2018/11/1 12:29:00

As you might expect from the undeniably “risk-off” tone throughout the month of October, the “safe haven” Japanese yen was last month’s best-performing major currency. The big surprise, however, came from a different safe haven currency; the Swiss franc was the weakest major on the month, edging out the euro.

Perhaps SNB President Jordan’s statement that Switzerland could be among the countries worst hit by a trade war has a kernel of truth, even if no countries are rushing to put tariffs on Swiss chocolate or watches.

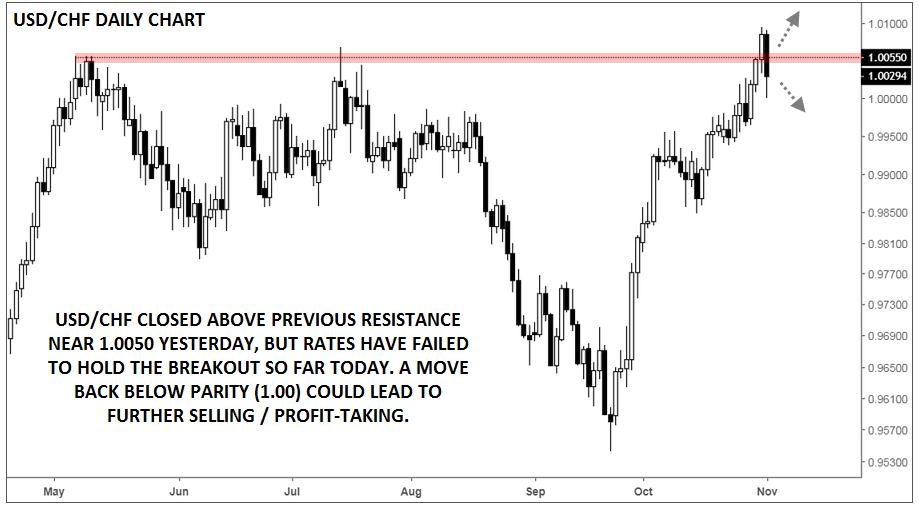

In any event, USD/CHF closed the month at its highest level in 17 months near 1.01, putting bulls in an optimistic mood heading into December. That said, today’s big reversal in the greenback has taken the pair back toward parity (1.00), raising the specter of a big “false breakout.”

Put simply, the longer USD/CHF holds below previous resistance in the mid-1.00s, the more nervous trapped bulls will become. If we see a close below parity, longs may abandon their positions en masse, leading a sharp drop back toward 0.9900 heading into the weekend (especially if tomorrow’s NFP report shows weakness).

On the other hand, a stronger-than-expected NFP report could take USD/CHF back toward 1.0100, paving the way for a continuation toward 1.02 or the previous highs above 1.03 next.

Source: TradingView, FOREX.com

最新市场分析

十二月 16, 2024 01:48 上午

十二月 9, 2024 02:11 上午

十一月 25, 2024 02:01 上午

十一月 20, 2024 03:31 上午

十一月 18, 2024 03:01 上午

十一月 11, 2024 01:22 上午