Flash PMIs are an investors favourite when it comes to economic indicators, as they can provide a forward look at GDP figures, alongside underlying trends within employment and inflationary figures. And that makes it an ideal tool for investors to place bets on future monetary policy action of a country or region’s respective central bank.

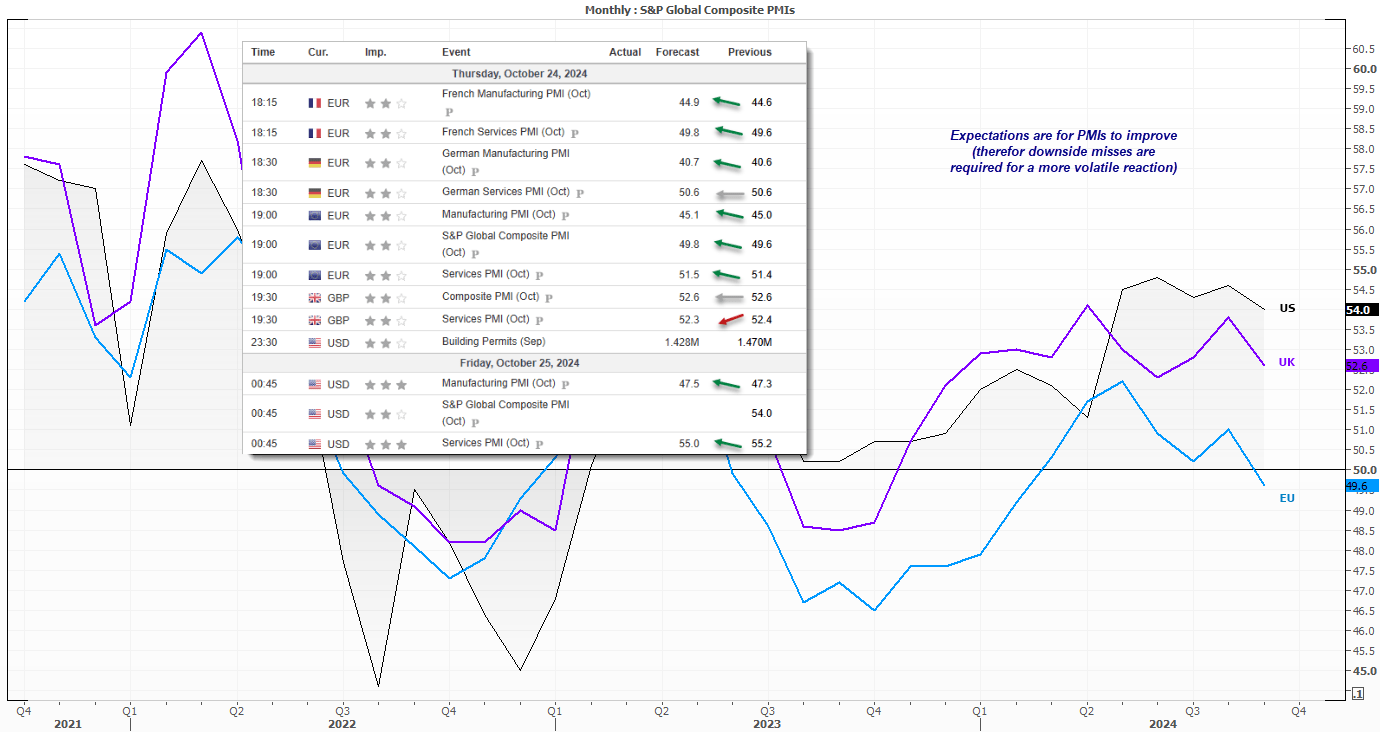

The table above shows the final composite data of the past 12 months for the US, Europe, Germany, France, Australia and Japan. All of which release reports today. We can see that the respective economies were contracting in Q4 2023 and potentially peaked around April to June this year. The fact that they are now all trending lower plays into the theme of central bank easing for the Fed, ECB and BOE.

