Oil prices rebounded strongly on Monday morning, but this could be a short-lived bounce as the crude oil outlook remains far from certain. The gains came on the back of raised geopolitical tensions as the US government said it is allowing Ukraine to use long-range American missiles against Russia. President Putin had previously warned that his country would view a strike inside Russia with missiles supplied by the US as a direct participation of NATO in the war. But questions remain as to how he will respond. And against a backdrop of rising supply and limited demand growth, not to mention oils’ ongoing bearish technical trend, the path of least resistance remains to the downside, and I would be surprised if a breakdown does not occur in the coming days. That’s unless Biden’s decision triggers some sort of Russian response that causes a supply side shock. Sentiment towards crude oil has turned bearish since Trump’s election victory, and amid growing signs of excess surplus coming from non-OPEC producers. There are now some concerns that if the OPEC+ cannot agree to extending their production agreement next month, this could give rise to fresh selling. At best, we could be looking at subdued prices in the coming months, until either demand growth picks up with the global economy, or oil production growth slows.

Crude oil outlook: Supply concerns could weigh on prices

Given the rise in non-OPEC supply growth, the OPEC+ will be under pressure to support prices. But the group has said that it will gradually restore withheld supplies after multiple delays. What’s more, we could see a sharp rise in US drilling activity under Trump’s plans. As a result, we could potentially see a boost in both OPEC and non-OPEC production by 2025 and beyond.

Additionally, Trump’s victory has led to geopolitical risk premiums being priced out – a trend reflected in the recent drop in gold prices. This shift stems from Trump’s promises to end ongoing conflicts, with markets seemingly optimistic about his ability to broker peace deals in the Middle East and between Ukraine and Russia. However, whether he can deliver on these pledges and the timeline for achieving them remain uncertain. For now, it appears traders are offloading oil first and saving their questions for later.

Oil market could be heading for surplus in 2025

Indeed, last week, the IEA predicted that the oil market looks like it’s in for a surplus next year. The group envisages the surplus to be in excess of over a million barrels a day—thanks largely to China’s weakening demand, where demand has fallen for six months straight. Demand growth in China is now growing at just a tenth of its 2023 rate. Meanwhile, growth in oil production from the non-OPEC producers, most notably the US, Brazil, Canada, and Guyana, are adding to signs of excess supply-side concerns. The IEA thinks that this year’s oil demand increase will only reach 920,000 barrels a day—less than half of last year’s growth rate—and next year’s rise doesn’t look much better, capped at around 990,000 barrels a day.

Demand concerns linger

By its own accord, the OPEC recent also cut its oil demand growth forecast for the fourth month in a row thanks to weak oil demand in China, the world’s largest oil consumer. But the OPEC+ is also ready to potentially inch production back up, starting with a modest 180,000-barrel increase planned for January. They’ll review this when they meet on December 1, and there is a good chance they could postpone this increase yet again, should prices fall further by then.

