Asian Futures:

- Australia's ASX 200 futures are up 14 points (0.19%), the cash market is currently estimated to open at 7,294.70

- Japan's Nikkei 225 futures are up 30 points (0.11%), the cash market is currently estimated to open at 28,260.61

- Hong Kong's Hang Seng futures are up 58 points (0.23%), the cash market is currently estimated to open at 25,020.59

UK and Europe:

- UK's FTSE 100 index fell -16.62 points (-0.23%) to close at 7,130.23

- Europe's Euro STOXX 50 index fell -17.43 points (-0.43%) to close at 4,055.09

- Germany's DAX index fell -52.27 points (-0.34%) to close at 15,146.87

- France's CAC 40 index fell -22.43 points (-0.34%) to close at 6,548.11

Tuesday US Close:

- The Dow Jones Industrial fell -117.72 points (-0.34%) to close at 34,378.34

- The S&P 500 index fell -10.54 points (-0.25%) to close at 4,350.65

- The Nasdaq 100 index fell -51.619 points (-0.35%) to close at 14,662.11

Indices: Fed on track for November taper, FOMC minutes released tonight

The global recovery has lost momentum according to the IMF (International Monetary Fund) which prompted them to trim their forecasts for global growth by 0.1% this year to 5.9% from 6.0%. 2022 growth is expected to come in at 4.9% before moderating to around 3.3% over the medium term. Investors have continued to buy long-term bonds at a faster rate than short-term bonds, which sent long-term yields noticeably lower (yields moves inversely to bond prices).

Two Fed members all but confirmed tapering is still on track as early as their November meeting. Bostic thinks the latest employment report shows sufficient progress to taper and that he endorsed a November start. This is despite concerns that the headline number completely missed expectations (but then perhaps markets expected too much anyway). And Clarida believes that “substantial further progress” has been more than met for towards their price stability and employment mandates. The Fed release their minutes of their October meeting tonight.

Concerns over stagflation (low growth, high inflation and unemployment) continued to weigh on equity prices. Rate-sensitive technology stocks were continued to slide, with the Nasdaq 100 touching a 4-day low and trading -0.35% lower. The Dow Jones and S&P 500 fell -0.34% and -0.24%, with communication services and utility sectors trading around -1.4% lower. Small caps bucked the trend to see the Russell 2000 rise 0.6%.

No updates to the ASX 200 analysis; we continue to suspect the corrective low of 7145 formed in September and await a decent break above 7332 to confirm its next leg higher.

ASX 200 Market Internals:

ASX 200: 7280.7 (-0.26%), 12 October 2021

- Healthcare (0.87%) was the strongest sector and Information Technology (-1.46%) was the weakest

- 9 out of the 11 sectors closed lower

- 4 out of the 11 sectors outperformed the index

- 54 (27.00%) stocks advanced, 138 (69.00%) stocks declined

- 59.5% of stocks closed above their 200-day average

- 36% of stocks closed above their 50-day average

- 42.5% of stocks closed above their 20-day average

Outperformers:

- + 4.6%-Sims Ltd(SGM.AX)

- + 4.3%-Perseus Mining Ltd(PRU.AX)

- + 4.2%-Alumina Ltd(AWC.AX)

Underperformers:

- ·-4.6%-Ansell Ltd(ANN.AX)

- ·-3.8%-Appen Ltd(APX.AX)

- ·-3.5%-Corporate Travel Management Ltd(CTD.AX)

Forex:

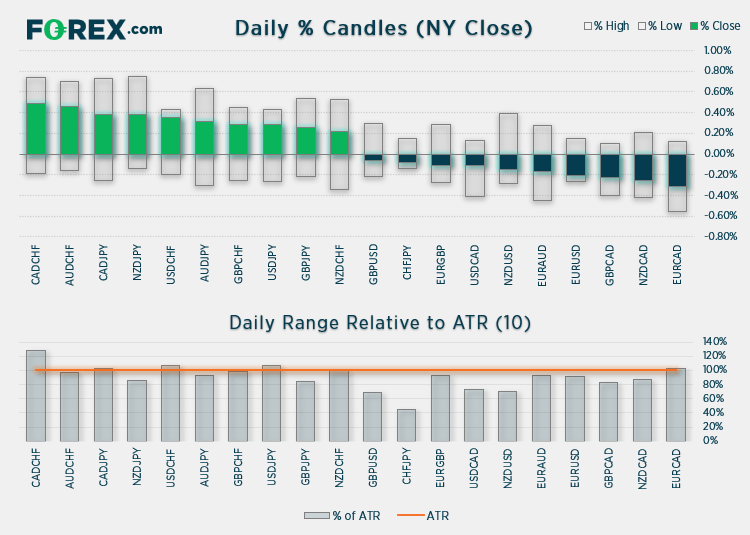

CHF and JPY remained the weakest currencies yet volatility was not quite what we saw on Monday. Commodity currencies were the strongest with AUD and CAD taking the lead (and are also the strongest currencies month to date).

The US dollar index (DXY) broke out of its coiling formation mentioned in yesterday’s report. We’d expect the September 2020 highs around 94.65 – 94.74 to cap as resistance initially, although the trend structure (and hawkish Fed backdrop) could send it above resistance it in due course.

EUR/AUD reached our 1.5664 target (and briefly traded beneath it) before recovering slightly above it. There are no obvious signs of a bottom yet and momentum favours a move towards 1.55, although we’re mindful of the potential for it to initially pause for breath around current levels.

AUD/USD touched a 1-month high on yield differentials, although its choppy breakout from the inverted head and shoulders is a little underwhelming. As is the spinning top Doji on the daily chart.

CAD/CHF was the strongest pair, rising to a 3-month high with a bullish outside day. Higher energy prices, strong fundamentals and hawkish BOC continue to support the Canadian dollar.

Commodities:

Platinum and palladium retraced from Monday’s highs but in a relatively orderly (and corrective) fashion. We are now seeking evidence of potential swing lows in anticipation of their next leg higher as we suspect they bottomed out in September.

Platinum’s daily chart broke above trend resistance and rose to a 9-week high on high volume on Friday, and the subsequent 2-days of trades has pulled back on lower volume which suggests the declines are corrective. Prices are holding above the 50-day eMA which sits around 1,000, although our bias remains bullish above the 981 high used to confirm the original breakout.

Natural gas futures fell to an 11-day low although recovered to close 1.8% higher and form a bullish pinbar on the daily chart. With the commodity remaining the main driver of the energy crisis, trades will be keeping a close eye on natural gas to see if it can break to new highs - as this translates to higher consumption prices and lower growth expectations, particular for the UK and across the rest of Europe.

Up Next (Times in AEDT)

Latest market news

Today 04:00 PM

Yesterday 08:00 PM

Yesterday 02:00 PM

Yesterday 07:00 AM

Yesterday 02:00 AM

December 24, 2024 08:00 PM

Latest articles

December 23, 2024 02:45 PM

December 20, 2024 02:45 PM

December 19, 2024 10:26 PM

December 19, 2024 05:22 PM