The RBA is the exception as they’re cash rate remains relatively low, and employment and inflation remains too firm to justify cuts. It is therefore interesting to see that Australia’s composite PMI contracted at a slower pace and is in fact close to expansion (above 50).

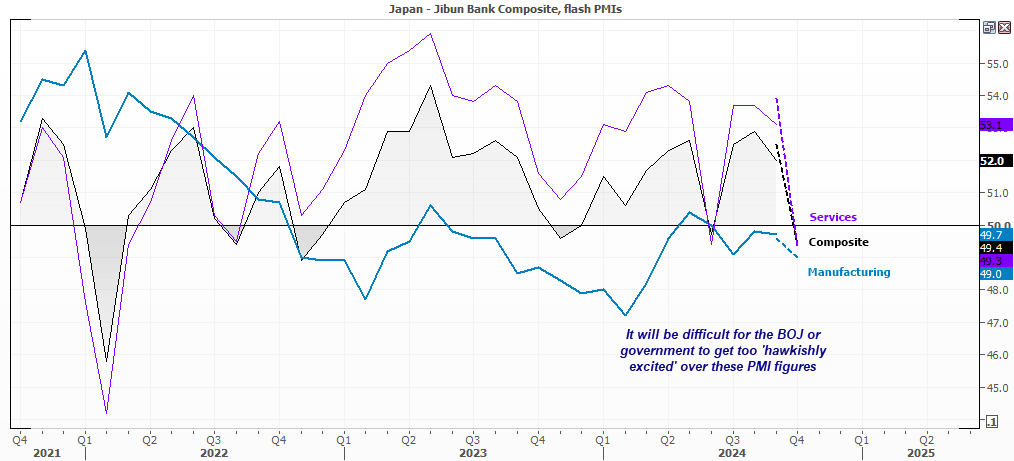

Japan’s data was weak overall, which once again makes it difficult to construct a hawkish case for the BOJ.

Australia’s economy shrank at a slower pace with a composite PMI reading of 49.8, (49.6 previously).

- Services PMI increased to a 2-month high of 50.6

- New orders increased, hiring rose at fastest pace in five months, price pressures eased

- Manufacturing PMI sank to a 53-month low of 46.7

- Weak demand for goods, employment, and purchasers were lower

Japan’s economy slipped back into contraction, with a composite PMI of 49.4.

- Services slipped below 50 to 49.3, down from 53.1 prior

- Manufacturing contracted at a faster pace of 49.5, compared with 49.7 prior

- New orders, employment and outlook for both sectors was weaker (faster contraction for manufacturing, slower gorwth for services)

- Input and output prices for services was stronger

Attention now shifts to Europe, the UK and US. In that order. While we can see that the economies of the three main regions has slowed, consensus estimates have pencilled in a slight improvement overall for manufacturing and services. That means downside misses may be required to spark the more volatile reaction (and appease doves).

- Take note that data from France and Germany can provide a lead for the Euro Area figures, and potentially weigh on the euro if they miss by a wide enough margin on bets of a more dovish ECB.

- GBP/USD traders will want to see broad weakness across services and manufacturing, but in particular a more bearish reaction for GBP could be expected if we see ‘prices paid’ soften notably to justify more BOE cuts

- Attention then shifts to the US for their latest set of PMI, which I suspect has the greatest chance of surprising to the upside given data has generally outperformed in recent weeks

- Currency traders will want to see a divergence between the data sets to spark larger moves (a weak EU or UK report coupled with a stronger-than-expected US report would likely be bearish for GBP/USD and EUR/USD, for example)