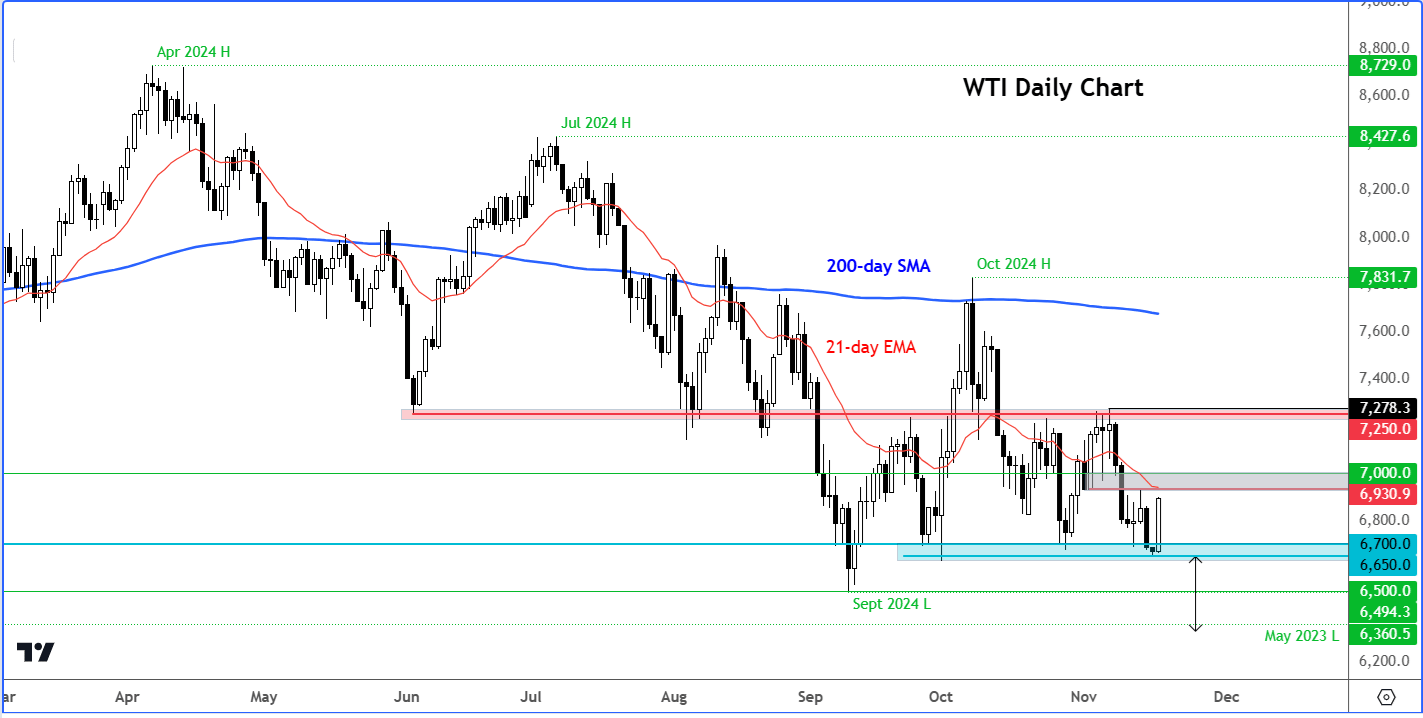

Crude oil technical outlook: WTI key levels to watch

Source: TradingView.com

Despite today’s sharp 3% rebound, until we see a clear reversal pattern in prices, the path of least resistance will remain to the downside. That’s because we are looking at a market with lower lows and lower highs, one where the moving averages have negative slopes and price action looking heavy. Every time oil has tried to rally in recent weeks, the sellers have stepped in to slam prices back down. That trend could continue this week after WTI’s positive start today.

Today, WTI oil prices have found good support from that $66.50 to $67.00 region once again. The key resistance area to watch is between $69.30 to $70.00, a recently broken support area. The bears would be looking to step in around these levels to maintain full control. If they successfully defend this area, then the next downside target below the aforementioned $66.50-$67.00 zone could be the September low of $65.27. Below that level, you have the May 2023 low at $63.64, but why stop there? So, we could see a sharp drop, if today’s earlier low gives way at some point this week.

Meanwhile, in the event we see a more meaningful recovery this week, then there is a possibility we could see WTI head initially to $70.00 and potentially all the way to the top of the recent range around $72.50, where prices might encounter stronger resistance.

In short…

The long and short of it is that lacklustre economic conditions and a growing shift to clean energy are reining in demand growth, at a time while supplies are rising and expected to get another boost under Trump. Against this backdrop, it is difficult to be positive on oil prices in the near-term outlook. It makes more sense, therefore, for traders to be looking for bearish setups near resistance, than bullish setups at support.

-- Written by Fawad Razaqzada, Market Analyst

Follow Fawad on Twitter @Trader_F_R

Latest market news

Yesterday 07:55 PM

Yesterday 05:50 PM

Yesterday 05:30 PM

Yesterday 05:06 PM

Latest articles

January 2, 2025 08:49 PM

December 29, 2024 08:30 PM

December 24, 2024 04:00 PM

December 24, 2024 01:00 PM