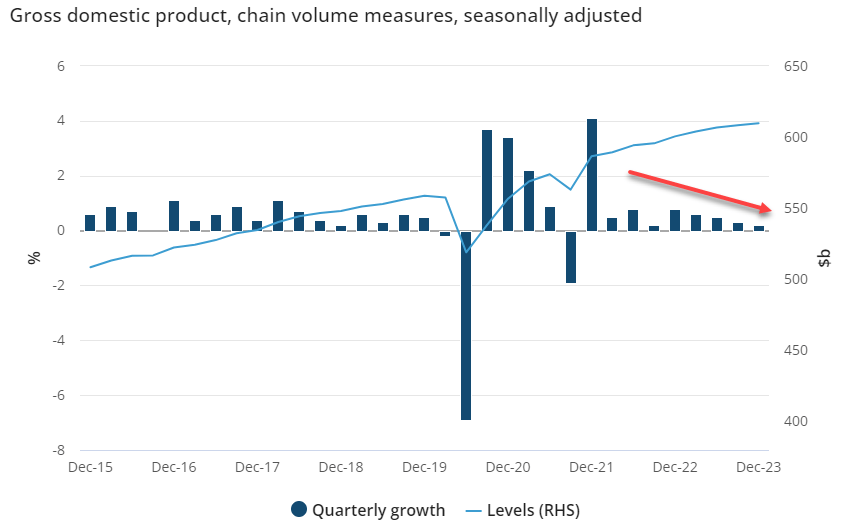

- The Australian economy grew 0.2% in Q4 and 1.5% over the year

- Growth was flattered by exports, rapid population growth and government spending, masking weakness in consumer spending

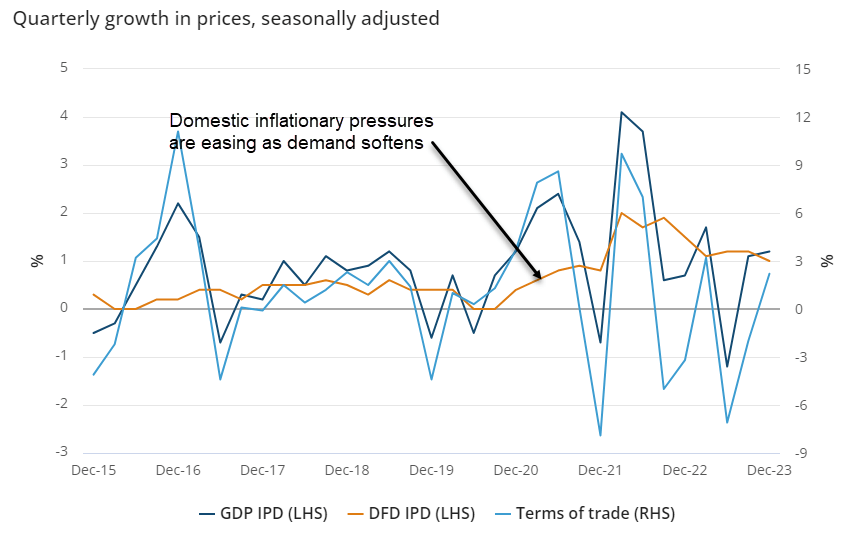

- Demand is softening while there is evidence that productivity trends are improving, creating conditions conducive to lowering inflation

- Dready domestic conditions and concerns about the Chinese economy continue to weigh on AUD

The largest and most important part of the Australian economy is struggling under the weight of higher borrowing costs, adding to the risk the Reserve Bank of Australia (RBA) may be forced to start lowering policy rates sooner than other central banks, keeping the Australian dollar under pressure.

Australian GDP up 0.2% in Q4, devil in the detail

According to the national accounts released by the ABS, GDP grew 0.2% over the December quarter and 1.5% over the year, the latter bang in line with forecasts issues by the RBA in February.