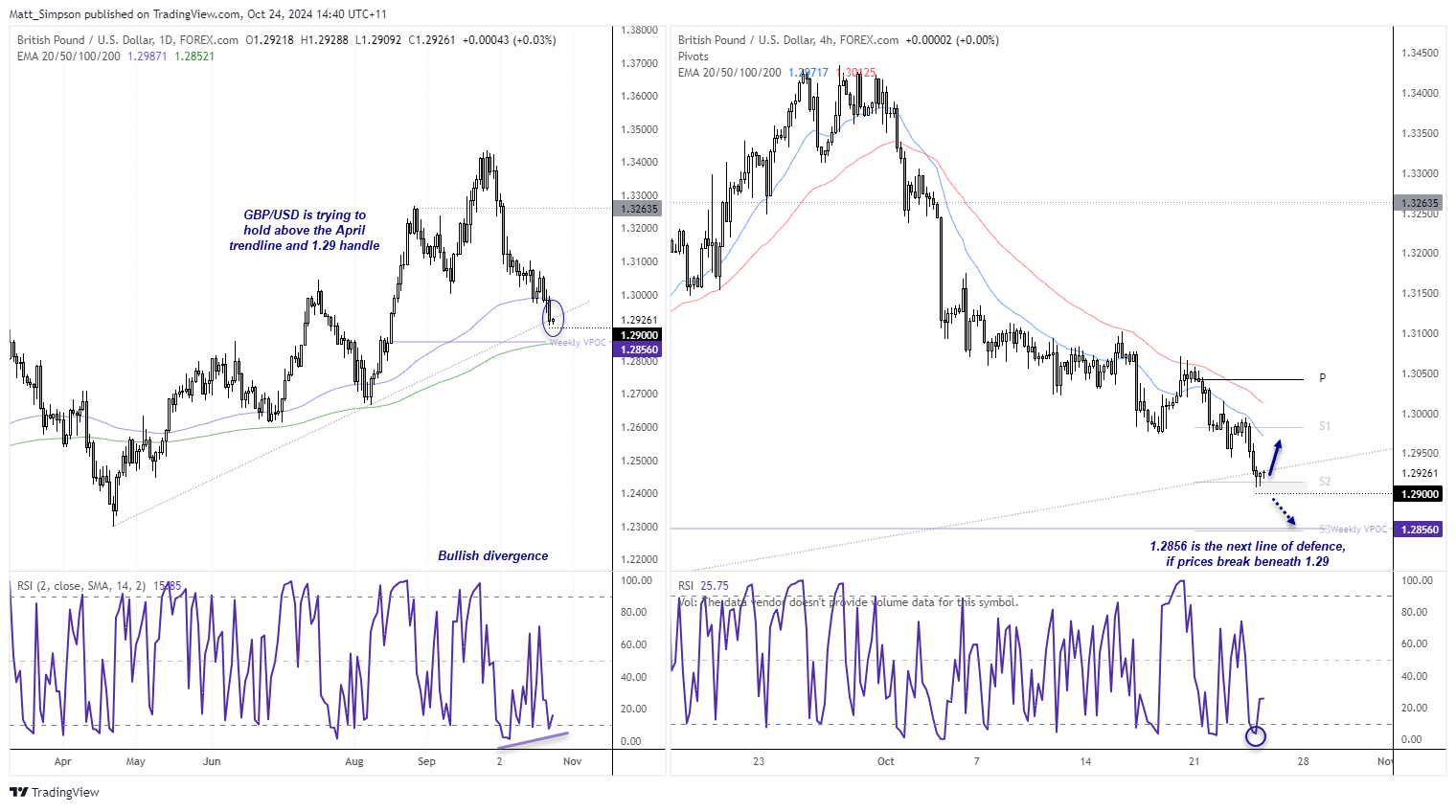

GBP/USD technical analysis:

The British pound has fallen just under 4% over the past four weeks, and finds itself trapped between the 200-day and 100-day EMAs. While 1.30 gave way this week, prices are tyring to build a base above 1.29 ahead of today’s figures. A strong set of PMI figures could help lift it from its lows, although bears could return if this was then coupled with a strong(er) US PMI report.

Should prices break beneath 1.29, GBP/USD might find support around the historical weekly VPOC (volume point of control) at 1.2856. This bearish move is not exactly new, and with a bullish divergence forming on the daily RSI (2) and the 4-hour recently having reached oversold, perhaps a bounce is indeed due.

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

Latest market news

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM

Yesterday 08:14 PM

Yesterday 08:00 PM

Latest articles

Today 12:31 AM

Yesterday 10:31 PM

Yesterday 08:30 PM