Giant techs face shrinking growth

Slowing global growth and hyper-spending in focus as U.S. technology giants report earnings

Warren front

New fronts have opened up in the second half of the year in the legal, regulatory and political threats facing vast U.S. tech firms. Chiefly, coordinated U.S. Department of Justice and the Federal Trade Commission examinations were announced in July. They are expected to take years to complete, though some negative early effects are possible, including a possible chill on M&A. Meanwhile, Senator Elizabeth Warren has stepped up calls for the break-up of large consumer technology groups, including Facebook, Google and Amazon.

Still outperforming…mostly

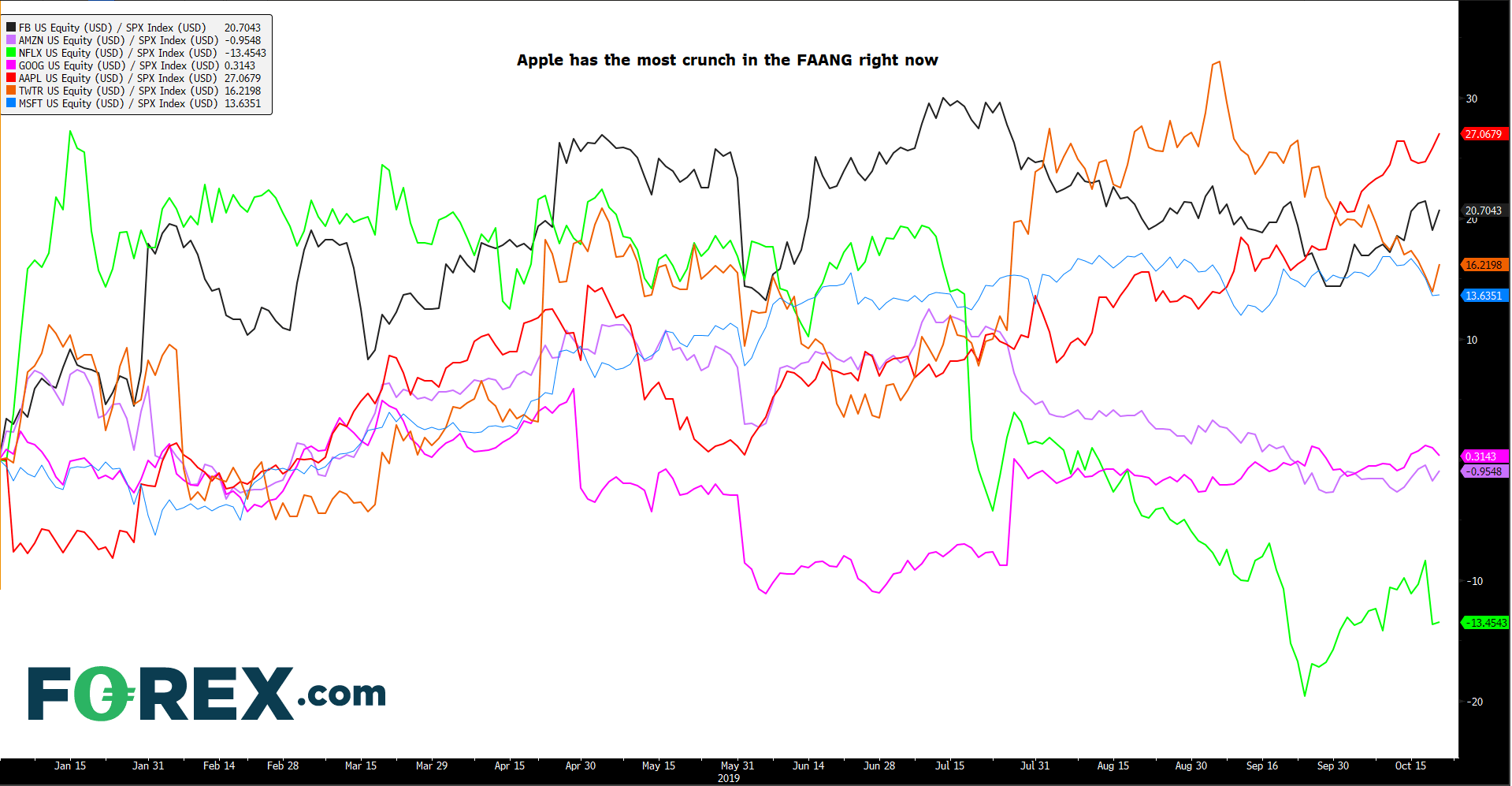

Yet whilst these headwinds have brought turbulence to FAANG stocks and beyond, they’ve failed to damp enthusiasm for leading web entities entirely. That’s partly due to how long such pressures will take to come to a head. The S&P 500’s Communication Services Index, which houses the best-known social networks, is up 23% this year, aided by a Facebook gain of 44% and 38% rise by Twitter. The gains put Amazon’s relatively modest 18% rise this year into context. Still, AMZN’s sluggish progress appears to have more to do with another phase of mega-investments than scrutiny or legal concerns.