But it was the underlying detail that created the biggest talking points with household consumption expenditure – the largest part of the economy at over 50% -- increasing by 0.09% following a 0.21% decline in Q3 that was initially reported as an increase. The ABS said growth was slanted towards essential goods and services, masking another big drop in discretionary spending.

“The rise in essential spending was driven by spending on food and on electricity, gas and other fuels, with higher demand for cooling as a result of warmer than average weather for the December quarter, it said. “Spending in Food coincides with a fall of 2.8% in Hotels, cafes and restaurant spending, suggesting households substituted eating out for cooking at home.”

With the population increasing by 0.5% over the quarter, per capita consumption declined by 0.4%.

Exports, government spending boost growth

Instead of households, domestic spending was bolstered by government expenditure which rose 0.6%, helping to drive a 0.2 percentage point increase in domestic final consumption. Elsewhere, net exports added 0.6 percentage points to the quarterly GDP figure, more than offsetting a 0.3 percentage point drop in inventories.

Productivity pickup needed for RBA rate cut pivot

For the RBA, while the evidence is compelling that higher borrowing costs are sapping demand, challenges remain when it comes to being satisfied that inflation will be brought back to and remain around the 2.5% midpoint of its inflation target.

GDP per capita declined by 0.3% for the quarter in a sign of continued weakness in productivity. The news was a little better when measured in hours worked with GDP rising 0.5% following a 1% increase in Q3, although it remained negative over the year at 0.4%.

To allow for inflation to remain steady and the economy to expand, productivity growth is a necessity to prevent bottlenecks and delays. Australia’s track record has not been good on this front over the past decade, especially coming out of the pandemic where productivity has gone backwards.

At the same time, costs to produce goods and services have increased with real until labour costs – which measures the cost to produce a constant amount of output rising 3.7% over the year. More expensive to produce the same amount of output, put simply.

Combined with a surprise uptick in household savings for the first time since Q3 2021 over the quarter, which may help to underpin a pickup in household spending in the future, these factors will make it hard for the RBA to shift towards rate cuts near-term unless the economy continues to weaken further.

Right now, that is the risk but it’s no certainty.

Australian dollar soggy

For the Aussie dollar, the national accounts barely registered on the charts, in large part because it was bang in line with market expectations. But the details suggest a growing risk the RBA may abandon its tightening bias signalling the potential for further interest rate hikes.

Given the structure of Australia’s mortgage market where most of borrowing is priced off overnight rates, the abandonment of the tightening bias could quickly usher in potential rate cuts. When prior rate hikes really start to clamp down on the economy, it will likely be quick if history is a guide.

The dreary domestic economy, combined with pessimism towards China’s outlook, continues to weigh on the Aussie dollar against other major currencies, especially the US dollar which retains its economic exceptionalism tag relative to other parts of the developed world.

