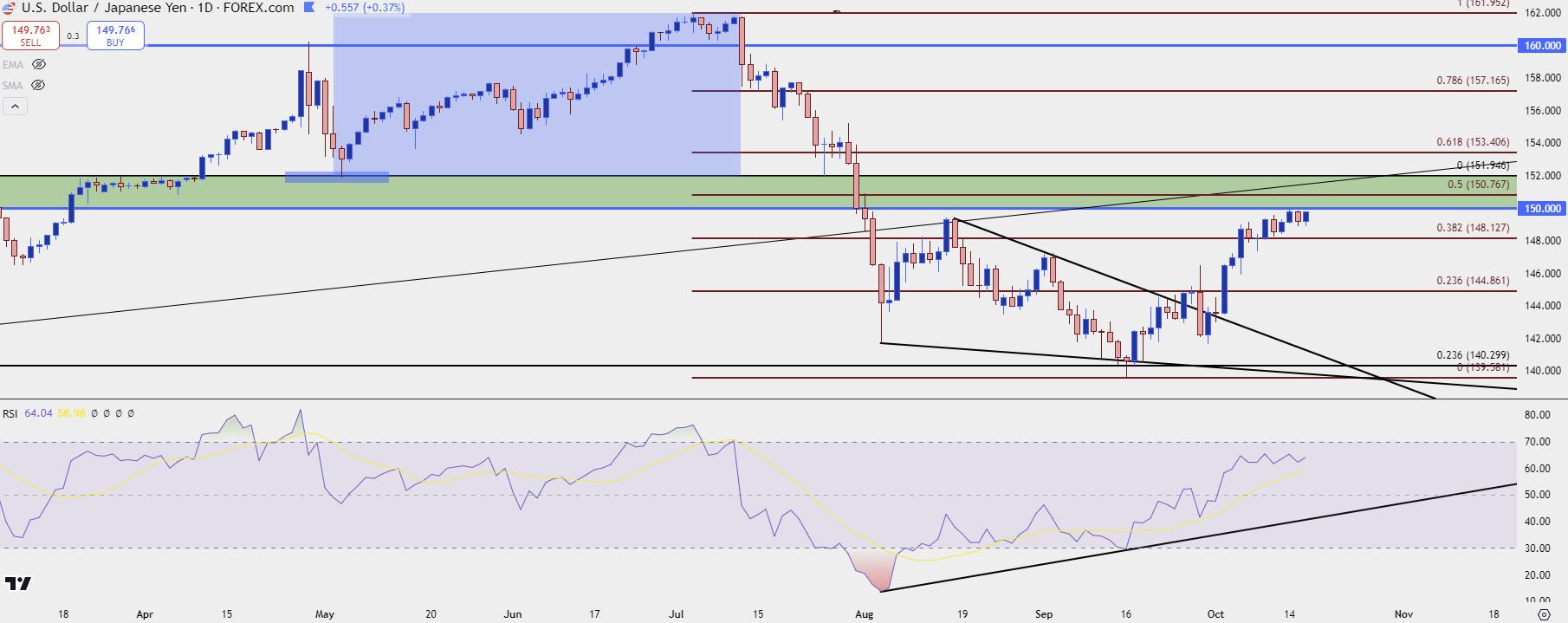

If there’s one thing that you take away from this article, I hope that it’s the realization that fundamentals nor technical are a perfectly direct push-point for price. The only thing that actually moves price in a true market environment is buying and selling, or supply and demand. Sure, fundamentals and technical can both induce that, to a degree; but, if everyone willing and able to sell already has, well, price will struggle to move lower.

And soon, even bad news will lead to higher prices and this will bring on the mirror image of the common deduction that if a market stops gaining on good news, look out below.

In my estimation that’s what happened in early-August. Longer-term carry traders that wanted to get out already had. Shorter-term speculators betting on faster and more rate cuts from the Fed had already piled into the trade. And this is why the move began to stall in August, despite the very clear and visible fear that had already permeated the backdrop.