Microsoft, Apple exempt

Elsewhere, the top-two global firms by market value, Apple and Microsoft, are relatively exempt from regulatory and antitrust issues impacting ‘younger’ titans. Yet all FAANG+ stocks have been dented by trade war and global slowdown anxieties. Generally, questions around growth are likely to be more in focus than regulation as mega-techs begin to report quarterly earnings this week. As ever, generalisations should be applied cautiously, though a plateau in world growth is partly reflected in modest or weaker earnings and sales forecasts for tech leaders. With the dollar hitting levels not seen since May 2017 at one point in the past quarter, investors will also be alert to any signs that slower growth outside of the U.S. is beginning to bite.

Microsoft Corp Q1 2020 earnings – 23rd October, after U.S. market close

The strength of its Azure cloud keeps MSFT’s outlook reaching for the skies. Furthermore, a deeply embedded installed base of productivity users means the group is better equipped to weather changing economic phases better than most peers. That said, cloud growth—which dominates investor attention— is called to slow over the next 12 months as the market matures. An average 74% rise at the Azure flagship over 4 quarters should moderate to the high 50%-60% levels, though that’s still twice the pace of the cloud services market. In turn, although the stock outpaces the Nasdaq 100 index this year with 30%-plus gains, moderating quarterly sales advances may bring headwinds for the shares into year end. Consensus adjusted EPS forecast: $1.24, +9.5%. Consensus revenue forecast: $32.21bn, +10.8%

Twitter Inc. Q3 2019 earnings – 24th October, before U.S. market open

Twitter downloads have shown healthy gains so far this year, despite the typical lag between numbers of potential new Tweeters relative to Facebook, Instagram and joiners of other rival apps. September downloads even topped tough comparable 2018 data. That points to continuation of a several-quarter trend of rising daily user engagement, underpinning advertiser confidence and consequently, revenue growth. Investments in ‘health’, clean-up and new engagement costs remain key headwinds. Consensus adjusted EPS forecast: $0.198, -5.7%. Consensus revenue forecast: $875.7m, +15.5%

Amazon Inc. Q3 2019 earnings – 24th October, after U.S. market close

Any update on how a slew of new hardware devices launched in recent weeks may draw attention, given that the prevalence of new Alexa-powered gadgets may drive higher-margin cloud revenues, though accelerating growth is a matter for the longer-term, rather than the prior quarter. For Q3, one-day free shipping remains a key watch: though launch costs have dragged prior quarterly results, Prime growth could now begin to stabilise group sales, whilst market-share gains and rising profit are probable benefits from third-party-seller growth and as AMZN’s advertising segment expands like wildfire. Still-demanding investment expenses are the main cautionary overhang. Consensus adjusted EPS forecast: $7.06, -10%. Consensus revenue forecast: $68.69bn, +21.4%

Alphabet Inc. Q3 2019 earnings – 28th October, after U.S. market close

Like Facebook, the Google owner faces multiple potential legal, regulatory and (for now) political headwinds. Little wonder then that although the shares have risen a respectable 20% in 2019, they’re well into laggard territory relative to FAANG counterparts. The nearest outperformer Twitter rises 13% above the S&P 500, year to date, whilst GOOG is about level with SPX.

Normalised: ‘FAANG’, Twitter, Microsoft relative to S&P 500 – year to date [21/10/2019 20:56:11]

{kind=link}

Source: Bloomberg/FOREX.com

Huawei concerns may feature in the stock, though the emerging consensus is that restricted business with the Chinese handset maker will have limited revenue impact. Furthermore, GOOG’s discount masks something of a comeback for the stock from two quarters over which Google’s advertising market share loss to Facebook, Amazon and others, began to crystallise. Steady end-market demand should abate concerns that followed the cliff-drop in paid clicks of Q1. Q3 should bring rebounding sales as year-to-year comparisons become less demanding. There’s a chance of recharged share price momentum if the group opts to disclose growth in YouTube or Maps. Expenses are in investors’ crosshairs, in case of overruns that marred recent quarters. Consensus adjusted EPS forecast: $14.59, +8%. Consensus revenue forecast: $32.72bn, +20.5%