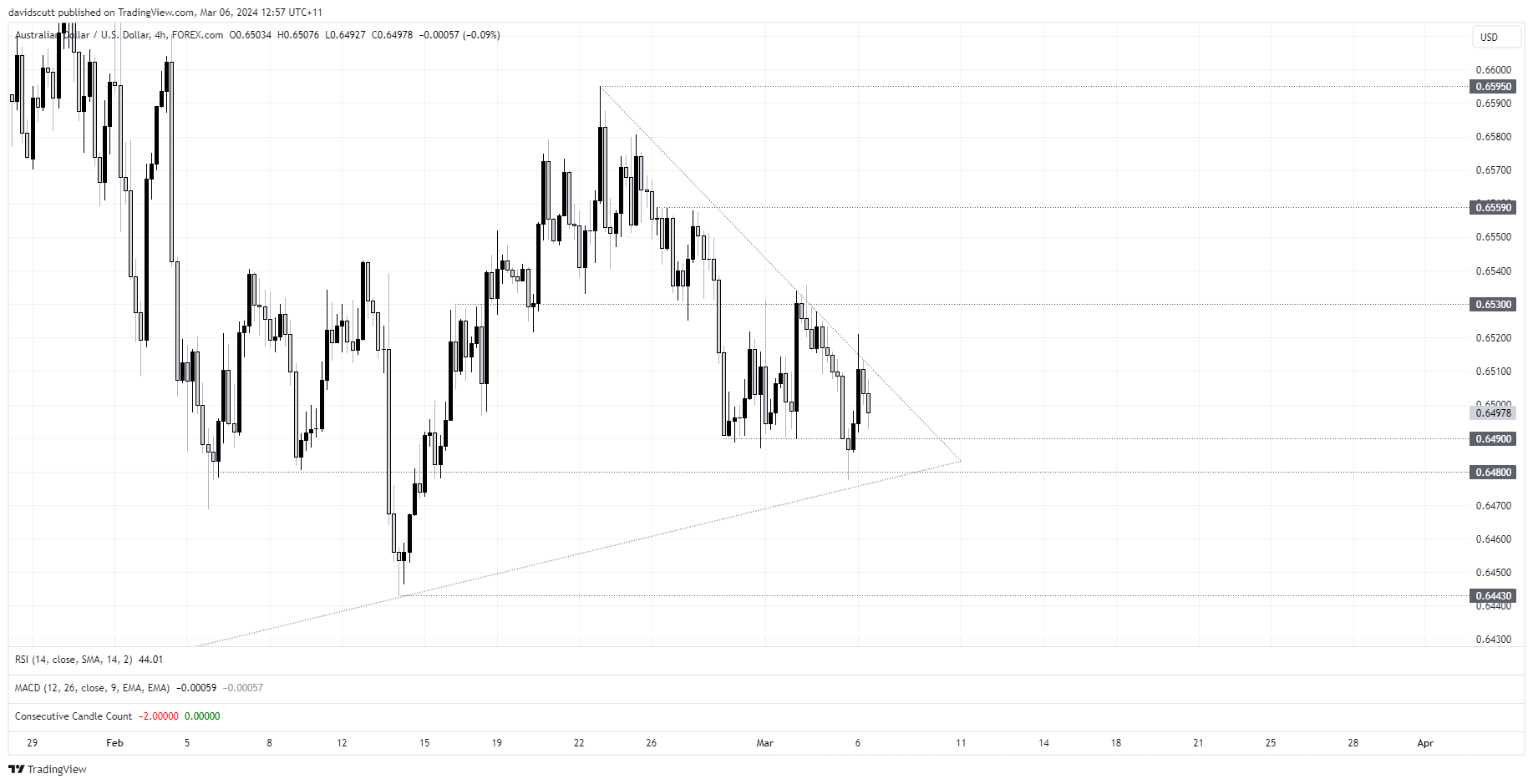

AUD/USD remains a sell-on-rallied play with a bounce on Tuesday on the back of the undershoot in the US ISM services PMI quickly rejected, sending it back below .6500. Bias remains to the downside near-term unless it can break the downtrend running from late February. Support between .6480-90 sits just above a longer-running uptrend dating back to November last year. Should the latter give way, it opens the door to a push back towards .6443.

The Aussie is also struggling against the crosses with EUR/AUD continuing to bounce off uptrend support, putting a potential retest of the recent high of 1.6745 into play should the upward shift continue. On the downside, a break of 1.6672 may be enough to spark a retracement back to support at 1.6600.