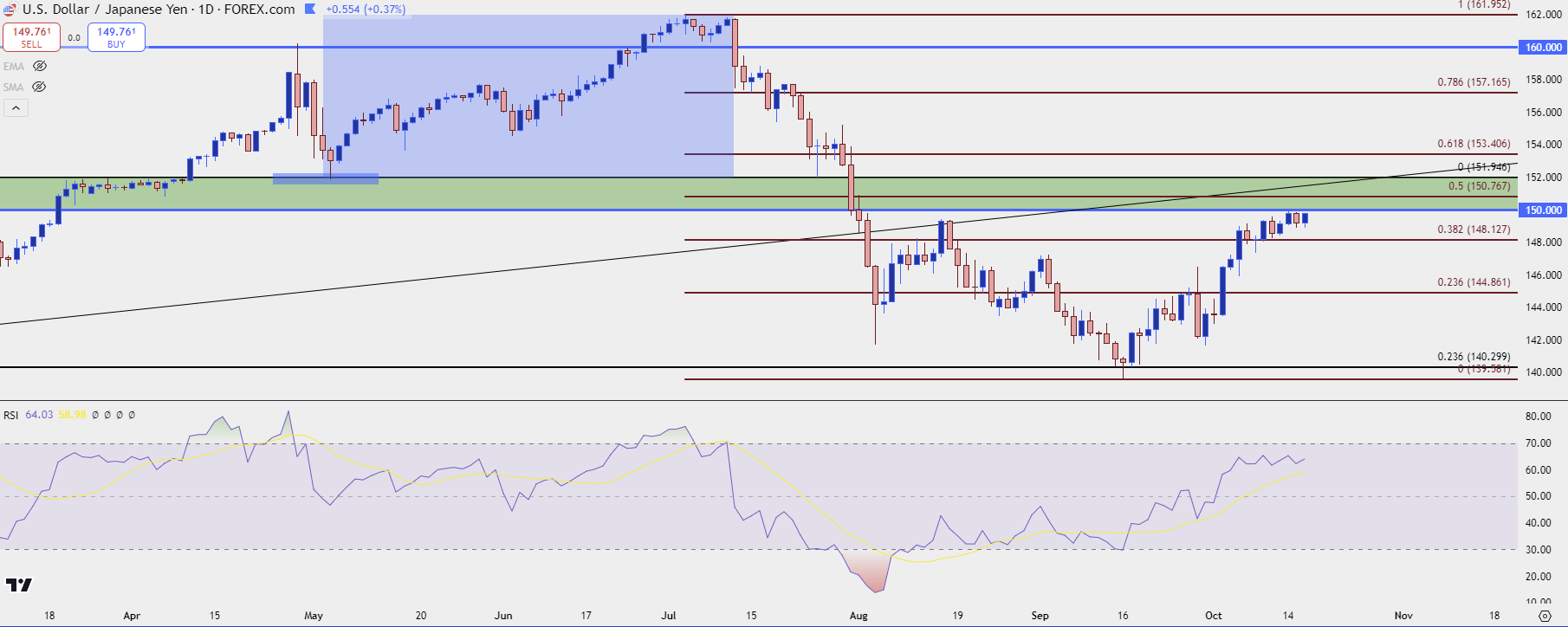

These matters take time, though. After a bounce, bears can fast get back to work and that’s what we saw in August as USD/JPY reacted harshly to resistance but was more tepid around support. This is what builds falling wedge formations, often approached with aim of bullish reversal and precisely what we’ve seen play out in the USD over the past few weeks.

There was also the building case of RSI divergence, where the lower-lows on price were showing higher-lows via RSI.

Sure, it wasn’t yet bullish as the downtrend remained. But it was a month ago as of today that sellers took a test below the 140.00 handle and failed to run with it.

And then, when the FOMC did actually cut rates – sellers again failed to run with the trend, setting a higher-low and holding above the same 140.30 level that set the low late last year. At that point, there was the initial making of a counter-trend rally and over the next few weeks, that set in.

USD/JPY Daily Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

Price Shapes Narrative

In my view, price shapes narrative, not the other way around. Headlines will often seek out whatever explanations they can muster to justify the moves that happened in a market but, as has hopefully been clear in this ever-expanding article, fundamentals aren’t always a directly perfect push-point for price.

And now that the pair is rushing higher, many are claiming that the carry trade is back. But given the wide expectation for the Fed to continue cutting into 2025 and combined with their persistence to do so this year, that doesn’t make a lot of sense, as the rationale on the long side of the carry seems as though it will be under further fire in the months and perhaps even years ahead.

So far, the 150.00 level has remained defended. It almost came into play after the weekly open and sellers quickly jumped in, leaving the high just 1.8 pips inside of the level. But, realistically, that entire zone spanning up to 151.95 represents and important decision point for USD/JPY.

For those that are holding carry trades on a longer-term basis, that represents an opportunity to get out with a minimum of damage.

And for those that are, or were holding short positions, the 50% mark of the sell-off is near the middle of that zone, at 150.77.

If one would like to speculate on the idea of US rate hikes, perhaps the long side of the pair can remain attractive through that resistance zone. But, as we’ve seen multiple times already in the past couple of years, the 150-151.95 zone is where matters can change very, very quickly.

So, buckle up for the next test because it appears as though that will be soon.

USD/JPY Four-Hour Price Chart

Chart prepared by James Stanley, USD/JPY on Tradingview

Chart prepared by James Stanley, USD/JPY on Tradingview

--- written by James Stanley, Senior Strategist

Latest market news

Today 12:30 PM

Today 09:44 AM

Today 09:34 AM

Yesterday 07:55 PM

Latest articles

Yesterday 05:06 PM

January 4, 2025 12:30 PM

January 3, 2025 03:50 PM