Facebook Inc. Q3 2019 earnings – 30th October, after U.S. market close

If Alphabet is at the heart of growing regulatory threats that could eventually clip Big Tech’s wings, Facebook is at the epicentre. CEO Mark Zuckerberg is preparing for a second appearance before a House committee this week as probes into whether FB and others are using their dominance to thwart competition gather pace. A record $5bn fine to settle U.S. claims that it repeatedly violated users’ privacy buffeted the stock even after a strong Q2. Facebook also faces antitrust and privacy probes in Europe. But the shares have not appeared to care that much of late. They’ve eased from a 30% ascent relative to the S&P 500 between the start of 2019 to July, though remain 20% above the benchmark, year to date. Boosted advertising sales growth on the back of Facebook Stories, that buoyed Q2, should remain evident in Q3, despite softer guidance. Rising video adoption and better-managed pricing volatility pose upside risks to forecasts. Instagram (now including Instagram TV) monetisation of which is still being incubated, also supports valuation multiples regardless of quarterly outcomes. Libra dropouts and blow back are a headache, though quite immaterial for now. Consensus adjusted EPS forecast: $2.25, +8.6%. Consensus revenue forecast: $17.34bn, +26%

Apple Inc. Q4 2019 earnings – 30th October, after U.S. market close

Growth of Services, Services and more Services is continuing to eclipse sales growth of the group’s still-dominant revenue generator, iPhones. Still, the segment that includes Music, TV, App Store, Health, Pay and more will take a few more years to approach anything like the sales contributed by handsets. Yet the stock’s leading position in the relative performance of FAANG shares and beyond this year signals that investors are now fully aboard the story. As such, risks to the stock now include unforeseen headwinds that could throw services sales off course. The slowdown in China could yet have difficult to predict consequences. The recent discovery of iPhone demand elasticity to higher prices is already an awkward though inescapable happenstance that may be tied to plateauing China and U.S. growth. The lack of 5G in the latest handsets suggests total growth should be modest till that facility’s launch, scheduled for September 2020. Gross margin impact from recently tariffed Mac Pro, though modest, is a warning about more painful compression should the trade war escalate with Apple in the crossfire. Consensus adjusted EPS forecast: $2.18, -5.7%. Consensus revenue forecast: $53.81bn, +1%

The information on this web site is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement. The information and opinions in this report are for general information use only and are not intended as an offer or solicitation with respect to the purchase or sale of any currency or CFD contract. All opinions and information contained in this report are subject to change without notice. This report has been prepared without regard to the specific investment objectives, financial situation and needs of any particular recipient. Any references to historical price movements or levels is informational based on our analysis and we do not represent or warranty that any such movements or levels are likely to reoccur in the future. While the information contained herein was obtained from sources believed to be reliable, author does not guarantee its accuracy or completeness, nor does author assume any liability for any direct, indirect or consequential loss that may result from the reliance by any person upon any such information or opinions.

Futures, Options on Futures, Foreign Exchange and other leveraged products involves significant risk of loss and is not suitable for all investors. Losses can exceed your deposits. Increasing leverage increases risk. Spot Gold and Silver contracts are not subject to regulation under the U.S. Commodity Exchange Act. Contracts for Difference (CFDs) are not available for US residents. Before deciding to trade forex, commodity futures, or digital assets, you should carefully consider your financial objectives, level of experience and risk appetite. Any opinions, news, research, analyses, prices or other information contained herein is intended as general information about the subject matter covered and is provided with the understanding that we do not provide any investment, legal, or tax advice. You should consult with appropriate counsel or other advisors on all investment, legal, or tax matters. References to FOREX.com or GAIN Capital refer to StoneX Group Inc. and its subsidiaries. Please read Characteristics and Risks of Standardized Options.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Contracts for Difference (CFDs) are not available to US residents.

FOREX.com is a trading name of GAIN Capital - FOREX.com Canada Limited, 30 Independence Blvd, Suite 300 (3rd floor), Warren, NJ 07059, USA is a member of the Canadian Investment Regulatory Organization and Member of the Canadian Investor Protection Fund. GAIN Capital – FOREX.com Canada Limited is a wholly-owned subsidiary of Stonex Group Inc.

Complaints are taken very seriously at FOREX.com. You can view our complaints procedure here.

© FOREX.COM 2025