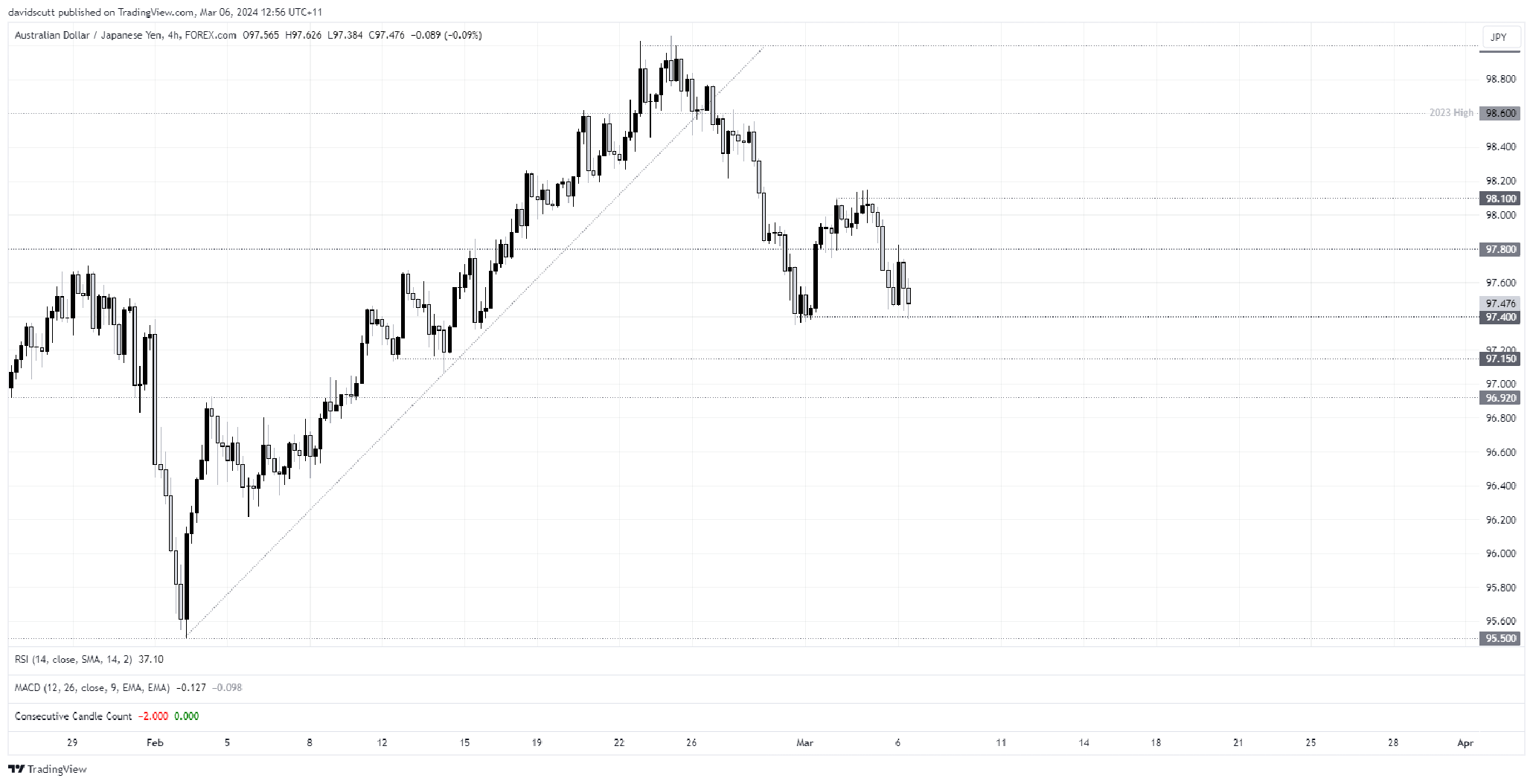

Having been rejected at resistance at 97.80 on Tuesday, AUD/JPY is threatening to break support at 97.40. If it does, traders will be eyeing off a return to 96.92 with only minor support at 97.15 located in between.

-- Written by David Scutt

Follow David on Twitter @scutty

Latest market news

Today 09:44 AM

Today 09:34 AM

Yesterday 07:55 PM

Yesterday 05:50 PM

Latest articles

May 6, 2024 06:05 AM

April 30, 2024 02:37 AM

April 24, 2024 06:51 AM

April 24, 2024 02:03 AM